Credit: Shutterstock photo

Credit: Shutterstock photoNote: This article is part of an analytical report I wrote on Cameco. The report is too long to publish here, so I decided to only include the main sections, which is the valuation of the company, and an investigation of the balance sheet if the company were to lose the tax case. If you are interested in reading the full report (including an analysis of the company, outlook for the uranium industry, competitive advantages of Cameco etc.), you candownload it for free here.

Key Metrics

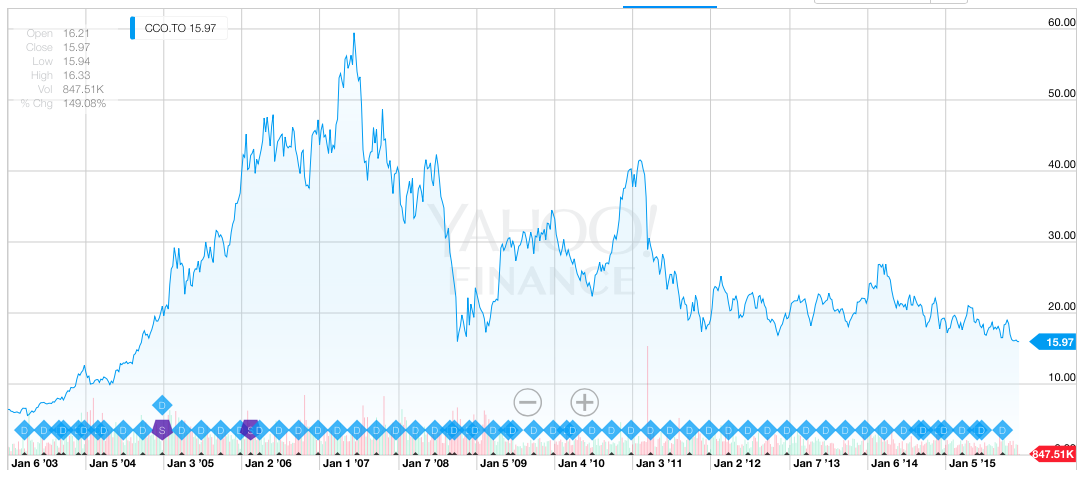

Cameco Share Price Chart (Toronto Exchange)

Source: Yahoo! Finance.com

Investment Thesis

The investment thesis for Cameco is simple. Going forward, the world will need more electricity and, despite its bad reputation, uranium is going to be an important part of the energy mix.

The uranium spot price is currently $USD 36 per pound, and Cameco's CEO, Tim Gitzel, estimates that the price needs to be at least $60-70 to spur new supply.

The current supply destruction, coupled with strong expected demand in the future, creates a bullish case for uranium. However, after Fukushima, there has been an oversupply of secondary uranium in the market and this supply needs to clear before we can see an upward move in price. Unfortunately, this might take a few more years, but when it happens, the move in price can be explosive (if history is an indicator).

Based on my model I estimate that the fair value per share of Cameco is around $CAD 30.

Valuation

I usually use a discounted cash flow model to estimate the fair value of a company. However, using a DCF for Cameco is very challenging because the company is operating in a very cyclical and capital-intensive industry.

A more suitable method is therefore to value the company based on future earnings power. I do this by estimating earnings in a "normal" year in the future (in this example 2018), and then applying a reasonable multiple.

In the scenario I have laid out below, I assume that uranium prices have rebounded by 2018 and that the profits are substantially higher than today. After all, I invest in Cameco because I believe the uranium industry will eventually enter into a new bull market.

My analysis is based on prudent assumptions about future revenues, which are determined by sales volume and the price Cameco can get for its uranium. I subsequently make a forecast about operating profits ((EBIT)) and apply an EV/EBIT multiple.

The key to remember is that I have based my analysis on what I believe are prudent assumptions.

Splitting Revenues By Segment

Cameco has three different operating segments: Uranium, Fuel Services and NUKEM. I decided to split my analysis into those three segments.

Uranium Segment

As far as I am aware, Cameco does not provide sales forecasts, and it's therefore challenging to estimate sales in 2018. A solution is to assume that they will sell as many pounds of uranium in 2018 as they did in 2014. This is likely an underestimation, if we expect uranium to be in a bull market in 2018, but it's a better alternative than overestimating. Prudence is what we are aiming for.

Sales volume in 2014 was 33.9 million pounds, and we therefore start with assuming that the company will sell 33.9 million pounds in 2018.

