Sometimes timing isn't ideal. Fintech Marqeta (NASDAQ: MQ) went public in the summer of 2021, just months before market sentiment toward most high-growth and technology stocks collapsed. The stock is down roughly 70% from its highs, making it a "loser" for just about anyone who has purchased shares.

The dirty secret of investing is that your risk in an investment is less when the share price falls! Obviously, the company needs to deliver the goods through solid execution and growth, but the risk versus reward is better when the price is lower. In Marqeta's case, the stock price has fallen enough to create a tasty opportunity for investors.

What does Marqeta do?

Payments are a straightforward process from the consumer's standpoint. You swipe your card, and the money moves from your bank account or credit card issuer to the merchant. But there's more to it underneath the surface. Multiple parties receive and send information, and there's traditionally not a lot of flexibility. It's a binary system where the money goes in or out.

Image source: Getty Images.

Apps and services are coming out that can make sophisticated payments, but how do they do it when the existing payment networks are rigid? Imagine you order lunch from food-delivery service Doordash; how can the driver pick up the food on your behalf? How can the customer pay without the risk of the driver adding their lunch to your bill?

Marqeta is a modern-card issuing platform that lets companies build custom payment solutions with Marqeta's application programming interface (API). Marqeta's software links new payment applications like the Doordash example above and the traditional payment networks, making these creative applications possible.

Why the business is about to grow at warp speed

Marqeta takes a small percentage of every transaction its platform powers. While this can make revenue more volatile, it's generally a good thing over the long term because the company can grow with its customers.

Fellow fintech company Block (formerly Square) is currently Marqeta's largest customer, making up 68% of revenue in the most recent quarter, third-quarter 2021. While Block and Marqeta have an agreement through 2024, customer concentration can be a risk that investors need to consider.

The good news is that Marqeta's dependence on Block could ease over the next couple of years. The company has a stable of rapidly growing customers, including Affirm, Uber, and others. Affirm grew transaction volume 115% in its most recent quarter, while Uber grew bookings 51% year over year in its most recent quarter. Marqeta even came out in early February and raised expectations for its fourth-quarter 2021 report beyond its original forecast.

Marqeta should directly benefit from the strong growth of its customers, many of which are innovative companies themselves. Let's hope this will help lessen Marqeta's reliance on Block, though investors won't find out until future quarters play out. In the meantime, the company has no trouble growing, currently putting up 79% year-over-year revenue growth through the first nine months of 2021.

The stock's valuation is compelling

It's easy for me to sit here and tell you that Marqeta's valuation has gotten cheaper over the past several months. That tends to happen when stocks fall 70%. But the take-home point here is just how cheap the stock has gotten.

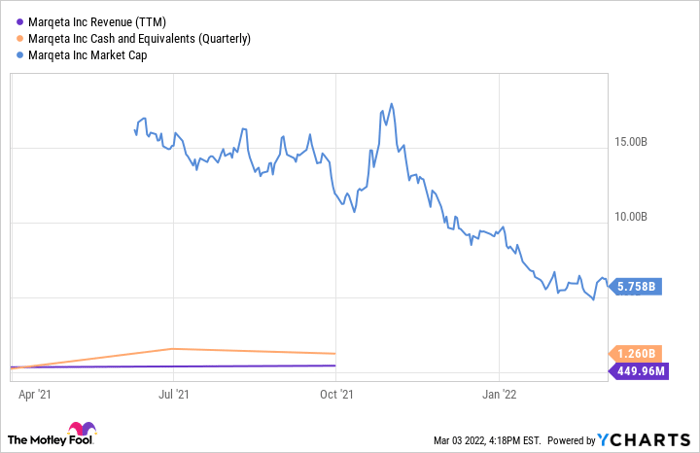

Marqeta's market cap has fallen to less than $6 billion while doing $450 million in revenue over the past 12 months. The stock's price-to-sales ratio (P/S) is 13, which doesn't seem like a bargain until you consider that the company has $1.26 billion in cash and no debt. If you subtract the cash from Marqeta's market cap, the business itself trades at a P/S of just over 10.

MQ Revenue (TTM) data by YCharts

For the money, you're getting a business growing revenue at 79% over 2020. Additionally, Marqeta's non-GAAP EBITDA (earnings before interest, taxes, depreciation, and amortization) was only slightly negative, losing $5 million in its most recent quarterly earnings report. In other words, the business seems well funded to continue growing without worrying about debt or issuing more shares to raise funds.

Investor takeaway

It seems like the company has a path to profitability with low losses and a model where Marqeta grows with its customers. The stock could benefit from a boost in sentiment once Marqeta turns profitable, along with an eventual broader recovery for growth stocks.

Buying into the pain of stocks selling off is never fun, and nobody knows when the bottom is or when a rebound will occur. That's why managing your risk and exercising patience can require superpowers for investors. Marqeta's fundamentals show the company's potential -- now it's a matter of time and execution.

10 stocks we like better than Marqeta, Inc.

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Marqeta, Inc. wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of January 20, 2022

Justin Pope owns Affirm Holdings, Inc. and Marqeta, Inc. The Motley Fool owns and recommends Affirm Holdings, Inc., Block, Inc., and DoorDash, Inc. The Motley Fool recommends Marqeta, Inc. and Uber Technologies. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.