Cameco CCJ reported first-quarter 2026 results on Tuesday. Total revenues were up 7% year over year to CAD 845 million ($616 million). Adjusted earnings rose 194% year over year to CAD 0.47 per share or 34 cents. Cameco beat the Zacks Consensus Estimate on both counts.

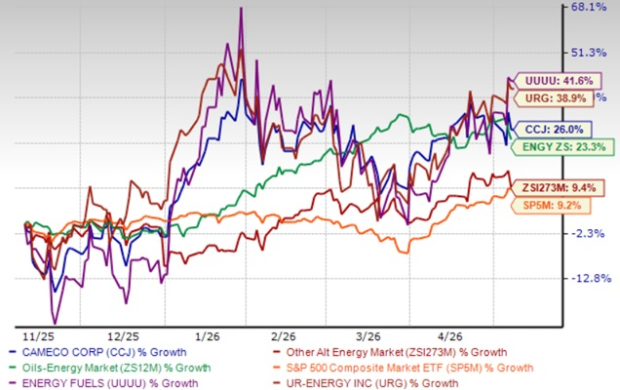

In the past six months, Cameco shares have gained 26% compared with the industry’s 9.4% growth. Meanwhile, the broader Oils-Energy sector has moved up 23.3%, while the S&P 500 has climbed 9.2%.

Cameco’s 6-Month Price Performance vs. Industry, Sector & Peers

Image Source: Zacks Investment Research

However, Cameco has lagged peers like Ur-Energy Inc. URG and Energy Fuels UUUU, which have gained 41.6% and 38.9%, respectively.

Let us delve deeper into the company’s first-quarter results and long-term prospects before assessing whether to buy, hold or sell the stock.

Digging Deeper Into Cameco’s Q126 Results

Uranium production in the quarter was up 3% year over year to 6.2 million pounds. The company sold 7.8 million pounds of uranium, 13% higher than the first quarter of 2025.

Cameco’s uranium revenues increased 15% to CAD712 million ($520 million) on higher volumes and prices. While the average U.S. dollar spot price for uranium increased 34% on a year-over-year basis, the Canadian dollar average realized price rose 2% due to the impact of fixed-price contracts compared to 2025 as well as the lagging impact of spot price changes on the portfolio

In Fuel Services, production volume was down 15% year over year to 3.3 million kgUs while sales volume rose 17% to 2.8 million kgUs. The segment reported a 1% dip in revenues to CAD 134 million ($98 million), with higher volumes being offset by a 17% decline in average realized prices.

Cameco’s total revenues were up 7% to CAD 845 million ($616 million) reflecting improved performance of the uranium segment which helped offset lower revenues in Fuel services.

Total cost of sales increased 4.6% to around CAD 543 million ($397 million). In the uranium segment, costs climbed 9% due to a higher sales volume partially offset by a 3% decrease in unit cost of sales. Costs in Fuel services segment increased 35% driven by the 17% increase in sales volume and a 16% increase in the average unit cost of sales. The company stated unit cost of sales could be impacted by the imposition of tariffs.

Adjusted EBITDA rose 44% year over year to CAD 509 million ($372 million). Cameco’s adjusted earnings surged 194% year over year to CAD 0.47 (34 cents) per share in the quarter. This was mainly attributed to higher revenues and stronger equity earnings from its 49% interest in Westinghouse Electric Company.

Cameco's 2026 Outlook Points to Lower Uranium Revenues

Uranium production is projected between 19.5 million pounds and 21.5 million pounds for 2026. Cameco expects uranium deliveries of 29–32 million pounds. Uranium revenues are projected in the range of CAD 2.54–2.73 billion, based on an average realized price of CAD 85–89 per pound. At the midpoint, this implies a roughly 7% year-over-year decline due to lower volumes. The fuel services segment is expected to fare better, with revenues projected at CAD 590-630 million, suggesting a 9% increase from 2025 levels.

Cameco’s total revenue guidance for the year is CAD 3.13-3.37 billion. The midpoint suggests a 7% decline from the CAD 3.482 billion in revenues reported in 2025.

Cameco expects its share of adjusted EBITDA from Westinghouse to be $370-$430 million for 2026.

