Carnival Corporation & plc’s CCL decision to resume its dividend marks a notable milestone for shareholders, signaling a clear shift from balance sheet repair to capital returns. After several years of suspension following the pandemic-driven downturn, management announced the reinstatement of a quarterly dividend of 15 cents per share, underpinned by strengthening fundamentals and renewed confidence in cash generation.

The timing of the move is significant. Carnival closed fiscal 2025 with record revenues, EBITDA and net income while delivering more than $3 billion to the bottom line. Strong pricing, resilient onboard spending and disciplined cost control lifted margins to multi-year highs. The company achieved an investment-grade net debt-to-EBITDA ratio of 3.4, well ahead of its original deleveraging timeline, after reducing total debt by more than $10 billion in less than three years.

Management framed the dividend resumption as part of a broader capital allocation reset rather than a one-off gesture. With no new ship deliveries in 2026 and EBITDA projected to exceed $7.6 billion, Carnival expects to fund dividends while continuing to deleverage toward a sub-3X leverage target. The company also left the door open for opportunistic share repurchases, reinforcing the message that excess cash will increasingly flow back to shareholders.

For investors, the dividend’s return represents more than incremental income. It underscores Carnival’s transition into a more normalized, cash-generative phase, supported by strong bookings, high customer deposits and improving financial flexibility. While execution risks remain, the move appears to mark a genuine turning point in the company’s post-pandemic recovery story.

CCL’s Price Performance, Valuation & Estimates

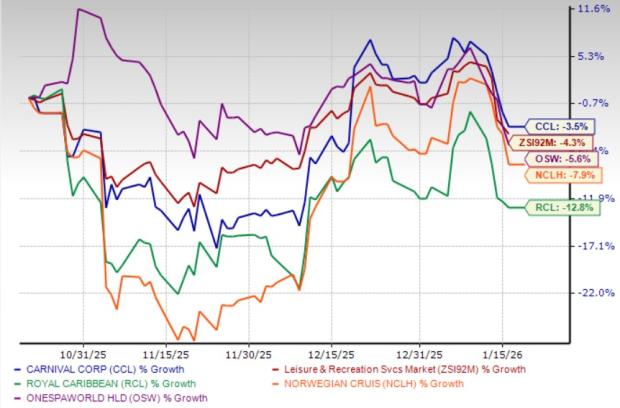

Shares of Carnival have declined 3.5% over the past three months compared with the industry’s fall of 4.3%.

In the same time frame, other industry players, such as Royal Caribbean Cruises Ltd. RCL, Norwegian Cruise Line Holdings Ltd. NCLH and OneSpaWorld Holdings Limited OSW have plunged 12.8%, 7.9% and 5.6%, respectively.

CCL Stock’s Three-Month Price Performance

Image Source: Zacks Investment Research

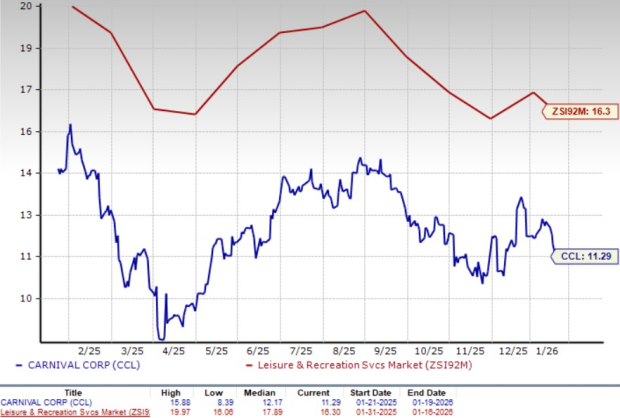

CCL stock is currently trading at a discount. It is currently trading at a forward 12-month price-to-earnings (P/E) multiple of 11.29, well below the industry average of 16.3. Conversely, industry players, such as Royal Caribbean, Norwegian Cruise and OneSpaWorld have P/E ratios of 15.34, 8.17 and 17.19, respectively.

CCL’s P/E Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Carnival’s fiscal 2026 earnings per share has been revised upward, increasing from $2.72 to $2.77 over the past 30 days. This upward trend indicates strong analyst confidence in the stock’s near-term prospects.

Image Source: Zacks Investment Research

CCL currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Carnival Corporation (CCL) : Free Stock Analysis Report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

Norwegian Cruise Line Holdings Ltd. (NCLH) : Free Stock Analysis Report

OneSpaWorld Holdings Limited (OSW) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.