Hasbro, Inc.’s HAS flagship franchise, Magic: The Gathering (“MAGIC”), is rapidly evolving beyond its traditional tabletop roots to become a highly profitable, multi-platform ecosystem. The company’s first-quarter 2026 results highlighted the strength of this transformation, as sustained demand for MAGIC, record product launches, growing player engagement and expanding partnerships fueled strong performance across the Wizards of the Coast and Digital Gaming segment.

In the first quarter of 2026, Hasbro's Wizards of the Coast and Digital Gaming segment delivered revenues of $582 million, up 26% year over year. Magic: The Gathering was the key driver, with revenues rising 36%. The segment also generated an operating profit of $298 million and an operating margin of 51.2%, highlighting the profitability of Hasbro's gaming-led strategy.

Hasbro is also leaning harder into digital expansion. Management highlighted that MAGIC ARENA will feature full digital rights for the upcoming Marvel Super Heroes launch through its partnership with Disney. This is important because it brings Hasbro closer to a one-to-one ecosystem where players can buy physical cards and engage with the same content digitally.

The broader strategy is clear, using Universes Beyond partnerships, digital play, collectibility and social formats like Commander to bring more fans into MAGIC and keep them engaged across platforms. Management said Universes Beyond has been one of MAGIC's most successful new-player acquisition initiatives, while digital iterations of MAGIC are expected to lean further into collectibility, tradability and multiplayer experiences over the next few years.

The question for investors is whether this digital expansion can create a longer runway beyond the current surge in tabletop demand. So far, the signs are encouraging. MAGIC is driving revenue growth, margin expansion and stronger cash generation for Hasbro. If the company can successfully scale MAGIC ARENA and future digital experiences alongside its high-margin tabletop business, MAGIC could remain one of Hasbro's most important long-term growth pillars.

Key Competitors to Watch in Digital Gaming and Franchise Expansion

Two notable competitors to monitor as Hasbro expands the Magic: The Gathering ecosystem across digital gaming, entertainment and consumer products are Mattel, Inc. MAT and JAKKS Pacific, Inc. JAKK.

Mattel is increasingly pursuing a strategy that mirrors Hasbro’s efforts to transform iconic brands into multi-platform franchises. Management recently emphasized a brand-centric operating model designed to monetize intellectual property across toys, entertainment, digital gaming, mobile experiences and location-based attractions rather than relying solely on traditional toy sales. Mattel is leveraging franchises such as Barbie, UNO and Hot Wheels across digital platforms, with management highlighting strong consumer engagement for branded experiences on Roblox and Fortnite.

JAKKS Pacific is expanding aggressively through licensed entertainment properties, digital creator ecosystems and fan-driven merchandise. The company recently unveiled a large-scale Anime, Manga and Digital Creator platform designed to capitalize on one of the fastest-growing segments of global entertainment. Management expects the initiative to combine collectibles, merchandise, costumes, tech accessories and direct-to-consumer engagement while leveraging partnerships with major anime franchises and digital creators. Similar to Hasbro's Universes Beyond strategy, JAKKS Pacific is using established fan communities and entertainment brands to drive engagement across multiple product categories and distribution channels.

HAS’ Stock Price Performance & Valuation Trend

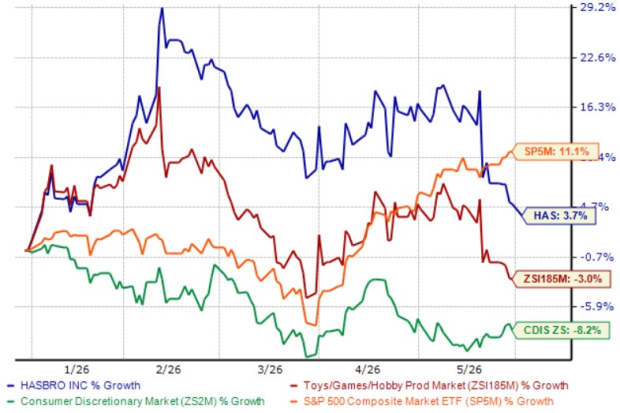

Shares of this games and toys manufacturer have gained 3.7% year to date, outperforming the Zacks Toys - Games - Hobbies industry and the broader Consumer Discretionary sector, but underperforming the S&P 500 Index.

Image Source: Zacks Investment Research

HAS stock is currently trading at a premium compared to its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 13.83, as evidenced by the chart below.

Image Source: Zacks Investment Research

Earnings Estimate Revision of HAS

HAS’ earnings estimates for 2026 and 2027 have trended upward in the past seven days to $5.96 and $6.42 per share, respectively. The revised estimates for 2026 and 2027 imply year-over-year growth of 7.6% and 7.7%, respectively.

Image Source: Zacks Investment Research

HAS stock currently flaunts a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpHasbro, Inc. (HAS) : Free Stock Analysis Report

Mattel, Inc. (MAT) : Free Stock Analysis Report

JAKKS Pacific, Inc. (JAKK) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.