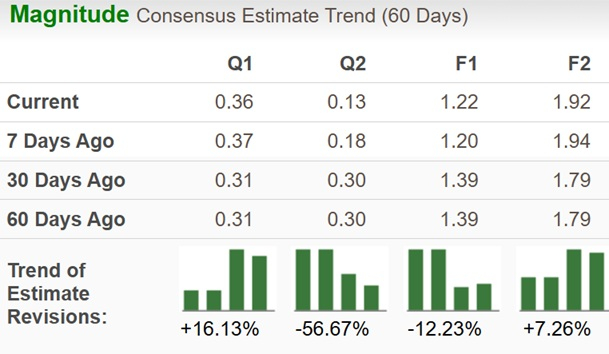

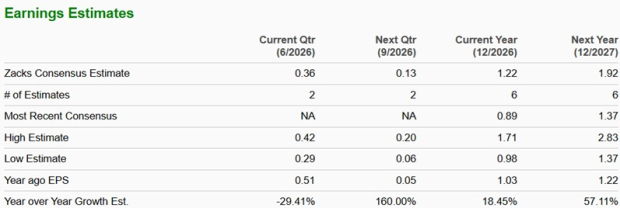

CCJ’s Estimates Suggest Growth, Revisions Seem Mixed

The Zacks Consensus Estimate for Cameco’s earnings for 2026 has moved down over the past 60 days, while the same for 2027 has moved up, as shown in the chart below.

Image Source: Zacks Investment Research

The consensus estimate for Cameco’s earnings for 2026 indicates year-over-year growth of 18.5%. The same for 2027 implies growth of 57.11%.

Image Source: Zacks Investment Research

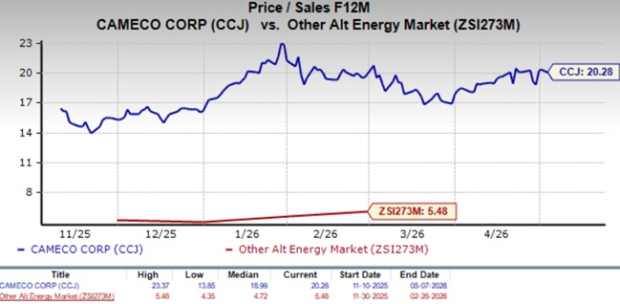

Cameco’s Valuation Looks Stretched

CCJ stock is trading at a forward price-to-sales ratio of 20.28 compared with the industry’s 5.48. CCJ’s Value Score of F suggests that the stock is not so cheap and a stretched valuation at this moment.

Image Source: Zacks Investment Research

Energy Fuels is trading higher at 22.78 while Ur-Energy is a cheaper option, trading at 4.62.

CCJ’s Long-Term Story Intact

Cameco continues to strengthen its long-term portfolio. It has long-term obligations to deliver about 230 million pounds of uranium, translating to average annual deliveries of around 28 million pounds over the next five years. In the Fuel Services segment, strong demand and elevated UF6 conversion prices have enabled Cameco to secure additional long-term contracts. Total contracted volumes now stand at roughly 83 million kgU of UF6, offering solid visibility into future revenues

Cameco’s uranium production capacity is among the largest globally, accounting for nearly 15% of worldwide output. The company is investing to expand production and capture favorable market conditions, including extending Cigar Lake’s mine life to 2036 and ramping up output at McArthur River and Key Lake toward their licensed annual capacity of 25 million pounds (100% basis).

Rising energy security concerns, geopolitical tensions and the global push for low-carbon energy continue to create structural tailwinds for nuclear power. With low-cost, high-grade assets and a diversified nuclear fuel cycle portfolio, Cameco is well-positioned to benefit from sustained growth in nuclear energy demand.

Should You Buy Cameco Stock Now?

Supported by a strong balance sheet, the company is making investments to boost its capacity to capitalize on the expected surge in uranium demand. However, new investors can wait for a better entry point, considering the premium valuation and mixed earnings estimate revisions. The stock currently carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpCameco Corporation (CCJ) : Free Stock Analysis Report

Ur Energy Inc (URG) : Free Stock Analysis Report

Energy Fuels Inc (UUUU) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.