General Electric (NYSE: GE) or Raytheon Technologies (NYSE: RTX) for 2023? The two industrial giants are fierce rivals in commercial aerospace (they are the two leading players in aircraft engines), and a comparison of their relative investment merits says a lot about the current overall investing environment. So which stock is the better option for investors right now?

Commercial aerospace

A lazy, superficial interpretation of affairs would quickly conclude that Raytheon Technologies is more of a commercial aerospace company versus the more broad-based, industrially focused General Electric. That view might lead investors to favor Raytheon because commercial flight departures are still recovering to at least 2019 levels. Meanwhile, the economic slowdown will pressure other areas of the industrial economy currently operating closer to full capacity.

However, that view would be wrong. In reality, commercial aerospace is more important to GE. While GE does have a healthcare segment, it will be spun off in early January 2023. Looking into the implied guidance for 2023, GE's management believes GE Aerospace (predominantly a commercial aerospace business) will generate $6 billion in profit in 2023, compared to $1 billion to $2 billion for GE Power, while the remaining business, GE Renewable Energy will struggle to avoid a loss in 2023.

In contrast, based on my calculation interpolated from management's estimates, Raytheon Technologies is set to generate around 54% of its segment profit from its two commercial-aerospace-focused businesses, Pratt & Whitney and Collins Aerospace, in 2022. GE's greater overall exposure to commercial aerospace is one reason to give it the edge over Raytheon in 2023.

Commercial aerospace is a growth market

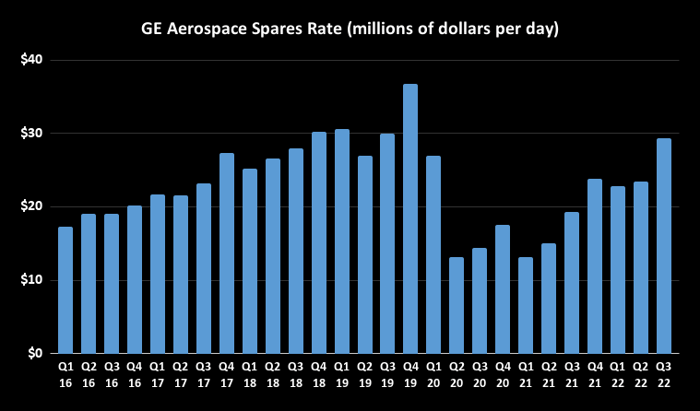

CFM International -- GE Aerospace's joint venture with Safran -- and Pratt & Whitney are the leading players in aircraft engines, with rival engines on the Airbus A320 neo family -- CFM's LEAP engine is also the sole engine on the Boeing 737 MAX. A good way to monitor commercial aviation conditions is through GE Aerospace's spares rate, representing the spare parts used in time and material shop visits in millions of dollars per day.

As you can see in the chart, the commercial aviation industry continues to grow strongly. Management expects GE Aerospace's revenue to grow more than 20% in 2022, while Raytheon's management expects low-double-digit sales growth at Collins Aerospace (original equipment and aftermarket aerospace structures and systems) and low teens at Pratt & Whitney in 2022.

Data source: General Electric presentations.

The nonaerospace businesses

Raytheon definitely has the edge regarding the quality of the two companies' nonaerospace-focused businesses. Indeed, its defense businesses (Raytheon Intelligence & Space, or RIS; and Raytheon Missiles & Defense, or RMD) are seeing robust demand, partly due to a new geopolitical reality and tensions created out of the conflict in Ukraine.

That said, it is still battling to overcome supply chain difficulties and component shortages that negatively impacted profitability in 2022.

However, challenges can often become opportunities. For example, if the supply chain pressures ease in 2023 (likely as the economy slows, releasing tension on supply chains), RIS & RMD could get some help on margins.

But here's the thing: GE Aerospace and GE Renewable Energy also got hit hard with supply chain costs and logistical difficulties in 2022. If conditions ease (say, transportation costs, raw material prices, and semiconductor availability) for Raytheon, they are likely to ease for GE too. As such, buying both stocks involves making the same positive assumption over an easing supply chain environment in 2023.

Valuation favors General Electric

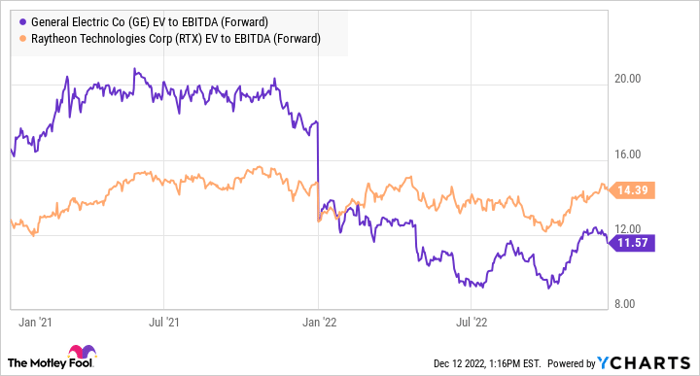

Finally, a quick look at valuations in terms of enterprise value (market cap plus net debt) to earnings before interest, taxation, depreciation, and amortization (EBITDA) suggests GE is better valued.

Data by YCharts

All told, Raytheon is an attractive company on its own and a stock worth buying for 2023 in its own right. However, GE gets the nod if forced to choose between the two. Its greater exposure to commercial aviation, lower valuation, and upside to an easing supply chain environment (also shared with Raytheon) mean it's slightly more attractive than its rival.

10 stocks we like better than General Electric

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and General Electric wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of December 1, 2022

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.