Synchrony Financial SYF is set to report its third-quarter 2024 results on Oct. 16, before the opening bell.

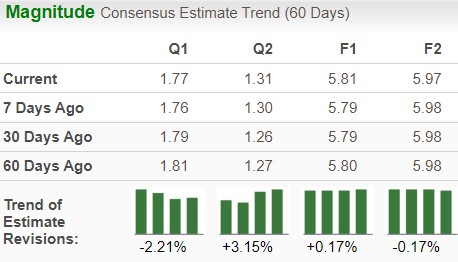

The Zacks Consensus Estimate for third-quarter earnings is currently pegged at $1.77 per share, implying growth of 19.6% from the year-ago reported number. The estimate was revised upward by one analyst in the past week against no movement in the opposite direction, resulting in an increase of 1 cent from $1.76 per share. The Zacks Consensus Estimate for third-quarter revenues is currently pegged at almost $4.5 billion, suggesting a 3.5% uptick from the year-ago actuals.

Image Source: Zacks Investment Research

Stay up-to-date with all quarterly releases: See Zacks Earnings Calendar.

Synchrony beat the consensus estimate for earnings in three of the trailing four quarters and missed once, with the average surprise being 2.8%, as you can see below.

Synchrony Financial Price and EPS Surprise

Synchrony Financial price-eps-surprise | Synchrony Financial Quote

Q3 Earnings Whispers

Our proven model does not conclusively predict an earnings beat for Synchrony this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is not the case here, as you will see below.

Earnings ESP: The company has an Earnings ESP of -2.79%. This is because the Most Accurate Estimate currently stands lower than the Zacks Consensus Estimate of $1.77.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: Synchrony currently carries a Zacks Rank #3.

Now, let’s see how things have shaped up before the third-quarter earnings announcement.

Q3 Factors to Note

Synchrony is expected to have seen advantages in the third quarter from loan receivables, average active accounts and net interest income. However, lower purchase volumes might act as a partial offset.

Our model predicts an increase of more than 6% year over year in interest and fees on loans, boosting the top line. We expect net interest income to rise 4% year over year in the third quarter. However, the Zacks Consensus Estimate for Synchrony’s total purchase volumes for the quarter under review indicates a deterioration of nearly 1.1% year over year, while our model predicts a 0.1% decrease.

SYF is expected to have consistently gained from digital sales volume in the to-be-reported quarter. Both the Zacks Consensus Estimate and our model estimate suggest that the total average active accounts are likely to have risen nearly 4% year over year in the third quarter.

The financial service provider is expected to have witnessed an increase in Average Interest-Earning Assets. The consensus estimate indicates a 10.1% increase in the metric from the year-ago period, whereas our estimate suggests 12% growth. The Zacks Consensus Estimate for the efficiency ratio is pegged at 32.78%, indicating a decline from the prior-year reported figure of 33.2%.

The above-mentioned factors are likely to have benefited the company in the third quarter, positioning it for year-over-year growth. However, Synchrony is expected to have incurred increased information processing, marketing and business development expenses, employee costs and professional fees in the third quarter.

As such, our estimate for total non-interest expenses for the quarter is pegged at more than $1.2 billion, suggesting a 5% increase year over year. Additionally, we expect an increase in provision for credit losses in the quarter under review.

The Zacks Consensus Estimate for the net interest margin is pegged at 14.46%, while our estimate suggests a net interest margin of 14.26%, down from 15.36% achieved a year ago, lowering its profit levels and making an earnings beat uncertain. The net charge-offs are also likely to have substantially risen in the quarter under review.

Price Performance

Synchrony's stock has exhibited an upward movement, gaining a notable percentage in the year-to-date period. It has soared 40.5% compared with the industry’s rise of only 7.4%. Additionally, the stock outperformed the S&P 500 Index, which rallied 21.9% during the same period.

ELV YTD Price Performance

Image Source: Zacks Investment Research

Stocks That Warrant a Look

Here are some other companies from the Finance space, which according to our model, have the right combination of elements to beat on earnings this time around:

Virtu Financial, Inc. VIRT has an Earnings ESP of +6.42% and a Zacks Rank of 1 currently. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for VIRT’s third-quarter 2024 earnings is pegged at 73 cents per share, indicating 62.2% growth from the year-ago quarter’s number.

Virtu Financial’s earnings beat estimates in three of the trailing four quarters and missed the mark once, the average surprise being 9.87%.

Brighthouse Financial, Inc. BHF has an Earnings ESP of +1.22% and a Zacks Rank of 2 currently. The Zacks Consensus Estimate for BHF’s third-quarter earnings is pegged at $4.50 per share, indicating a 7.7% improvement from the year-ago quarter’s figure.

BHF’s earnings beat estimates in three of the trailing four quarters and missed the mark once, the average surprise being 3.8%.

Ameriprise Financial, Inc. AMP has an Earnings ESP of +0.68% and a Zacks Rank of 2 at present. The Zacks Consensus Estimate for AMP’s third-quarter earnings is $8.87 per share, indicating 15.5% growth from the year-ago quarter’s figure.

Ameriprise Financial’s earnings beat estimates in each of the trailing four quarters, the average surprise being 1.55%.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Ameriprise Financial, Inc. (AMP) : Free Stock Analysis Report

Synchrony Financial (SYF) : Free Stock Analysis Report

Virtu Financial, Inc. (VIRT) : Free Stock Analysis Report

Brighthouse Financial, Inc. (BHF) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.