Key Points

Quantum computing stocks D-Wave and Rigetti have seen double-digit drops year to date.

Both D-Wave and Rigetti are not profitable but have amassed large cash hoards on their balance sheets.

D-Wave is growing bookings, while Rigetti captured a big customer order in 2026.

- 10 stocks we like better than D-Wave Quantum ›

Quantum computing has the potential to transform technologies such as artificial intelligence (AI). It can process complex data in minutes that would take centuries for a conventional computer.

The sector sparked strong investor interest in 2025, but the "great rotation" of 2026 changed the situation. Wall Street shifted away from tech stocks with sky-high valuations this year, which includes the nascent quantum computing industry.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

This creates a potential buy opportunity for once-hot stocks D-Wave Quantum (NYSE: QBTS) and Rigetti Computing (NASDAQ: RGTI). The former's share price is down 47% this year through the week ending March 27. Rigetti dropped 40% in that time.

But if you had to pick only one, which is a better investment in the quantum computer field? Here's an examination of both to arrive at an answer.

Image source: Getty Images.

Rigetti Computing

Rigetti uses gate-model technology for its quantum computers, a popular approach in the sector since it allows for precise control over quantum machines. The company seeks to solve some key industry challenges, such as enabling scalable systems.

Rigetti's competitive advantage is a vertically integrated tech stack, enabling end-to-end execution of the construction process. Its in-house Fab-1 manufacturing process permits quick iterations in the design and building of quantum computer chips.

The company's vertical integration strategy seems sound, yet it hasn't led to much revenue. It ended 2025 with $7.1 million in sales, a 34% decline from the prior year's $10.8 million. This resulted in a 2025 operating loss of $84.7 million as research expenses soared 23% year over year to $61.3 million.

With slim sales compared to huge costs, the company is in a precarious position. Its saving grace is its substantial cash and short-term investments totaling $443.5 million at the end of 2025. This provides a cushion while it builds up sales.

In that regard, the company recently announced purchase orders from India and Japan. The former is worth $8.4 million, which is more than Rigetti's $7.1 million in total 2025 revenue.

D-Wave's strong 2026 start

D-Wave is off to an excellent start in 2026. It closed the acquisition of Quantum Circuits in January, which is significant because Quantum Circuits specializes in the gate-model approach, while D-Wave focuses on annealing quantum computers.

Annealing quantum technology is great for solving optimization problems, such as those often found in logistics and machine learning, but isn't ideal for general computational needs, limiting its usefulness. Therefore, the Quantum Circuits acquisition fills a gap in D-Wave's offerings.

The company also announced customer bookings of more than $30 million in January. This sum represents impressive acceleration from fourth-quarter bookings of $13.4 million and the mere $2.4 million achieved in the third quarter.

Moreover, D-Wave enjoyed 179% year-over-year sales growth to $24.6 million in 2025. Its January bookings suggest 2026 revenue could rise even higher.

However, like Rigetti, D-Wave is not profitable. In 2025, its operating loss was $100.4 million, up 30% year over year. That said, at the end of 2025, it held record cash and marketable securities of $884.5 million on its balance sheet.

Deciding between D-Wave and Rigetti

When choosing to invest in D-Wave or Rigetti for exposure to the quantum computing sector, the former looks like the superior investment. Several factors stand out to make D-Wave the better buy.

Its revenue is larger and growing compared to Rigetti's, suggesting its approach is gaining greater traction in the market. It has a higher cash balance to sustain its business as it builds sales, and its 2026 bookings demonstrate it's making progress in securing more customers.

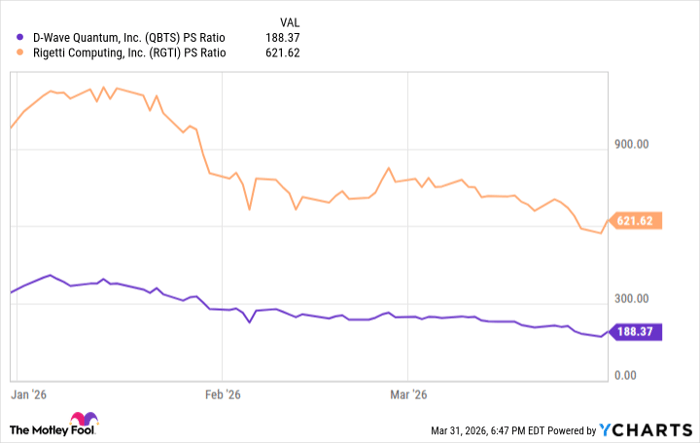

In addition, D-Wave stock has a superior valuation compared to Rigetti, as illustrated by the price-to-sales ratio (P/S), which indicates how much investors are paying for each dollar of revenue generated over the past 12 months.

Data by YCharts.

The chart shows that D-Wave and Rigetti experienced a drop in their sales multiples this year, but D-Wave is significantly lower than its rival, indicating it is the cheaper stock.

The company's several advantages over Rigetti make it the better pick, yet because quantum computing is an emerging technology, and identifying the long-term winners is far from certain, investing in the sector requires a high risk tolerance.

Should you buy stock in D-Wave Quantum right now?

Before you buy stock in D-Wave Quantum, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and D-Wave Quantum wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $515,294!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,077,442!*

Now, it’s worth noting Stock Advisor’s total average return is 914% — a market-crushing outperformance compared to 184% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of April 3, 2026.

Robert Izquierdo has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.