The Caribbean cruise market is heading into 2026 with a clear supply shock. Industry-wide capacity in the region is set to jump sharply, driven largely by competitors redeploying ships into short and mid-length itineraries. For investors, the key question is whether Carnival Corporation & plc CCL can protect pricing and yields as the supply-demand balance tightens.

Management believes it can. On the fourth-quarter 2025earnings call Carnival acknowledged that non-company Caribbean capacity will rise about 14% in 2026, pushing the two-year increase to roughly 27%. Even so, the company’s full-year guidance already incorporates this pressure, with it still forecasting normalized yield growth of around 3% in 2026. That confidence rests on strong booking visibility, with roughly two-thirds of next year’s capacity already sold at historically high prices across North America and Europe, and customer deposits ending 2025 at a record level.

Carnival’s strategy emphasizes revenue optimization over simply filling berths. Management stressed that it is willing to sacrifice marginal occupancy to preserve price integrity, a notable shift from the industry’s historical tendency to discount heavily during capacity surges. This discipline is supported by robust onboard spending trends and continued strength in close-in demand, both of which helped drive higher yields in late 2025.

Diversification also matters. While the Caribbean is a focal point, Carnival’s broad brand portfolio and geographic mix, including European-sourced Caribbean sailings, provide flexibility to absorb regional supply spikes. Add in private-destination initiatives that enhance guest spend and Carnival appears better positioned than in past cycles.

Capacity growth will test the industry, but Carnival’s booking momentum, pricing discipline and portfolio breadth suggest it has a credible path to defending yields in 2026.

How Rivals Are Positioned as Caribbean Supply Swells

Two of Carnival’s closest competitors, Royal Caribbean Cruises Ltd. RCL and Norwegian Cruise Line Holdings Ltd. NCLH, are also navigating the Caribbean capacity surge, but with slightly different playbooks.

Royal Caribbean enters 2026 with outsized exposure to the Caribbean, supported by a steady stream of new ships and its expanding private-destination portfolio, including Perfect Day locations. While these assets enhance onboard and shore-side revenues, Royal Caribbean’s higher capacity growth raises the bar for maintaining pricing discipline if demand softens. Its premium-leaning brand mix and loyalty base help, but incremental supply could pressure yields during peak capacity quarters.

Norwegian faces a more delicate balancing act. With a smaller fleet and a heavier reliance on contemporary and premium brands, Norwegian has less scale to absorb aggressive regional supply growth. While its focus on guest experience and bundled pricing supports onboard spend, Norwegian may be more exposed to promotional activity if the Caribbean market becomes crowded.

Overall, Carnival’s comparatively modest capacity growth gives it a relative advantage against these peers.

CCL’s Price Performance, Valuation and Estimates

Shares of Carnival have gained 18.7% in the past three months compared with the industry’s rise of 12.8%.

Price Performance

Image Source: Zacks Investment Research

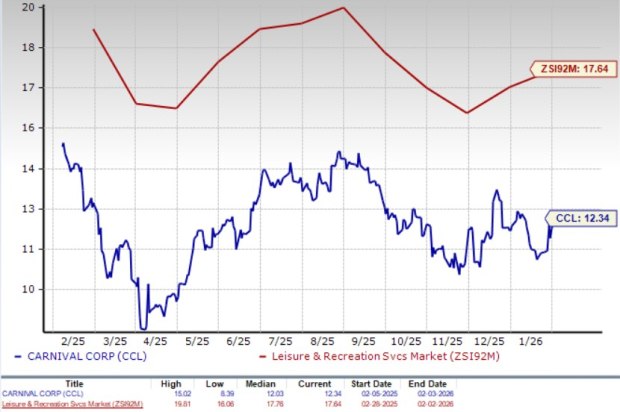

From a valuation standpoint, CCL trades at a forward price-to-earnings ratio of 12.34X, below the industry average of 17.64X.

P/E (F12M)

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for CCL’s 2026 sales and earnings implies a year-over-year uptick of 4.6% and 12.9%, respectively. EPS estimates for fiscal 2026 have decreased in the past 30 days.

Image Source: Zacks Investment Research

CCL currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Carnival Corporation (CCL) : Free Stock Analysis Report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

Norwegian Cruise Line Holdings Ltd. (NCLH) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.