On the surface, Mastercard (NYSE: MA) and Visa (NYSE: V), look similar enough as companies. Indeed, they appear almost interchangeable. They're both just credit card middlemen, collecting a small percentage of the transaction every time a customer makes a card-based purchase.

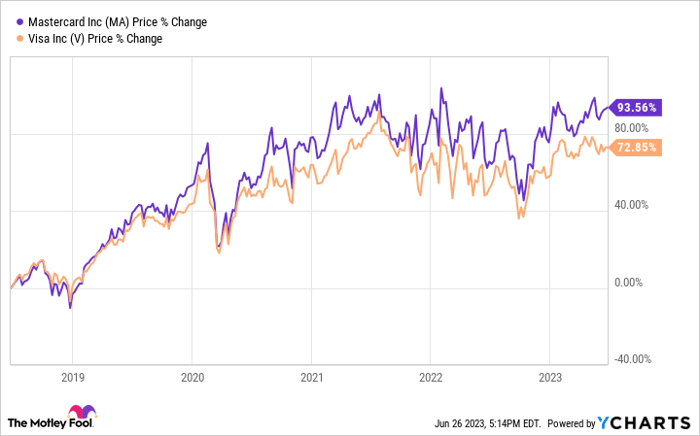

If you look more closely at their performances ... well, not a whole lot seems to change either. The two companies -- as well as their respective stocks -- also sport comparable results for the past several years. That makes sense, too. They're in the same business serving the same markets, after all.

There's one distinct difference between these two companies, however, that makes a difference to investors. And this nuanced difference favors a position in Mastercard over Visa.

Mastercard enjoys a subtle but meaningful edge

Don't panic if you already own a stake in Visa and aren't in a position to swap it out for the other name. Visa's a fine company in its own right.

For future-thinking investors, though, Mastercard's arguably got more growth potential.

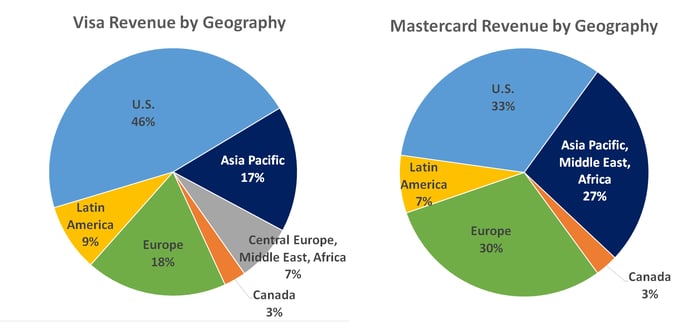

The key is where the two companies derive their respective revenue. The United States is both organizations' single biggest market, and Europe is second for both. Visa relies far more heavily on the U.S. for revenue than Mastercard does, however, whereas Mastercard's reach is stronger in Europe and the Asia Pacific region.

Data source: Visa and Mastercard. Chart by author.

And, yes, it matters.

Most of us are a little too busy with our lives to dig into such details or to think philosophically about these things. But the U.S.'s (and Canada's) credit and debit card market is pretty well saturated. The Atlanta branch of the U.S. Federal Reserve Bank reports that 77% of all adults living in the U.S. own a credit card, while 93% hold a debit card. Most American and U.S. residents, in fact, have several cards.

These people are using their cards too. On average, people in the U.S. are using about one-fourth of their total credit capacity, carrying a typical balance of more than $5,000. The U.S. doesn't really need more domestic lines of credit. Many of these people, in fact, are looking for ways to wean themselves off the spending all these easy-to-get credit accounts seem to induce.

In other words, the United States isn't exactly a high-growth market for credit card middlemen.

That's not quite the case elsewhere, where Mastercard enjoys a measurably better market share. Take Europe's highly developed U.K. and German markets as an example. Only 62% of people in the United Kingdom currently own a credit card, according to data from The World Bank, while in Germany the figure's less than 57%.

Connect the dots. There's room for growth.

Ditto along the Pacific Rim, which includes Australia, where only a little more than half of residents have a credit card. The number's less than 40% in China, where Mastercard is making a point of developing its cross-border payment offerings.

We're seeing this opportunity start to bear out in results. While Mastercard's gross purchase volume in the United States grew 12.2% last year, it improved to the tune of 18.6% all over the rest of the world. Visa saw similar disparity in its volume growth in the U.S. and abroad. But it saw less overall growth (perhaps reflecting its sheer bigger size), and its above-average growth abroad means less to it than it does to Mastercard.

Not forever, but for now and until further notice

This edge may not always exist. Visa may figure out how to better compete overseas. Mastercard may make a major mistake, like buying the wrong company. After all, it is aggressively acquiring bolt-on names, like the recent deal for cybersecurity outfit Baffin Bay. Not all these deals are going to end up adding value. Anything's possible.

This nuanced dynamic is one that will likely persist for several years, providing Mastercard a slight but decided edge on its bigger rival as long as it does. And when two companies are as similar as these two are, it's the little things that end up making big differences to investors.

10 stocks we like better than Mastercard

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Mastercard wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of June 26, 2023

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Mastercard and Visa. The Motley Fool recommends the following options: long January 2025 $370 calls on Mastercard and short January 2025 $380 calls on Mastercard. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.