Credit:

Credit: By Josh Blechman :

By Herbert D. Blank, Senior Consultant, Global Finesse LLC & Qiao Duan, Quantitative Analyst, Exponential ETFs

Abstract

Index investing can trace it roots back almost 50 years. However, the dynamics around implementing index portfolios have changed as capital markets have evolved, opening up new discussions around the possibilities and potential benefits of different index methodologies. This paper sets out to explore the investment potential of an index consisting of the same stocks as the popular market-cap-weighted S&P 500, but weighted by the reciprocal of each stock's market capitalization. We explore the properties such an index would have versus traditional capitalization-weighted and equally weighted schemes. This is followed by empirical testing and attribution analysis to confirm whether reverse-cap weighting provides a viable alternative to the momentum, concentration, and anti-value biases inherent in capitalization weighted indices.

Evolution of US Index Weighting Schemes

In order to understand how market cap-weighted indexing became the global industry standard for passive investment, it is important to understand how passive investment evolved. The beginnings trace back to the 1969-1971 period (Bernstein, 1991). Wells Fargo Bank ( WFC ) had worked from academic models to develop the principles and techniques leading to index investing. John A. ("Mac") McQuown and William L. Fouse pioneered the effort, combined with the growing institutional interest in investing in this manner, led to the construction of a $6 million index account for the pension fund of Samsonite Corporation.

The actual implementation details significantly influenced how index funds developed for the next 30 years. With a strategy based on an equal-weighted index of New York Stock Exchange equities, its execution was described as "a nightmare." Transaction costs were eating up most of the profits realized by the portfolio.

Today, stock transaction and impact costs for most large cap US-equities are trivial. This was not the case, however, until more than 20 years later.

The equal-weighting strategy was replaced by a market-weighted strategy in 1976 using the Standard & Poor's 500 Composite Stock Price Index. Drawing on a market-cap-weighted index created by Alfred Cowles to represent and measure consistently the average experience of stock market investors, the Standard & Poor's 500 Index launched in 1957. Although measurement, not ease of portfolio management was its purpose in design, this little-known-at-the-time index was the answer to the prayers of the Wells Fargo team.

From an index portfolio manager's viewpoint, market-cap weighting is as good as it gets. The only time portfolio trading is needed is when there is a corporate action or a constituent change in the index. It should be no surprise, then, that market-cap-weighted indices became the standard for core equity index investment.

An interesting sidebar is how this evolution debunks the widespread belief that Bill Sharpe's Modern Portfolio Theory (MPT) model was based upon a cap-weighted market index; as seen above, it was not. Cap-weighting became the indexing standard as a direct result of implementation issues, not efficient-market theory. Therefore, MPT does not dictate that alternative systematic market-weighting schemes cannot produce consistently superior returns over time.

Challenges to Market-Cap Weighting

By the end of the 20th Century, large institutional acceptance of MPT principles and cap-weighted benchmarks for equity performance was the rule. Accordingly, the largest plans routinely indexed a significant portion of core equities to a market-cap weighted index, usually the Russell 1000. Active management was, and still is, far from dead. Pension consultants still promulgated a select list of specialty active managers for whom they used MPT-driven statistics to show potential outperformance within style boxes. Moreover, some plans still refused to use index managers because they considered the concept of not trying to outperform to be "un-American."

Increasingly, however, some of the top academic researchers and index practitioners came to believe that market-cap indexing was then not necessarily the best that investors could do. Efficient Market Theory standard-bearers Eugene Fama and Kenneth French, went into the asset management business after publishing research that there are certain factors that caused value and small cap stocks to outperform over time (Fama and French, 1992). This leads directly to the logical conclusion that if small cap and value stocks were undervalued, large cap stocks must be systematically overvalued.

These are considered seminal findings. By definition, market-cap weighted indices put increasingly higher weights in stocks as they become higher in relative market cap and relative growth (as defined as inverse of value) because both increase formulaically with increases in share price. Therefore, market-cap-weighted indices must contain intrinsic inefficiencies relative to other index weighting schemes.

Concentration and Anti-Value Biases of the S & P 500 Index

Anyone who reviews SPIVA (Standard & Poor's Index Vs. Active) data knows that S & P 500 index fund performance has been formidable and extremely difficult for actively managed mutual funds to beat. Yet, the same may not be true of other index funds using the same selection universe.

