Church & Dwight Co., Inc. CHD appears in a troubled spot. The company is facing challenges related to volatile consumer spending in the current environment. Increasing marketing expenditure and weakness in the gummy vitamins business are also a concern for the company’s overall performance.

These downsides are reflected in Church & Dwight’s guidance for the third quarter and 2024. Reflecting the negative sentiment, the Zacks Consensus Estimate for the current quarter and full year has seen downward revisions.

Here’s Why Church & Dwight Stock is Acting Up

The company is also navigating headwinds from changes in consumer spending patterns. Recent trends indicate a slowdown in consumer consumption, particularly in June and July, where dollar consumption growth decelerated from 4.5% to approximately 2%. This deceleration is attributed to consumers adjusting their spending habits in response to extended economic pressures and rising prices.

The company notes that while its portfolio of value and premium products is well-suited to navigate these shifting consumer patterns, the overall slowdown suggests that future growth may be more modest compared to the first half of the year.

Church & Dwight’s gummy vitamins business continues to be a drag on overall growth, with a notable decline of 10.9% in consumption in the second quarter compared to the previous year. Although there are efforts to stabilize the segment through new packaging and formulas, the recovery has been slower than anticipated, impacting overall performance in the personal care category.

CHD has been witnessing increasing marketing expenses for the past few quarters as it has been undertaking increased marketing to fuel brand awareness, especially for new products and acquired brands. In the second quarter of 2024, marketing expenses increased $20.2 million year over year to $152.4 million. As a percentage of net sales, the figure rose 100 bps to 10.1% on persistent investment in brands and new products. Adjusted SG&A expenses, as a percentage of net sales, expanded 20 bps to 14.4% due to investments in international operations, research and development and expenses associated with the Graphico acquisition.

Church & Dwight anticipates marketing, as a percentage of sales, to be nearly 11% in 2024. Adjusted SG&A, as a percentage of sales, is projected to be higher year over year, up from the previous expectation of being flat. This upside reflects additional costs associated with the Graphico acquisition and higher incentive compensation than initially anticipated.

Image Source: Zacks Investment Research

What to Expect From CHD in 2024?

Although the company anticipates its brands to outperform the categories in the second half of the year, it adjusted the 2024 organic revenue forecast to about 4% growth on its lastearnings call down from the previous range of 4-5%. Reported sales growth is projected to be slightly lower, around 3.5%, due to the effects of divestitures and adverse currency fluctuations.

Adjusted EPS growth is now expected to be at the lower end of the 8-9% range. For the third quarter, the company anticipates quarterly adjusted earnings of 67 cents a share, suggesting a year-over-year decline of 10%.

Final Thoughts on CHD

While a solid brand image, innovative products and strategic expansions place Church & Dwight well for long-term success, the abovementioned obstacles cannot be overlooked for the near term. All said, investors should approach CHD stock with caution. The company currently carries a Zacks Rank #4 (Sell).

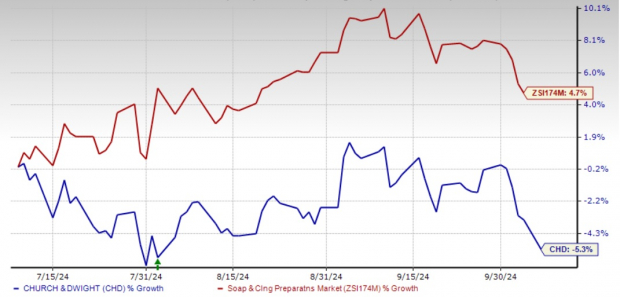

Shares of CHD have dropped 5.3% in the past three months against the industry’s growth of 4.7%.

Three Staple Stocks Worth Betting On

The Chef’s Warehouse CHEF, which engages in the distribution of specialty food products, currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

CHEF has a trailing four-quarter earnings surprise of 33.7%, on average. The Zacks Consensus Estimate for The Chef’s Warehouse’s current fiscal year sales and earnings indicates growth of 9.7% and 12.6%, respectively, from the year-ago reported numbers.

Flowers Foods FLO, a packaged bakery food company, currently carries a Zacks Rank #2. FLO has a trailing four-quarter earnings surprise of 1.9%, on average.

The Zacks Consensus Estimate for Flowers Foods’ current financial-year sales and earnings implies growth of around 1% and 5%, respectively, from the year-ago reported numbers.

McCormick MKC is a leading manufacturer, marketer and distributor of spices, seasonings, specialty foods and flavors. It currently carries a Zacks Rank of 2.

The Zacks Consensus Estimate for McCormick & Company’s current fiscal-year earnings indicates an advancement of 5.9% from the year-ago reported figures. MKC has a trailing four-quarter earnings surprise of 13.8%, on average.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Church & Dwight Co., Inc. (CHD) : Free Stock Analysis Report

McCormick & Company, Incorporated (MKC) : Free Stock Analysis Report

Flowers Foods, Inc. (FLO) : Free Stock Analysis Report

The Chefs' Warehouse, Inc. (CHEF) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.