David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Coca-Cola Consolidated, Inc. (NASDAQ:COKE) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Coca-Cola Consolidated's Debt?

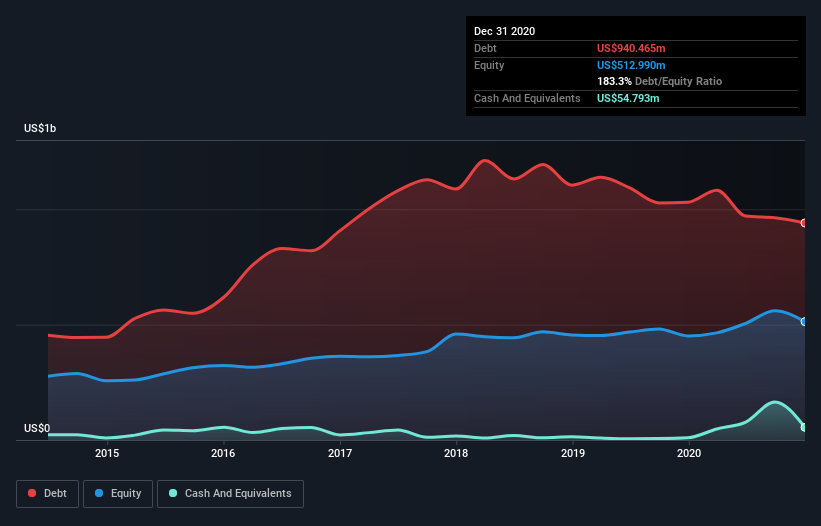

As you can see below, Coca-Cola Consolidated had US$940.5m of debt at December 2020, down from US$1.03b a year prior. However, it also had US$54.8m in cash, and so its net debt is US$885.7m.

A Look At Coca-Cola Consolidated's Liabilities

We can see from the most recent balance sheet that Coca-Cola Consolidated had liabilities of US$647.1m falling due within a year, and liabilities of US$2.06b due beyond that. Offsetting these obligations, it had cash of US$54.8m as well as receivables valued at US$490.1m due within 12 months. So its liabilities total US$2.16b more than the combination of its cash and short-term receivables.

This is a mountain of leverage relative to its market capitalization of US$2.74b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Coca-Cola Consolidated's net debt of 1.8 times EBITDA suggests graceful use of debt. And the fact that its trailing twelve months of EBIT was 8.5 times its interest expenses harmonizes with that theme. Importantly, Coca-Cola Consolidated grew its EBIT by 70% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is Coca-Cola Consolidated's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Coca-Cola Consolidated recorded free cash flow worth 79% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

The good news is that Coca-Cola Consolidated's demonstrated ability to grow its EBIT delights us like a fluffy puppy does a toddler. But truth be told we feel its level of total liabilities does undermine this impression a bit. When we consider the range of factors above, it looks like Coca-Cola Consolidated is pretty sensible with its use of debt. While that brings some risk, it can also enhance returns for shareholders. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 1 warning sign for Coca-Cola Consolidated you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.