Carlson (2016) showed that in terms of style, the S&P 500 Index ETF, SPY, is a momentum fund relative to the universe of mutual funds. He called S&P 500 indexing the world's largest momentum strategy which is not to be dismissed lightly. Price momentum can be an effective strategy in some markets, but certainly not all.

An article by Fernholz, Garvy, and Hannon (Fernholz, et al, 1998) demonstrated that the over-concentration of the S&P 500 led to an over-concentration in stocks that had exhibited recent relative outperformance. Overweighting recent winners was shown to be equivalent to a systematic risk factor and thus not negated by portfolio diversification. They introduced a mathematical construct called the Diversity Index that mathematically distributed weights downward in the portfolio without using optimization. The top 25 holdings of the Diversity Index accounted for less than 20% of the index's weight rather than more than 30%. They then showed that the Diversity Index exhibited higher returns with the same risk level as the S&P 500 over a 30-year period.

The overweighting of recent winners also runs contrary to a study by Hillenbrand in 2003. This study found that mean-reversion in stock returns is a transient but recurring phenomenon. Ringenaum (Ringenaum, 1983) showed that price momentum as a factor tends to peak over a six-month factor, then tended to mean-revert. Mean reversion has been postulated as one of the reasons for the success of the Dogs of the Dow strategy for more than 50 years. This has relevance to the S&P 500 selection set. Since new companies selected by the S&P 500 Index Committee tend to be former mid-cap companies that have had recent superior performance, these companies typically enter at a market cap higher than its bottom 100 market cap companies. The Committee has never selected a new entrant as its lowest market cap company. Therefore, the stocks near the bottom of its market capitalization spectrum are likely its most opportune candidates for mean reversion. This is especially true since part of the function of the S&P 500 Selection Committee is to remove stocks that have declined precipitously in the market due to solvency problems. This implies that the survivor companies with reasonably strong balance sheets that have simply fallen out of favor. A white paper (Krause, 2012) demonstrated the effectiveness of a diversified strategy selecting stocks with the highest yields, intrinsically due primarily to poor relative recent price performance, in their industry sector.

Trading and Fund Structures Get Much More Efficient

A few years into the 20th Century, just about everything had changed during the previous 15 years for equity traders. The advent of new technologies and regulatory conventions transported a world that had traded in eighths to decimals, from an exchange-centric specialist-controlled system to fragmentation and disintermediation, and from calling a broker to trading online (Board et al, 2002). Unlike the early experiences of the Wells Fargo team, the trading costs of managing and trading an equally weighted 500 stock portfolio were now manageable.

Moreover, ETFs, introduced in the US with SPDRs in 1993, were beginning to be offered for indices beyond the standard institutional benchmarks.

One of the best-known examples of the is an exchange-traded fund ((ETF)) launched by Rydex Funds in 2003 was designed to hold 500 equally weighted positions of the constituents of the S&P 500 index with the ticker symbol RSP. The first full month of performance for the now Guggenheim S&P 500 Equal Weight ETF ( RSP ) was May 2003. The compound average annualized returns of RSP vs. the SPDR S&P 500 Trust ETF ( SPY ), from the morning of May 1, 2003 through the most recent year end, December 31, 2017 are respectively 10.89% and 8.87%

Exhibit 1

We apply this formula for the examples of 500-stock portfolios with the same exact stocks but drastically different weighting schemes: equally weighted; market-cap weighted; and reverse market-cap weighted. In order to make sure we refer to the same stocks in each portfolio, we will rank each stock's identifier (CUSIP) from 1 to 500 in order of its market cap and we will calculate the weight of each stock in each portfolio using this sort order with CUSIP #1 belonging to the stock with the largest market capitalization in the beginning of the period and CUSIP #500 belonging to the stock with 500th largest (smallest) market capitalization at the beginning of the period. Further, for easy comparison, we will substitute for the generic

The major difference between equation x and equation y is that in the x equation, the series of weights are not identical, so it matters which weight is to be multiplied to each successive return. This means that we need to run enough simulations to cover all possible permutations of returns for the descending order of weights, a process known as Monte Carlo simulation.

Therefore, when b , the expected return of the 380 relatively lower cap stocks is greater than a , then y , the return of the equal-weighted portfolio will be greater than x , the return of the cap weighted portfolio. Conversely, when a >b , x will be greater than y . Of course, when a = b , x and y are equal.

