The Coca-Cola Company KO is slated to report third-quarter 2024 earnings on Oct. 23, before the opening bell. The company is expected to register a year-over-year top-line decline and flat bottom-line results when it reports third-quarter numbers.

Stay up-to-date with all quarterly releases: See Zacks Earnings Calendar.

The Zacks Consensus Estimate for third-quarter earnings is pegged at 74 cents, suggesting no change from the prior-year quarter’s reported figure. The consensus mark for earnings has moved down by a penny in the past 30 days. For quarterly revenues, the consensus mark is pegged at $11.6 billion, implying a 2.9% decline from the year-ago quarter's reported figure.

The Atlanta, GA-based company has been reporting steady earnings outcomes, as evident from its positive top and bottom-line surprise trends in the trailing four quarters. KO has a trailing four-quarter earnings surprise of 4.7%, on average. Additionally, the top line has surpassed the Zacks Consensus Estimate in the trailing six quarters. Given its positive record, the question is, can KO maintain the momentum?

Image Source: Zacks Investment Research

Earnings Whispers

Our proven model conclusively predicts an earnings beat for Coca-Cola this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Coca-Cola has a Zacks Rank #3 and an Earnings ESP of +0.79%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Key Trends in Focus Ahead of KO's Q3 Earnings Release

Coca-Cola has shown resilience, supported by positive business trends, such as a robust brand portfolio, investments and revenue growth in its segments. This growth has been driven by improved pricing/mix and volume increases. Volume gains have been notable across at-home and away-from-home channels, reflecting value share improvements.

In the third quarter, Coca-Cola’s volumes are expected to have benefited from strong momentum in emerging and developed markets. Volume growth is likely to have been driven by categories such as trademark Coca-Cola, sparkling flavors, nutrition, juice, dairy, plant-based beverages, and hydration, sports drinks, coffee and tea.

We anticipate strong volumes and favorable price/mix trends to have fueled the company’s third-quarter performance. Our model forecasts a 5.7% year-over-year increase in organic revenues for the third quarter, driven by a 5.1% rise in price/mix and a 0.6% increase in concentrate sales.

Coca-Cola’s third-quarter results are expected to reflect gains from innovations and increased digital investments. E-commerce has surged, with growth rates doubling in many countries. Coca-Cola has accelerated investments in digital capabilities, enhancing consumer connections and piloting digital initiatives to capture online demand, likely boosting third-quarter sales.

Despite favorable volume trends in most markets, macroeconomic challenges are expected to have impacted KO’s third-quarter performance. Factors such as low consumer confidence in China, geopolitical and economic instability in Eurasia and the Middle East, and high inflation in Argentina are expected to have weighed on Coca-Cola's top-line performance.

CocaCola Company (The) Price and EPS Surprise

CocaCola Company (The) price-eps-surprise | CocaCola Company (The) Quote

In the previousearnings call management noted that inflation was normalizing in developed markets, but developing and emerging markets continue to experience high inflation, leading to elevated pricing and currency headwinds. These inflationary pressures and currency fluctuations are expected to have affected some segments in the third quarter.

Coca-Cola projects a 4% impact on third-quarter comparable revenues from currency headwinds, with acquisitions, divestitures and structural changes reducing revenues by 4-5%. Comparable earnings per share are expected to face an 8% currency headwind, with a 1-2% negative impact of acquisitions and structural changes.

Our model estimates a 4% impact on third-quarter revenues from currency headwinds, and a 4.9% impact of acquisitions, divestitures and structural adjustments.

Price Performance & Valuation

Coca-Cola’s shares have exhibited an uptrend, rising as much as 18.7% in the year-to-date period. The stock has surpassed the broader industry and the Consumer Staples sector’s growth of 11.5% and 8.5%, respectively. However, the KO stock has underperformed the S&P 500 index, which grew 22.6% in the same period.

KO Stock’s YTD Performance

Image Source: Zacks Investment Research

Coca-Cola stock also outperforms its competitors, including PepsiCo PEP and Keurig Dr Pepper KDP, which have risen 2.8% and 9.5%, respectively, in the year-to-date period. The KO stock compares favorably against Monster Beverage’s MNST decline of 7.3% in the same period.

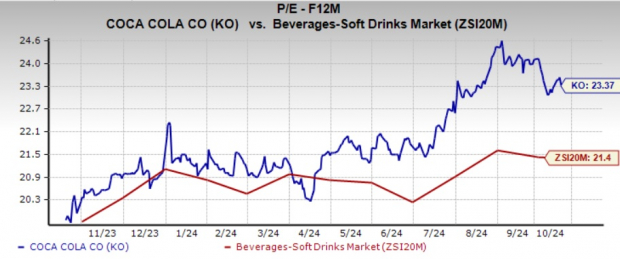

From the valuation standpoint, KO trades at a forward 12-month P/E multiple of 23.37X, exceeding the industry average of 21.4X and the S&P 500’s average of 22.2X. Coca-Cola’s valuation appears quite pricey.

Coca-Cola undoubtedly commands a high valuation, reflecting its strong market positioning, brand power and long-term growth potential compared with other non-alcoholic beverage companies. However, we believe that its valuation is too stretched at this time.

Image Source: Zacks Investment Research

Investment Thesis

Coca-Cola has been a dominant force in the beverage industry, with more than 40% market share of the non-alcoholic beverage market. KO’s strong market presence, marketing prowess and commitment to innovation have been aiding its performance. The company’s more than 4,700 products and 500 brands, ranging from sodas to energy drinks, highlight its strong market position.

KO’s leading market position, diverse product portfolio, and strategic focus on innovation and digital expansion place it well for long-term growth. However, near-term challenges like rising inflationary pressures, macroeconomic disruptions across some markets and adverse currency rates persist.

Conclusion

Regardless of what course the KO stock takes after the third-quarter 2024 earnings results, it is still a solid long-term buy due to its robust profitability and expanding global presence. Prospective investors may carefully evaluate the current valuation before investing. If you already have the KO stock in your portfolio, hold on, as the upcoming earnings report is expected to affirm the company’s strong performance.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpCocaCola Company (The) (KO) : Free Stock Analysis Report

PepsiCo, Inc. (PEP) : Free Stock Analysis Report

Monster Beverage Corporation (MNST) : Free Stock Analysis Report

Keurig Dr Pepper, Inc (KDP) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.