Target TGT stock went on a huge run before covid and it then soared for roughly a year and a half as consumers flocked to its one-stop-shop offerings, e-commerce options, and more.

Some investors might be worried they missed their chance on Target. Yet, TGT stock is currently sitting at enticing levels for those with longer-term horizons, especially considering its solid fundamentals.

One-Stop-Shop

Target’s e-commerce growth helped business boom during the heart of the pandemic and its offerings will see it succeed in a retail age where customers want as many options as possible. Last year, its comparable digital sales soared 145%, with same-day services up 235%. These same-day offerings include in-store pickup, Drive Up, and its Instacart-style Shipt unit.

Along with its new-age shopping push, the Minneapolis-based retailer has focused even more heavily on its own in-house brands for fashion, furniture, food, and more. TGT’s various store brands succeed because of its ability to adapt and stay on-trend, while remaining affordable. Target’s growing slate of in-house brands have helped separate it from rivals like Walmart WMT and Costco COST within some key demographics.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Recent Results & Outlook

Despite coming up against an extremely difficult to compete against year of 20% revenue expansion (vs. around 3.5% sales growth for several years leading up to 2020), Target continued its rapid sales growth during the first three quarters of 2021. For instance, TGT reported 23% sales growth in the first quarter, followed by 10% in Q2 and over 13% in the third quarter.

Target’s Q3 comps popped 13% on top of 21% expansion in the year-ago quarter. Last quarter’s growth was driven by a big jump in in-store traffic, as shoppers flocked back to TGT locations for in-person shopping. And all of its segments remained strong, with all five of its core merchandise categories posting double-digit comps growth.

Zacks estimates call for Target’s FY21 revenue to climb another 14% from $93.6 billion to $106.6 billion. Meanwhile, its adjusted earnings are projected to surge 40%, which would come on top of FY20’s 47% EPS expansion.

Peeking further down the line, Target’s FY22 revenue is projected to pop another 2.3%, to help push its earnings slightly higher. Next year’s estimates clearly mark a slowdown compared to its covid-boosted results in FY20 and FY21. But the firm’s earnings and revenue outlook continued to improve throughout the last year.

Target’s consensus earnings estimates for the fourth quarter of 2021 and fiscal 2022 popped following its Q3 release and executives remains optimistic in the face of global supply chain bottlenecks and rising prices. The company’s bottom-line positivity helps TGT land a Zacks Rank #1 (Strong Buy) right now. TGT has also beaten our EPS estimates in the trailing 12 quarters.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Other Fundamentals

Target’s management team is focused on higher-than-industry-average margins. The company is able to achieve these via various efforts, including its strong supply chain and ability to fulfill more than 95% of its sales (including its booming e-commerce space) from its own stores. The rapid success of its in-house private label brand also helps keep its margins solid.

In fact, TGT said in November that it continues to expect its full-year operating income margin rate will be 8% or higher. And it raised its guidance for the vital holiday shopping quarter.

Target also flexed its fiscal stability and confidence when it raised its dividend by 32% over the summer. TGT’s current 1.60% yield tops the S&P 500’s 1.2% and its industry’s 0.83% average.

In terms of performance, Target shares have soared 225% in the last three years to crush Walmart’s 52% and Costco’s 145%. As we alluded to up top, TGT cooled off in the back half of last year, with the stock down 10% in the past six months vs. the S&P 500’s 7% pop. And Target is currently trading 15% beneath its mid-November records.

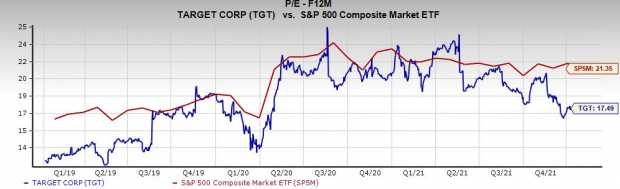

The downturn pushed Target below both its 50-day and 200-day moving averages, where it hasn’t stayed for long during the past several years. And investors with long-term horizons might want to think about stepping in considering its valuation. The stock trades at a 30% discount to its own year-long highs and its industry’s current average at 17.5X forward 12-month earnings.

Taking a step back, Target shares are trading at a discount to where they were in the fourth quarter of 2019 and right around where TGT was prior to the pandemic selloff. Target’s valuation appears even stronger considering how relatively stretched the benchmark appears.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Bottom Line

Investors should also remember that being a part of a strong industry is important when it comes to stock price movement. Target is part of the Retail - Discount Stores space that’s in the top 20% of over 250 Zacks industries.

Wall Street is also very high on Target, with 14 of the 18 brokerage recommendations Zacks has for TGT at “Strong Buys,” with the remaining four at “Holds.” And investors might want to add stocks in 2022 with strong earnings power and stable businesses amid the Fed’s plans to raise interest rates that has Wall Street dumping tech stocks to start the year.

Zacks’ Top Picks to Cash in on Artificial Intelligence

This world-changing technology is projected to generate $100s of billions by 2025. From self-driving cars to consumer data analysis, people are relying on machines more than we ever have before. Now is the time to capitalize on the 4th Industrial Revolution. Zacks’ urgent special report reveals 6 AI picks investors need to know about today.

See 6 Artificial Intelligence Stocks With Extreme Upside Potential>>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT): Free Stock Analysis Report

Walmart Inc. (WMT): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.