Dine Brands Global, Inc. DIN stock has tanked 60% in the past three years, while its Zacks sector climbed 65% and its Retail–Restaurants industry climbed 12%.

The restaurant giant behind Applebee's and other chains has a rough balance sheet, and its earnings revisions have tumbled over the past several years as Dine Brands struggles to navigate multiple headwinds.

Should Investors Stay Away from DIN Stock?

Dine Brands operates restaurants via subsidiaries and franchisees under the Applebee's Neighborhood Grill + Bar, IHOP, and Fuzzy’s Taco Shop brands. The Pasadena, California-headquartered company boasted that its portfolio consisted of roughly 3,500 restaurants across 19 international markets as of June 30.

DIN has struggled since its massive post-Covid lockdown boom that benefited every area of the consumer economy. Since then, soaring inflation and slowing consumer spending have hurt revenue and crushed its bottom line.

On top of that, consumers have more dining options than ever, and more people are trying to eat healthier.

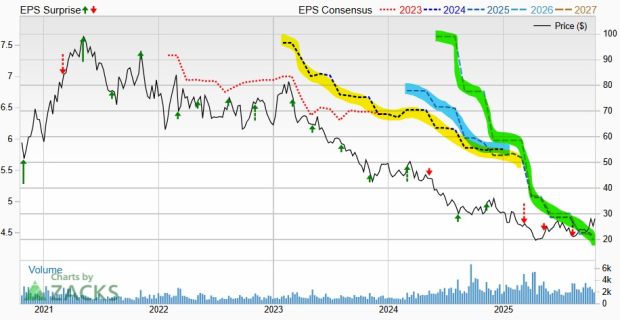

Image Source: Zacks Investment Research

The chart above shows that DIN’s earnings estimates fell off a cliff over the past several years. Dine Brands missed our Q2 earnings estimate by 22% and provided downbeat earnings per share (EPS) guidance.

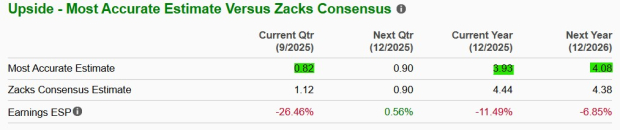

DIN's Most Accurate estimates came in well below consensus for Q3, FY25, and FY26 (see below). Dine Brands' overall negative EPS revisions earn the stock a Zacks Rank #5 (Strong Sell).

Image Source: Zacks Investment Research

Some investors might want to start bottom-feeding on Dine Brands stock since it’s trading near its Covid lows while the broader stock market sits near fresh records.

But it might be wise to stay away from DIN since it has underperformed its industry by a wide margin over the past 10 years (down -68% vs. its industry’s +75% climb).

The Retail–Restaurants space is in the bottom 15% of roughly 240 Zacks industries. This amplifies its near-term bear case since studies have shown that roughly half of a stock's price movement can be attributed to its industry group. And the top 50% of Zacks Ranked Industries outperforms the bottom 50% by a factor of more than 2 to 1.

On top of that, Dine Brands has more liabilities (total and current) than assets (total and current).

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>DINE BRANDS GLOBAL, INC. (DIN) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.