Cameco's uranium sales are targeted at a ratio of 40:60 fixed contracts versus spot contracts. This means the company is aiming to sell 40% of its uranium under fixed contracts and 60% in the spot market. For our 2018 estimate, this means 13.6 million pounds will be fixed contracts, and 20.3 million pounds will be spot contracts.

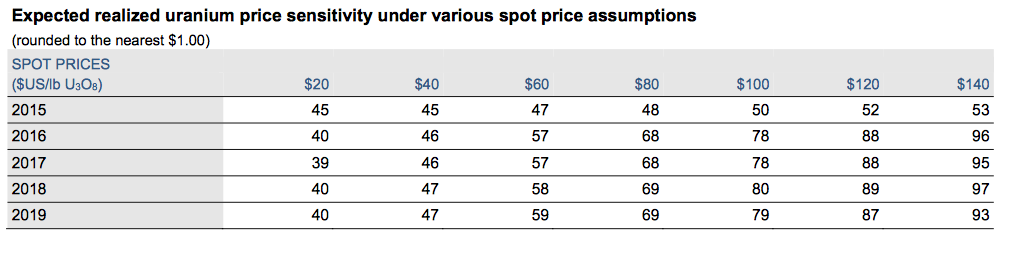

Cameco has a table in its quarterly report showing how long-term contracts would react to spot price changes (they highlight that these are not forecasts , but how the contract portfolio, as it looks at September 30th, 2015, would change as spot changes).

Source: 2015 Q3 Report

I use a spot uranium price of $60 for 2018, because according to industry experts that's more or less the minimum price level that's needed for new producers to enter the market, i.e. it's the average marginal cost. Under such a scenario Cameco would make $58 per fixed contract (ref. chart above). These prices are in USD, however Cameco's figures are in CAD, so we have to convert them (using an average ratio of historical CAD to USD uranium prices).

If we assume that in 2018 Cameco will sell 13.6 million pounds of uranium at a fixed price of $USD 58 and 20.3 million pounds at a spot price of $USD 60, we get revenues of $CAD 2,182 million for the uranium segment.

Fuel Services

The next step is to forecast sales for the Fuel Services segment of the company.

Again, Cameco does not provide sales forecasts so I use the realized sales volume in 2014, 15.5 million kgU. This is an historically low figure (chart below), but again we are being prudent and don't want to overestimate 2018 sales.

For the price per kgU I use the average over the last six years (the oldest data I found), rather than a future estimate. That's because I was not able to find a reasonable estimate for price per kgU and furthermore because the price has fluctuated very little over the years (between $CAD 16.7-19.7). The average price was $CAD 17.7.

If I assume Cameco will sell 15.5 million kgU in 2018 at a price of $CAD 17.7 per kgU, the estimated revenues in 2018 for the fuel services segment will be $CAD 275 million.

Source: Morningstar.com

NUKEM

Again we assume that the 2018 sales volume will equal that of 2014, which was 8.1 million pounds. The assumed price per pound is the same as above, $USD 60 ($CAD 65, using the average historical CAD to USD uranium price ratio).

If we assume NUKEM will sell 8.1 million pounds of uranium in 2018 and the average price is $USD 60 per pound, the estimated revenues are $CAD 528 million.

Operating Income ((EBIT)) Assumptions

Now that I have an estimate for total revenues for 2018 ($CAD 2,986 mil), I have to estimate operating earnings (or EBIT), as I am using an EV/EBIT multiple to value the company.

This is a challenging task because the operating income margin for all the segments is different (the uranium segment is a higher margin business than the other two segments).

I could try to estimate operating earnings by firstly estimating gross profits in each of the segments, then work my way downwards to operating income. I tried going down that route, but I realized I did not have sufficient information to make reasonable assumptions.

I therefore decided to use the company's average operating margin over the last decade. Historically, the operating margin has on average been 18.1%, if we exclude the outlier years 2009 (they sold part of their business which increased income) and 2014 (substantial impairment charges). If we expect the uranium price to rebound to $60 by 2018, 18.1% could turn out to be a conservative number. During years where the uranium price was strong (2007, 2010 and 2011) the margin was higher. But again, we are being prudent.

If we assume that the revenues in 2018 will be $CAD 2,986, and apply an operating income ((EBIT)) margin of 18.1%, we get an operating income of $CAD 540 million in 2018 .

