Humana HUM is a health care plan provider in the United States. The company provides health insurance benefits under Health Maintenance Organization, Private Fee-For-Service, and Preferred Provider Organization plans.

Analysts have taken a bearish stance on the company’s earnings outlook, landing it into a Zacks Rank #5 (Strong Sell).

Image Source: Zacks Investment Research

In addition, the company currently resides in the Zacks Medical – HMOs industry, which is currently ranked in the bottom 14% of all Zacks industries. Let’s take a closer look at a few other aspects of the company.

Humana

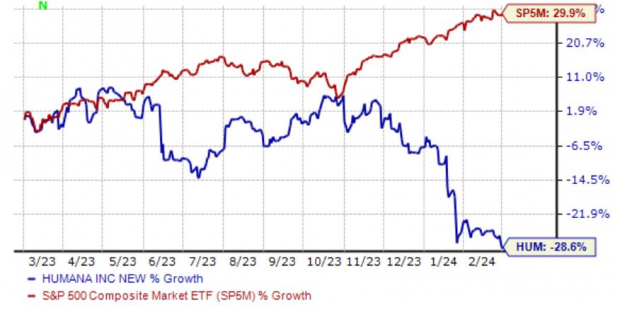

HUM shares have struggled to find their footing over the last year, losing nearly -29% in value and widely underperforming relative to the S&P 500. Shares faced notably strong selling pressure following its latest quarterly release, with the company falling short of the Zacks Consensus EPS estimate by 57%.

Image Source: Zacks Investment Research

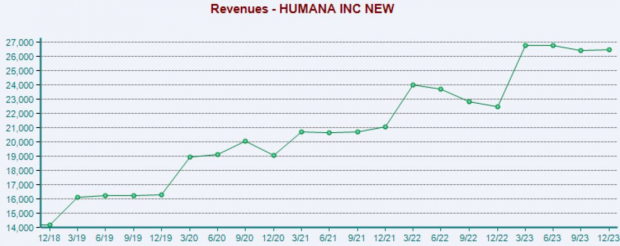

The results were hampered by an additional increase in Medicare Advantage medical cost trends, causing the company to give ‘soft’ initial guidance for its FY24. The results snapped a streak of positive EPS surprises, with investors reacting negatively in response.

Image Source: Zacks Investment Research

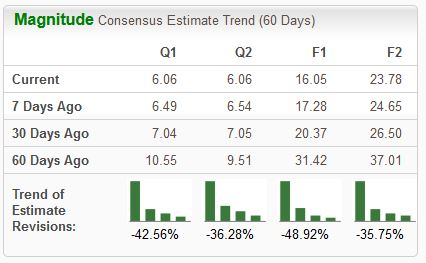

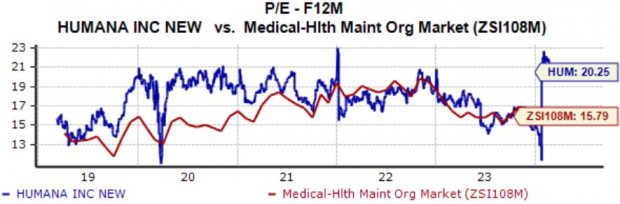

The company’s profitability is forecasted to take a sizable hit in its current year (FY24), with the $16.05 Zacks Consensus EPS estimate representing a pullback of -38% from FY23. Shares presently trade at a 20.3X forward 12-month earnings multiple, above the five-year median and the respective Zacks industry average.

The stock carries a Style Score of ‘D’ for Value.

Image Source: Zacks Investment Research

Bottom Line

Negative earnings estimate revisions from analysts stemming from increased costs paint a challenging picture for the company’s shares in the near term.

Humana HUM is a Zacks Rank #5 (Strong Sell), indicating that analysts have taken a bearish stance on the company’s earnings outlook.

For those seeking strong stocks, a great idea would be to focus on stocks carrying a Zacks Rank #1 (Strong Buy) or a Zacks Rank #2 (Buy) – these stocks sport a notably stronger earnings outlook paired with the potential to deliver explosive gains in the near term.

Zacks Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>Humana Inc. (HUM) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.