What does all this mean from a practical perspective? Looking back at the work of Fama-French, Fernholz, Hillenbrand, etc. and the empirical outperformance of SPY by RSP, there is certainly reason to believe that it is plausible that the smaller cap 380 stocks of the S & P 500 will have higher average returns than their largest 120 stock compliments more often than not.

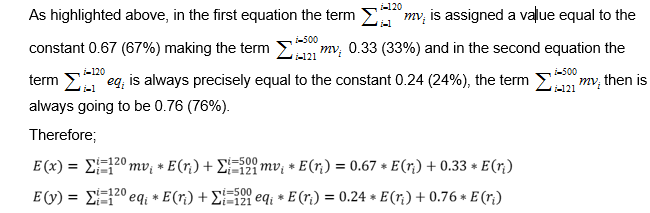

Now, let's examine the case of the Reverse Cap Weighted U.S. Large Cap Index. By definition, the smaller 380 stocks will always be greater than, or equal to, the equal-weighted 76% of the portfolio. Similarly, the top 120 market-cap stocks will always be weighted less than, or equal to, the equal-weighted 24% of the portfolio. Let's look empirically what this looks like. As of December 31, 2016, the 120 largest market cap stocks comprised 5.6% or the portfolio and the portfolio weights of the smaller 380 stocks by market cap was 94.4%.

Skipping the derivations, because all the above simplifications hold true for this weighting scheme as well, we can express the return, z , of the reverse-cap-weighted portfolio using the same a and b as:

So, on an expected value basis, when b >a , then z >y >x .

When a >b , then xyz . And when a = b , x = y = z .

If one accepts the case made earlier that it is reasonable to expect that over time the equally weighted S&P 500 will outperform the cap-weighted S&P 500, then it is at least an equally reasonable expectation that the reverse-cap-weighted portfolio will outperform both.

Empirical Results

Point-in-time data were used to run a back-test from September 30, 2007 through the September 30, 2017 that was devoid of look-ahead bias. This table displays the annualized returns and standard deviations for the 10-year period.

The above table illustrates clearly that REVERSE (Reverse Cap Weighted U.S. Large Cap Index) had an annualized 10-year return of 10.36%, 292 basis points better than SPX (S&P 500). Exhibit 2 below shows that an investor would have accumulated 60% more wealth (10-year gain of $167.90 vs. $104.88) with REVERSE than SPX.

Exhibit 2

Taken together, a clear illustration of what one might expect from the three indices is confirmed. The theory postulated above that the Reverse Cap Weighted U.S. Large Cap Index should generate the top returns over most lengthy periods is confirmed by the data.

In years of extreme market stress and downside volatility, the market tends to drift toward the perceived safety of the highest quality equity which are generally the stocks of highest market capitalization. Indeed, in each of the three years above when the S&P 500 delivered flat-to-negative returns, it outperformed the Equally-weighted (S&P 500 EWI) which in turn outperformed REVERSE. In five of the remaining six years when the S&P 500 return exceeded 10%, the order was reversed. REVERSE outperformed S&P 500 EWI, which outperformed the S&P 500 Index. Thus, the test period confirms the expectation that since market returns skew positively over time, REVERSE should be the best performer of the three in most years. The table above also shows that there tends to be a cost to the higher returns. REVERSE had a significantly higher annualized volatility than S&P 500 EWI. The lowest annualized volatility of the three was exhibited by SPX. These results are also in keeping with expectations.

The expectation that REVERSE would be more diversified than SPX was also tested empirically. For this purpose, the Herfindahl-Hirschman index (HHI), a commonly accepted measure of market concentration, was applied to annual snapshots of both indices for the nine calendar years. Exhibit 4 below illustrate how consistently REVERSE with an average HHI of 38 as compared with 77 for SPX measured as the more diversified of the two.

Exhibit 4

The Sortino ratio is a useful way for investors, analysts and portfolio managers to evaluate an investment's return for a given level of downside risk (Sortino and van der Meer, 1991). Since this ratio uses the downside deviation as its risk measure, it addresses the problem of using total risk, or standard deviation, as upside volatility is beneficial to investors. The higher the ratio, the better the investment's return per unit of downside risk. This examination makes it clear that the higher overall volatility of REVERSE is concentrated on the upside and that its added return more than compensates investors for the level of downside risk taken relative to the S&P 500 Index.