The next step will be to find the Enterprise Value of the company by applying an EV/EBIT multiple to the operating income figure.

Applying a multiple

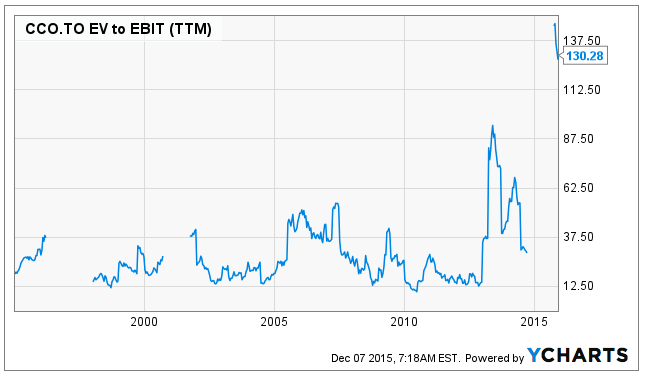

Historically the EV/EBIT multiple of Cameco has been very volatile (chart below). During "normal" times the multiple seems to be fluctuating between 12.50 (lower bound) and 37.50 (upper bound), with a midpoint of 25.

If I apply an EV/EBIT multiple of 25 to my EBIT calculation for 2018 (~$CAD 540m), I get an enterprise value of around $CAD 13.5 billion, which equates to a value per share of $CAD 30.45 (using the most recent numbers for cash and long term debt to estimate equity value, and 396m shares outstanding).

With the share price (in Canada) currently trading just under $CAD 16, the potential upside is around 92%.

If we were to use a more prudent estimate of EV/EBIT, say 20, the fair value drops to $CAD 23.6 per share, which gives a potential upside of 49%.

Valuation Sanity Check

When using a model to value a company, there are many assumptions involved, and the more assumptions we use, the more uncertain the outcome becomes. A common saying is "crap in, crap out".

I tried to mitigate the inherent uncertainties of forecasting by using prudent metrics. I assumed that revenues in 2018 will be $CAD 2,986, which is only a 25% rise in revenues from 2014 (compound annual growth rate of 5.6%). Based on trailing-twelve-month revenues as at 30 September 2015 ($CAD 2,669 mil), it's only a 12% rise.

By way of comparison, when the last uranium bull market was in full swing, Cameco's revenues increased 40% in 2006, 26% in 2007, and 24% in 2008.

Despite my conservative assumptions, I wanted to double-check that they were not unreasonable. To do this I performed a simple P/E multiple analysis based on historical EPS figures.

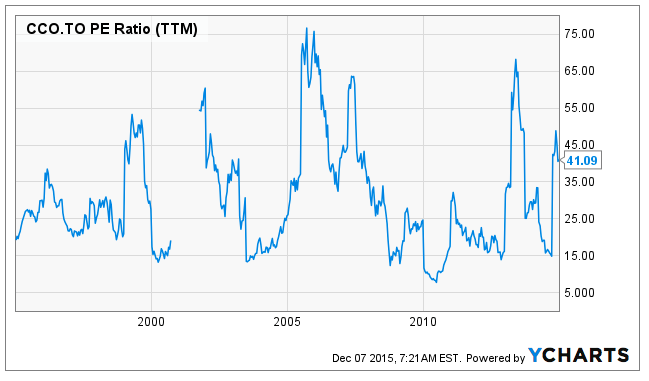

Below is a chart showing Cameco's historical P/E ratio. The chart does not include 2015 because there was a huge spike in the P/E in the middle of the year and reading the chart becomes impossible if we include this aberration.

Cameco's P/E ratio has been very volatile, but it seems that a P/E of 25 is a reasonable multiple to use (as with EV/EBIT), as it is more towards the lower end of the chart.

If we look at the historical earnings per share of Cameco (chart below), it's around $CAD 1.05, if we exclude 2009 and 2014, which I explained above were outliers.

Applying a 25 P/E multiple to an average EPS of $1.05 gives us a share price of $CAD 26.25, which is not far from the fair value we found above ($CAD 30.45 per share).

If we expect a bull market in 2018, an EPS of $1.05 is likely a conservative measure. Nevertheless, this model shows us that my fair value of estimate of $CAD 30.45 is a reasonable estimate.

Lastly, according to the Financial Times, the median 12-month price target for Cameco (based on 16 analyst forecasts) is $CAD 23.75, with a high estimate of $29 and a low estimate of $16.

