Falling 30% year to date, the trend of declining earnings estimate revisions points to more downside risk for IGP Photonics IPGP stock.

After much hype in recent years, investor sentiment has diminished for the laser systems and components provider due to shrinking operating margins amid lower demand for materials processing products.

To that point, IPGP has fallen mightily from its all-time peaks of over $200 a share, and unfortunately, the slide could continue as IPG's stock lands a Zacks Rank #5 (Strong Sell) and the Bear of the Day.

Image Source: Zacks Investment Research

IPG’s Q1 Results & Guidance Spooked Investors

Although IPG was able to exceed its Q1 expectations in early May, sales fell 9% from the comparative quarter to $227.79 million. More concerning, earnings dropped 40% to $0.31 a share from EPS of $0.52 in Q1 2024. Attributing to the top and bottom-line decline were tariff-related costs, which have reduced demand for material product applications that rely heavily on IPG’s high-performance lasers.

Furthermore, IPG warned that tariff-related delays could slow shipments and further impact its profit margins. Leading to much anguish, IPG expects Q2 EPS between $0.05-$0.25 versus $0.45 a share in the prior period, with sales expected at $210-$240 million compared to $257 million a year ago.

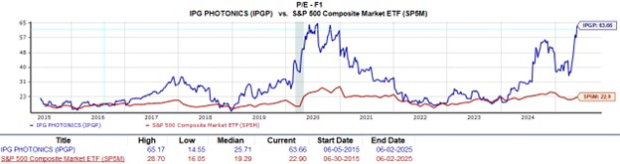

Declining EPS Revisions & Stretched P/E Valuation

Correlating with softer-than-expected guidance, earnings estimate revisions have continued to decline for IPG. Notably, fiscal 2025 and FY26 EPS estimates have now dropped over 37% in the last 60 days, respectively.

Image Source: Zacks Investment Research

Making the trend of declining EPS revisions harder to bear is that IPG’s stock still trades at an overly stretched premium to the broader market at 63.6X forward earnings. It’s also noteworthy that IPGP is trading near its decade-long high in terms of price to forward earnings and is 177% above its median of 25.7X during this period.

Image Source: Zacks Investment Research

Bottom Line

There are many signs that point to it being time to sell IPG Photonics stock, with IPGP having an overall “F” VGM Zacks Style Scores grade for the combination of Value, Growth, and Momentum. Ultimately, investing in the company’s unique laser services is not worth it right now.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2024. While not all picks can be winners, previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>IPG Photonics Corporation (IPGP) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.