Fabrinet (FN) is a global manufacturing services company that specializes in precision optical, electronic, and electromechanical components. It serves industries such as telecommunications, automotive, and medical devices. Known for its expertise in high-complexity manufacturing, Fabrinet operates facilities primarily in Thailand and the U.S., offering end-to-end manufacturing and supply chain solutions.

At its most recent earnings meeting Fabrinet delivered strong financial results, exceeding market expectations in both revenue and earnings. The company achieved record revenue for the fourth consecutive quarter, totaling $753.3 million, a 15% increase year-over-year, while earnings per share (EPS) also reached a new high, coming in at $2.41. Fabrinet also announced that its Board of Directors has approved an expansion of its share repurchase program, authorizing the repurchase of up to an additional $139.5 million of Fabrinet’s ordinary shares.

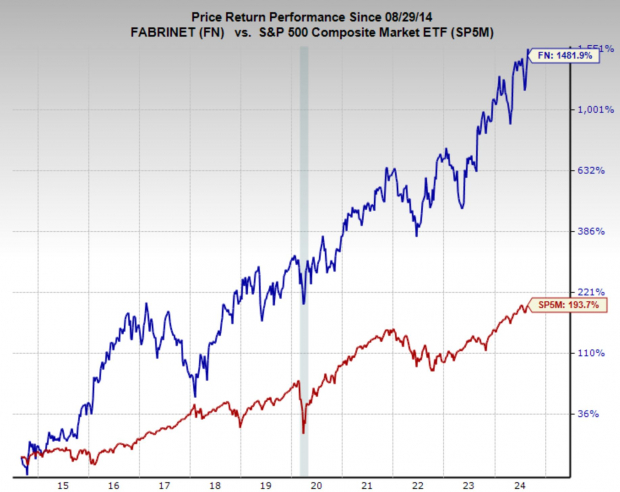

Fabrinet stock has been a powerful performer over the last decade, demonstrating its secure position in the industry and its successful business execution. Over the last ten years the stock has compounded at an annual rate of 31.7%, nearly triple that of the broad market.

Image Source: Zacks Investment Research

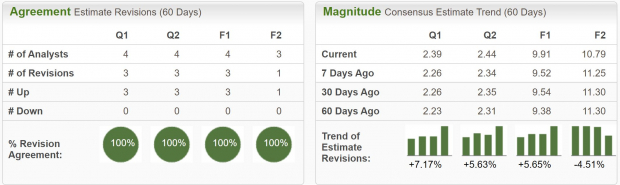

Analysts Raise Fabrinet Earnings Estimates

Possibly reflecting such a positive quarterly report, analysts have upgraded earnings estimates for Fabrinet, giving it a Zacks Rank #1 (Strong Buy) rating.

Excluding next year’s estimates, earnings have been revised higher unanimously and across timeframes. Current quarter earnings estimates have been boosted by 7.2% and are expected to grow 19.5% year-over-year (YoY), while FY25 earnings estimates have climbed by 5.7% and are forecast to grow 11.6% YoY.

Revenue is expected to grow 11.3% this year to $3.2 billion, while next year is expected to increase 9.6% to $3.5 billion.

Image Source: Zacks Investment Research

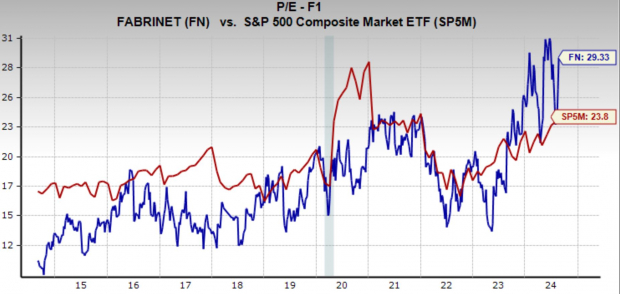

Fabrinet Shares Trade at a Historical Premium

As the quality of Fabrinet’s business has become more recognized by market participants its valuation has steadily climbed over the last 10 years. Today, FN is trading at a one year forward earnings multiple of 29.3x, which is well above its 10-year median of 16.6x and above the broad market average.

It is worth noting that as a company grows larger and demonstrates consistent profit growth such as Fabrinet has done it brings in a new class of investors who seek such a well-guarded business model. Because of this the appropriate earnings multiple can creep up as seen in FN. Nonetheless, its strong position was only further confirmed by the recent quarterly report. FN’s five-year median valuation was 20.1x, more closely reflecting this position of quality.

Image Source: Zacks Investment Research

Should Investors Buy Fabrinet Stock?

Fabrinet's strong performance, both in terms of financial results and stock appreciation, reflects the company’s solid execution and leadership in the high-tech manufacturing sector. With record revenue growth, consistent earnings beats, and an expanding share repurchase program, Fabrinet is well-positioned for continued success.

However, investors should be aware of the stock's elevated valuation. Trading at a forward earnings multiple is above its historical median—Fabrinet is priced at a premium. This premium may be justified by its consistent performance and strong industry positioning, but it also suggests that future returns may be more dependent on continued execution and growth.

For long-term investors looking for exposure to a high-quality company with a proven track record in precision manufacturing and growth potential in key sectors like telecommunications, automotive, and medical devices, Fabrinet could still be a strong buy. However, new investors should consider the current valuation and potentially look for pullbacks to optimize entry points.

Overall, Fabrinet represents a compelling investment opportunity, particularly for those focused on long-term growth in the technology and manufacturing sectors.

Zacks Names #1 Semiconductor Stock

It's only 1/9,000th the size of NVIDIA which skyrocketed more than +800% since we recommended it. NVIDIA is still strong, but our new top chip stock has much more room to boom.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>Fabrinet (FN) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.