Summary of Valuation

Based on my analysis, I conclude that $CAD 30.45 is a reasonable fair value per share. However, this analysis is based on a prudent measure of sales volume, price and operating margin. If we enter a sustained uranium bull market, Cameco's share price is likely to go higher.

What If They Lose The Tax Dispute?

A question that is surely on every Cameco shareholder's mind is "what if the company loses the tax dispute". It's arguably the biggest risk that the company faces. I therefore wanted to get an understanding of how a potential loss would affect the balance sheet of the company.

My personal opinion on the matter is that it's impossible to predict the outcome of the case, but I am leaning towards Cameco losing. That's because of my prudent nature and because I believe the government is a tough opponent to beat. From what I understand, Cameco has not done anything wrong from a legal standpoint (the transfer pricing was based on legitimate contracts), but if the government wants its pound of flesh, it is likely to get it.

I do believe that some of it is priced into the stock, but I believe that if they lose, the stock will go lower. It's the logical and prudent conclusion.

I was in touch with the company's investor relations department and they explained how the company would be affected if they lost the case. Below I have tried to lay out how the balance sheet would look if that were to happen. Note that I use the last available balance sheet (as per 30 September 2015). When the court decision is made the balance sheet will naturally be different.

The company told me that if they have to pay penalties of $1.5 billion (current estimate) it would first be charged through the P&L as an expense. This will likely lead to a massive net loss that year.

The loss would subsequently have to be charged against equity on the balance sheet (i.e. the equity would be decreased by the net loss that year, which I assume is $1.5 billion).

If we assume that the company will borrow the full $1.5 billion, long-term debt will increase by $1.5 billion. In reality this will likely not be the case because some of it will be charged against cash, long-term receivables and deferred tax assets, but it's the prudent assumption.

Currently, total liabilities as a percentage of total assets is only 36%, and long-term debt as a percentage of total assets is only 17%.

Source: Cameco Q3 2015 report

Based on how the balance sheet looks today, if the company were to increase long-term debt by $1.5 billion, and decrease equity by $1.5 billion, the figures actually don't look terrible.

Total liabilities to total assets would increase to 54% (equity would be 46%), while long-term debt to total assets would increase to 35%.

Conclusion

I do believe that if Cameco loses the case, the stock will fall further, despite some of the downside already being priced in. In such a scenario, the balance sheet would be weakened, but I don't believe to a point where Cameco is at risk of bankruptcy.

The final outcome will undoubtedly be different from the scenario above because the case has not yet gone to court. When that finally happens the balance sheet will look different, and the company's net profits, cash position, amount of penalties paid to date, the ratio of liabilities to equity etc. will also be different. These factors are impossible to predict, but the above example serves as a possible scenario.

Relative valuation

In the section above, I presented Cameco's historical P/E ratio and EV/EBIT ratio. Based on these two metrics the company does not currently seem very cheap. But these metrics are misleading because there have been several one off charges over the last few years (as a result of the difficult industry conditions), which have depressed income. That can be seen from the huge fluctuations we've seen in the P/E and EV/EBIT multiples.

But if we look at the Price/Sales ratio and Price/Book ratio (charts below), we see that they are at multi-year lows. The Price/Sales ratio has been consistently declining over the last few years and is now at levels last seen at the bottom of the financial crisis, and in the period before the uranium bull market of the last decade really took off (2004/2005).

We can see a similar trend in the Price/Book ratio, however today's level is even lower than during the financial crisis, and we have to go back around 11 years to see a similar Price/Book ratio.

Looking at Price/Sales and Price/Book in isolation is not enough to conclude if a company is undervalued or not. But in this case, we have already established that the company's fair value is around $CAD 30 per share, and these low multiples therefore strengthen the argument that Cameco is currently undervalued.

Closing Thoughts

The uranium industry has been tough over the last 4-5 years, but eventually a new bull market will emerge. Cameco is a solid company and has weathered the downturn well, especially compared to its competition. The company currently looks undervalued based on several metrics and I estimate that the fair value per share is a little above $CAD 30, which gives the share a potential 92% upside.

The tax dispute is like a dark cloud hanging over the company, but much of it should already be priced in the stock (although not all of it), but if the company were to lose the case I believe their balance sheet is strong enough to weather the storm.

I own Cameco shares and I am considering buying more at these levels. It might take a few years, but I believe that eventually my patience will be rewarded.

See also ConAgra Is Unlocking Growth on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}