Implications for Investors

REVERSE - the Reverse Cap Weighted U.S. Large Cap Index, provides an intriguing alternative weighting scheme with the potential to realize in superior rates of return to both S&P 500 EWI, the equally weighted S&P 500 and SPX, the traditional S&P 500 Index that is renowned for being market-cap weighted. In fact, there is both theoretical and empirical justification to expect relatively superior returns from REVERSE, especially during periods of market expansion. Although these superior returns are associated with greater market volatility, the Sortino ratio comparison illustrates that a disproportionate amount of that volatility comes on the upside which benefits investors.

REVERSE may also be useful to tactical investors. An investor with the conviction that a market expansion will continue would invest based on this index until he or she detected a potential regime change. In that event, an investment vehicle based on REVERSE could well be used as a source of funds or even a shorting opportunity.

Reverse can further be used as a way to combat the weaknesses and vulnerabilities inherent to cap weighted indices that were discussed above. Through blending a traditional cap weighted index such as SPX with REVERSE, an investor can choose to amplify or mute the effects of cap weighting in a precise way in order to fit their market outlook.

Areas for Further Study

Ideally, we would like to calculate daily performance for REVERSE on a point-in-time basis starting when S&P Index-based derivatives first became available in the 1980's. This would provide more empirical validation of its ability to outperform over time. It would also provide a much longer horizon for event studies of potential tactical applications. Practically speaking, this endeavor capturing 10 years of history was more painstaking than we anticipated at this time. At a future point in time, perhaps it will be easier to expand the testing period.

Summary

It took more than 20 years since the introduction of the first index fund in 1973 for the strategy to be accessible and meaningful to anyone but large institutional investors and academics. This has changed dramatically with the advent of ETFs and the success of the Vanguard Group both beginning in the early 1990s. Another phenomenon is that brokerage fees and impact trading costs have diminished dramatically. Until then, trading costs associated with most enhanced indexing strategies made them cost-inefficient. However, the empirical superiority since the 2003 inception of equally-weighted RSP, over cap-weighted SPY, has demonstrated that non-market-cap weighted schemes using S&P 500 stocks now have the potential to succeed. These results provided the inspiration for the Reverse Cap Weighted U.S. Large Cap Index (REVERSE). If equal weighting resulted in superior returns by avoiding increasing allocations to increasingly overpriced stocks, perhaps reversing the allocation completely would result in even higher returns. Examining the literature and actual launches, we found a number of compelling arguments and rationales why pursuing such a scheme made sense. Next, we ran an empirical test which showed that for the ten-year-period ending September 30, 2017, the Reverse Cap Weighted U.S. Large Cap Index delivered 292 basis points per annum superior performance to the S&P 500 index. Although these superior returns are associated with greater market volatility, concerns are mitigated by our Sortino ratio tests - demonstrating that a disproportionate amount of that excess volatility is attributable to higher upside returns. Also noteworthy are the pronounced cyclical differences between REVERSE and the S&P 500 in up markets as compared with sideways and down markets. For hedge funds and other investors implementing a regime change strategy, REVERSE represents a potentially powerful tactical tool.

References

- Bernstein, Peter L., Capital Ideas, John Wiley and Sons, 1991, pp. 21 - 38

- Board, J., Sutcliffe, C., Wells, S., Transparency and Fragmentation: Financial Market Regulation in a Dynamic Environment, Palgrave MacMillan, 2002, pp 81 - 82

- Carlson, Ben, "Seven Strategies for Investing in Market Peaks," URL: www.bloomberg.com/view/articles/2017-08-17/seven-strategies-for-investing-at-market-peaks

- Fama, Eugene L., and French, Kenneth," The Cross-Section of Expected Stock Returns", Journal of Finance, pp 427-465

- Fernholz, R., Garvy, R., and Hannon J., "Diversity-weighted indexing," Journal of Portfolio Management, Winter 1998, pp 74-82

- Hillenbrand, Eric, "A Mean-Reversion Theory of Stock-Market Crashes", Stanford University Department of Mathematics Working Paper, March 30, 2003

- Krause, Michael, "Tests of the Sector Dividend Dog Index", Alta Vista Working Paper, June 2012

- Reinganum, Marc. "The Anomalous Stock Market Behavior of Small Firms in January, Empirical Tests for Year End Tax Effect," Journal of Financial Economics. Winter 1983,12, pp 89-104

- Sortino, Frank L. and van der Meer, Robert, "Downside Risk", Journal of Portfolio Management, Spring 1991, pp 27 - 31

See also Starbucks: Does It Still Have A Bright Future? on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}