Robinhood (NASDAQ: HOOD) and Coinbase (NASDAQ: COIN) were both once considered disruptive fintech companies. Robinhood challenged traditional brokerages with commission-free trades for stocks, exchange-traded funds (ETFs), options, and cryptocurrencies. Coinbase emerged as one of the world's largest cryptocurrency exchanges.

But today, Robinhood trades more than 70% below its IPO price of $38 per share from last August. Coinbase, which started trading at $381 per share after its direct listing last April, now trades more than 80% below that price.

Let's see why these two fintech darlings were crushed, and if investors should consider either out-of-favor stock to be a turnaround play.

Image source: Getty Images.

A trio of unusual tailwinds

Robinhood and Coinbase benefited from three unusual tailwinds in 2020 and 2021. First, the COVID-19 pandemic caused people to stay at home and actively trade more stocks, options, and cryptocurrencies. Second, many of those investors used their federal stimulus checks to invest on those trading platforms.

Lastly, many retail investors plowed their cash into high-flying stocks and cryptocurrencies instead of more conservative investments. The Reddit-fueled rally in "meme stocks," the surging prices of cryptocurrencies, and bullish comments from famous growth investors like Cathie Wood also triggered a FOMO ("fear of missing out") rally that lasted until late 2021.

As a result, Robinhood and Coinbase both experienced explosive growth in 2021. Robinhood's revenue surged 89% to $1.82 billion as its monthly active users (MAUs) jumped 48% to 17.3 million. Coinbase's revenue soared 545% to $7.36 billion as its monthly transacting users (MTUs) increased 307% to 11.4 million.

The speculative bubble pops

But over the past six months, inflation and rising interest rates popped that speculative bubble. Those macroeconomic headwinds caused investors to dump riskier assets, like meme stocks and cryptocurrencies, and buy more conservative investments. Inflationary headwinds also forced retail investors to conserve their cash instead of plowing it into the markets, and a lack of new stimulus checks exacerbated that slowdown.

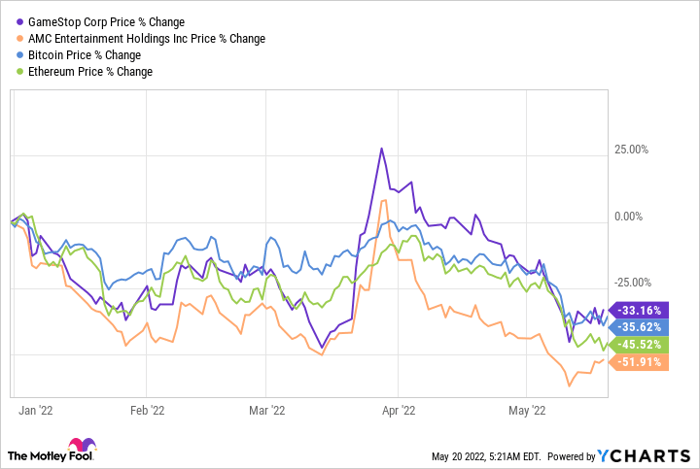

If we look at the prices of GameStop (NYSE: GME), AMC (NYSE: AMC), Bitcoin (CRYPTO: BTC), and Ethereum (CRYPTO: ETH) this year, we'll see why investors broadly lost their appetite for meme stocks and cryptocurrencies.

Source: YCharts

That's why Robinhood and Coinbase both face grueling slowdowns this year. In the first quarter of 2022, Robinhood's MAUs tumbled 10% year over year and 8% sequentially to 15.9 million. its average revenue per user (ARPU) fell 61% year over year to $53.

For the full year, analysts expect Robinhood's revenue to decline 16% to $1.52 billion as its adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) flips from $34 million to a loss of $328 million. It's also expected to remain unprofitable on a generally accepted accounting principles (GAAP) basis, with a net loss of $1.3 billion.

Coinbase's MTUs rose 51% year over year to 9.2 million in the first quarter, but still declined 19% sequentially from Q4 2021. It expects to end the year with 5 million to 15 million MTUs, depending on the market's appetite for cryptocurrencies, but that broad range runs from a 56% year-over-year decline to 32% year-over-year growth.

Coinbase's own expectations are vague, but analysts' consensus expectation is for its revenue to decline 41% to $4.7 billion this year as its adjusted EBITDA reverses from $4.1 billion to a loss of $151 million. They also expect it to post a GAAP loss of $1.7 billion.

Coinbase management's outlook is even gloomier: The company expects to rack up an adjusted EBITDA loss of "approximately $500 million" for the year as it endures a "prolonged and stressful scenario."

The valuations and verdict

Robinhood and Coinbase look unappealing in this tough market for tech stocks, and both companies could still face significant regulatory headwinds in the future as the Securities and Exchange Commission closely scrutinizes Robinhood's payment for order flow (PFOF) model and imposes new regulations on the cryptocurrency market.

That said, Robinhood and Coinbase still look fundamentally cheap at about 6 and 4 times this year's sales estimates, respectively. Those depressed price-to-sales ratios could make them tempting takeover targets for banks, brokerages, or diversified fintech companies.

I personally wouldn't bet on either stock as a turnaround play right now. But if I had to choose one over the other, I'd buy Robinhood because it's more broadly diversified and isn't an all-in bet on cryptocurrencies. If I wanted more exposure to cryptocurrencies, I'd simply buy Bitcoin or Ethereum instead of investing in Coinbase's capital-intensive business.

10 stocks we like better than Robinhood Markets, Inc.

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Robinhood Markets, Inc. wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of April 27, 2022

Leo Sun has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bitcoin, Coinbase Global, Inc., and Ethereum. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.