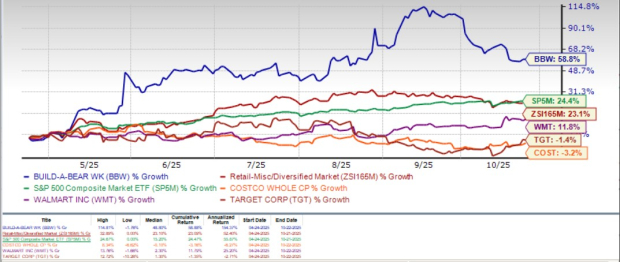

Build-A-Bear Workshop, Inc. BBW has witnessed a remarkable 58.8% surge in its stock price over the past six months, far outpacing broader benchmarks. The rally reflects solid execution across its retail, digital and commercial channels, supported by consistent earnings growth and disciplined capital allocation. With strong cash generation and a debt-free balance sheet, Build-A-Bear has evolved into a resilient consumer brand.

After such a sharp rally, investors are contemplating whether BBW’s fundamentals still justify holding the stock, investing more or booking some profits. Closing yesterday’s trading session at $56.10, Build-A-Bear has outpaced the industry, which has risen 23.1%, and the broader S&P 500 index, which has advanced 24.4% in the same period.

Build-A-Bear has even outperformed prominent players, such as Walmart Inc. WMT, Costco Wholesale Corporation COST and Target Corporation TGT. While shares of Walmart have risen 11.8% in the past six months, Costco and Target have declined 3.2% and 1.4%, respectively.

BBW Stock Six-Month Performance

Image Source: Zacks Investment Research

Tailwinds Behind BBW’s Momentum

Build-A-Bear is evolving from a niche mall-based retailer into a high-margin, diversified lifestyle brand. Its latest quarterly results make a compelling case for investors seeking both growth and profitability. For the second quarter of fiscal 2025, total revenues climbed 11.1% year over year to $124.2 million, while pre-tax income surged 32.7% to $15.3 million and earnings jumped 46.9% to 94 cents a share. This performance reflects that BBW has not only sustained post-pandemic momentum but also successfully expanded margins through pricing discipline, product innovation and capital efficiency.

One of Build-A-Bear’s most powerful growth engines is its asset-light partner-operated model, which enables rapid, low-capital store expansion worldwide. Management raised its fiscal 2025 net new unit guidance to at least 60 locations, up from the previous target of at least 50, largely driven by the accelerating pace of partner-operated openings. In the second quarter, BBW added a net 14 locations, including nine partner-operated locations, ending the period with 627 locations globally. This strategy has pushed partner-operated stores to roughly 25% of the company’s total footprint.

The company’s diversification efforts are also paying off, with strong growth in both its commercial and e-commerce channels. In the last reported quarter, commercial and international franchise revenues increased 15.2% year over year to $9.6 million, while consolidated e-commerce demand jumped 15.1%. These segments are helping Build-A-Bear reduce its reliance on mall-based traffic while tapping into broader consumer demographics. The company’s focus on web-driven demand and licensing not only smooths seasonality but also boosts margins. Complementing this expansion is the company’s product innovation strategy, led by the success of its Mini Beans collection.

Build-A-Bear's balance sheet strength provides it with enough headroom to continue aggressive buybacks. BBW ended the second quarter with $39.1 million in cash, cash equivalents and restricted cash. This was up 55.4% compared to the prior-year period while maintaining a debt-free position and unused revolving credit facility. During the first half of 2025, $13.1 million was returned to shareholders through dividends ($5.8 million) and stock repurchases ($7.3 million), supported by strong operating cash flow and margin expansion.

With consistent profitability, rising cash generation and a flexible growth model, Build-A-Bear Workshop appears well-positioned to sustain its momentum through fiscal 2025 and beyond. Management’s execution of its multi-channel strategy — blending in-store experiences, digital engagement and strategic partnerships — is reshaping the company’s long-term growth profile. As consumer demand for experiential and collectible products remains solid, Build-A-Bear is well-positioned to drive growth.

Is Build-A-Bear Stock Undervalued or Overvalued?

From a valuation standpoint, Build-A-Bear's forward 12-month price-to-earnings ratio stands at 12.96, lower than the industry’s ratio of 17.84. Build-A-Bear is trading at a discount to Walmart (with a forward 12-month P/E ratio of 37.75) and Costco (46.68) but at a premium to Target (11.88).

Image Source: Zacks Investment Research

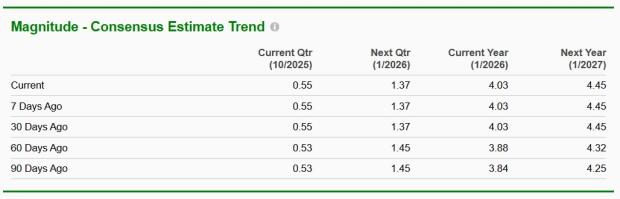

Here’s How Estimates Have Shaped Up for BBW

Wall Street analysts have expressed confidence in Build-A-Bear by raising their earnings estimates. Over the past 60 days, the Zacks Consensus Estimate for the current and next fiscal years has risen 3.9% to $4.03 and 3% to $4.45 per share, respectively.

Image Source: Zacks Investment Research

How to Play BBW Stock: Buy, Hold or Sell?

Build-A-Bear’s strong brand evolution, expanding partner model and consistent execution make it a compelling long-term story rather than a short-term trading play. The company’s balance sheet strength and diversified growth engines provide a solid cushion against market volatility, suggesting the rally is grounded in fundamentals. For existing investors, staying invested appears reasonable as momentum and earnings visibility remain favorable. Meanwhile, potential investors could consider accumulating the stock on pullbacks, given its solid fundamentals and attractive growth trajectory. BBW stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Target Corporation (TGT) : Free Stock Analysis Report

Walmart Inc. (WMT) : Free Stock Analysis Report

Costco Wholesale Corporation (COST) : Free Stock Analysis Report

Build-A-Bear Workshop, Inc. (BBW) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.