BILL Holdings BILL continues to gain momentum as transaction fee revenues increased 17% year over year to $252.1 million in the third quarter of fiscal 2025. This growth was largely driven by an 11% increase in Total Payment Volume (TPV), which reached $79.4 billion, reflecting rising payment volume and the company’s transaction-based income.

Growing adoption of BILL’s integrated financial operations platform, which served more than 488,600 businesses at the end of the fiscal third quarter, is positively impacting top-line growth. The platform processed 30 million transactions during the reported quarter, up 16% year over year. Enhanced offerings, such as Instant Payments, Local Transfer and Supplier Payments Plus, are expanding high-fee payment options and attracting larger enterprises to the network, contributing to stronger monetization and broader platform engagement.

While TPV showed solid year-over-year growth, BILL acknowledged some headwinds during the quarter. Customer spending came in slightly below expectations, resulting in a slight sequential decline in TPV and transactions per customer. However, this impact was partially mitigated by a favorable payment mix, as a greater share of high-margin transactions helped support monetization.

BILL’s long-term outlook remains constructive, driven by its continued investments in AI, ERP integrations and payment innovations, which are deepening user engagement and positioning the company for sustainable, volume-driven growth.

BILL Faces Competition From Large Fintech Players

BILL operates in a growing, competitive fintech landscape, increasingly challenged by larger, more diversified players with deeper market reach.

Global Payments GPN offers a robust global merchant processing and software ecosystem, handling over 50 billion transactions annually. GPN excels in high-volume credit-debit payments and issuer solutions, largely through its TSYS and Worldpay platforms. GPN’s strategic acquisitions, strong cash flows and expansive global footprint position it for sustained long-term growth.

Meanwhile, Intuit INTU, with flagship products like QuickBooks and TurboTax, continues to expand into AP/AR automation. Intuit’s tightly integrated small business ecosystem, brand strength and ongoing investments in AI and user experience give it a compelling edge. Both GPN and INTU present formidable competition to BILL’s niche focus on SMB financial workflows.

BILL’s Share Price Performance, Valuation & Estimates

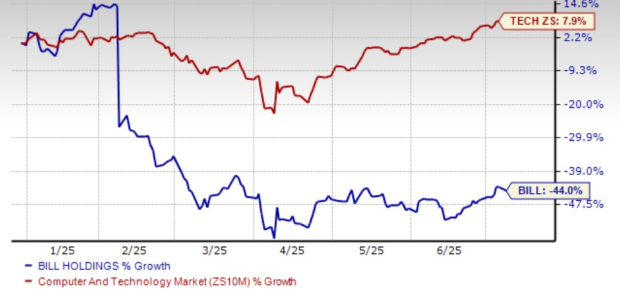

BILL’s shares have dropped 44% year to date, underperforming the broader Zacks Computer and Technology sector’s return of 7.9%.

BILL YTD Price Return Performance

Image Source: Zacks Investment Research

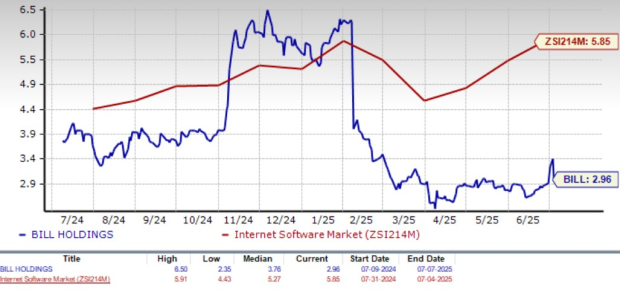

From a valuation standpoint, its forward 12-month Price/Sales of 2.96X compares with the industry’s 5.85X. BILL has a Value Score of D.

BILL Forward 12-Month Price/Sales Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for fiscal 2025 earnings is pegged at $2.07 per share, reflecting a 6.7% increase over the past 60 days. The earnings estimate reflects a 2.36% year-over-year decline.

Image Source: Zacks Investment Research

BILL currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Intuit Inc. (INTU) : Free Stock Analysis Report

Global Payments Inc. (GPN) : Free Stock Analysis Report

BILL Holdings, Inc. (BILL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.