Investors have cooled on the industrial niche of the real estate investment trust (REIT) sector. There's no better example of that than the roughly 25% decline from 2022 highs in the price of industrial giant Prologis (NYSE: PLD). That REIT is, without a doubt, a leader in the industrial REIT sector, but investors might still find more diversified W.P. Carey (NYSE: WPC) of more interest. Here's why.

Dividends

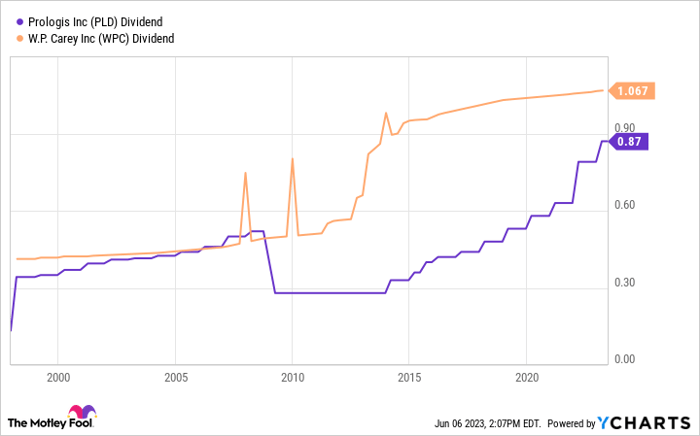

If you are looking at REITs, you are probably interested in dividends. W.P. Carey's dividend yield is 6.1% today, while Prologis' yield is less than half that at 2.8%. From a yield perspective, W.P. Carey easily beats Prologis. But there's more to the dividend story than yield alone.

Image source: Getty Images.

W.P. Carey has increased its dividend annually since its initial public offering in 1998. That's more than a quarter of a century of increases, including right through the Great Recession and the coronavirus pandemic, among other tough market and economic periods. That streak also includes the company's transition from a partnership structure to a REIT, which would have been an easy time to reset the dividend lower if management had wanted. It didn't, and has clearly shown that returning value to investors with regular dividend increases is a key priority.

PLD Dividend data by YCharts.

By comparison, Prologis ended up cutting its dividend in the Great Recession and its dividend increase streak is "only" 10 years long. That's nothing to sneer at and the industrial-focused REIT's dividend has grown at a far more rapid clip than that of W.P. Carey over the past decade. But for consistency, W.P. Carey clearly gets the nod.

That said, Prologis' funds from operations (FFO) payout ratio in the first quarter was 71%. W.P. Cary's FFO payout ratio was 83%, which is not as strong. There's a nuance here, though, because Prologis operates its properties while W.P. Carey uses the net lease approach.

Different ways of doing things

Prologis has a massive portfolio of warehouse properties (totaling 1.2 billion square feet across 19 countries!) that it actively manages, including offering services for which it earns additional revenue. It is the 800-pound gorilla of the warehouse sector. But it actually manages its properties, which leads to additional costs and makes a lower FFO payout ratio a prudent decision as cash might be needed for other things (like property upgrades and repairs).

W.P. Carey uses a net lease approach, which means that it leases its properties to single tenants that are responsible for most asset-level operating costs. Since it doesn't have to think about those expenses, it can afford to have a higher FFO payout ratio. But that's not the only difference.

While Prologis is laser-focused on one property niche, W.P. Carey has gone in the exact opposite direction. Its portfolio of roughly 1,445 properties (about 176 million square feet) is spread across the industrial (27% of rents), warehouse (24%%), retail (17%), office (17%), and self-storage (5%) sectors (a fairly large "other" category rounds things out to 100%). And while it doesn't have quite the same global reach as Prologis, W.P. Carey has a sizable portfolio of assets in Europe (36% of rents). It is one of the most diversified REITs you can buy, making it almost a one-stop shop for investors seeking REIT exposure.

And that's really where the rubber hits the road. Where Prologis is a one-trick pony with a modest yield, W.P. Carey gives you broader exposure, a much more generous yield, and a stronger dividend history.

One and done

If you are looking specifically for an out-of-favor industrial REIT, then Prologis has to be on your list of names to consider. But if what you really want is just a dividend-paying REIT, then you have a lot more options. And one of the most attractive, given its diversification and dividend history, is W.P. Carey. And like Prologis, W.P. Carey's shares have been in a downtrend, so the generous 6.1% yield is up toward its highest levels over the past decade. In other words, like Prologis, W.P. Carey seems like it is on sale, too, but in some important ways, it offers investors more than Prologis.

10 stocks we like better than Prologis

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Prologis wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of June 5, 2023

Reuben Gregg Brewer has positions in W. P. Carey. The Motley Fool has positions in and recommends Prologis. The Motley Fool recommends W. P. Carey. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.