Comfort Systems USA, Inc. FIX delivered a stunning first-quarter performance for 2026, but beyond the eye-popping revenue growth, one key question stands out for investors: Is margin expansion becoming the company’s true long-term earnings engine?

The company reported first-quarter 2026 earnings of $10.51 per share, up 121.3% from $4.75 reported in the year-ago quarter. Revenues surged 56.8% year over year to $2.87 billion, driven by relentless demand from technology and data center customers. However, the biggest surprise came from profitability metrics, which improved at an even faster pace than sales.

Gross profit soared 87% to $754 million, while gross margin expanded to 26.3% from 22.0% a year ago. Operating margin climbed sharply to 17.0% from 11.4%, reflecting strong project execution, favorable late-stage project developments and meaningful operating leverage. Management noted that both Mechanical and Electrical segments benefited from booming technology-sector demand, with Electrical revenues jumping 88% year over year. Importantly, selling, general and administrative (SG&A) expenses rose far more slowly than revenues, allowing FIX to convert higher sales into disproportionately stronger profits. Meanwhile, a record backlog of $12.45 billion (up 80.8% year over year) provides significant visibility into future work.

FIX is also investing heavily in modular construction capacity and automation, aiming to improve labor productivity and execution efficiency over time. While elevated CapEx could pressure near-term free cash flow, these investments may strengthen margins further in the coming years. Thus, Comfort Systems’ latest results suggest that rapid revenue growth alone is not driving the story. Increasingly, disciplined execution and expanding margins appear to be powering its exceptional earnings trajectory.

Comfort Systems, EMCOR & Carrier Global: Backlog Boom or Peak Cycle?

Comfort Systems, sharing space with renowned market players, including EMCOR Group, Inc. EME and Carrier Global Corporation CARR, are benefiting from accelerating demand tied to data centers, electrification and advanced technology infrastructure, but each company brings a different operational strength to the market.

EMCOR offers a more diversified model across mechanical, electrical and facilities services, helping it balance cyclical construction exposure with recurring service revenues. Its scale and disciplined execution continue to support steady backlog conversion and resilient profitability.

Meanwhile, Carrier Global is leveraging demand for high-efficiency HVAC, cooling and climate-control systems critical to AI-driven data centers. Unlike the project-heavy models of Comfort Systems and EMCOR, Carrier Global benefits more from equipment demand, aftermarket services and energy-efficiency trends, giving it a differentiated position amid evolving infrastructure spending.

FIX Stock’s Price Performance & Valuation Trend

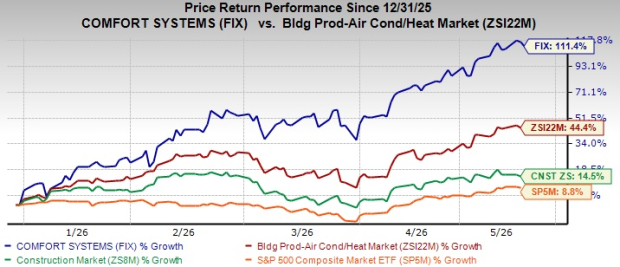

Shares of this Texas-based heating, ventilation, air conditioning and electrical contracting service provider have spiked 111.4% year to date, significantly outperforming the Zacks Building Products - Air Conditioner and Heating industry, the broader Construction sector and the S&P 500 Index.

Image Source: Zacks Investment Research

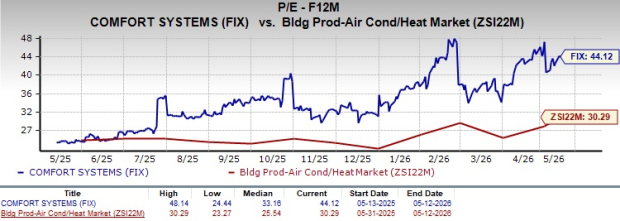

FIX stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 44.12, as the trend lines suggest below.

Image Source: Zacks Investment Research

Earnings Estimate Trend Favors FIX

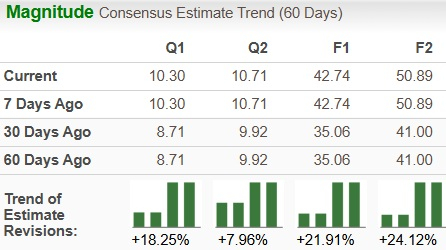

FIX’s earnings estimates for 2026 and 2027 have moved upward in the past 30 days to $42.74 and $50.89 per share, respectively. The revised estimates for 2026 and 2027 imply year-over-year growth of 48% and 19.1%, respectively.

Image Source: Zacks Investment Research

Comfort Systems currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpEMCOR Group, Inc. (EME) : Free Stock Analysis Report

Comfort Systems USA, Inc. (FIX) : Free Stock Analysis Report

Carrier Global Corporation (CARR) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.