BDSwiss Insights: Don’t Worry About the Dollar’s Global Role

Marshall Gittler is the Head of Investment Research at online brokerage firm BDSwiss Group

Image originally posted on Tsikot

Recently the financial press and my Twitter feed have been filled with stories about what the recent weakness of the dollar means. The gist of many of these articles seems to be how the world is losing confidence in the US currency thanks to the Fed’s extraordinary money-printing and how the dollar’s place as the center of the global monetary system is at risk. A typical headline: the Financial Times’s Big Read recently was Dollar blues: why the pandemic is testing confidence in the US currency

All I can say is: don’t hold your breath.

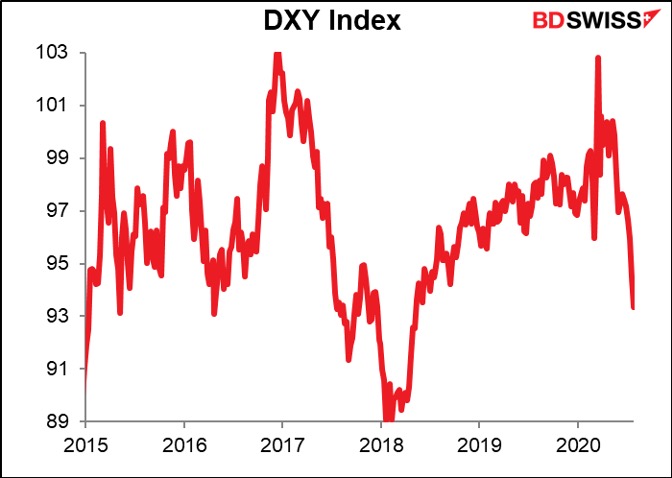

The focus of everyone’s attention has been the stunning plunge in the widely followed DXY index. This is an index of the nominal dollar’s value against six major currencies, mostly the euro (58%) yen (14%) and pound (12%), plus CAD, SEK and CHF. There’s no denying: it’s down 8.8% since its peak back in March. In July alone it fell 4.2%, its biggest one-month drop since September 2010.

This analysis is unfortunately based on three economic fallacies:

- Money illusion. The DXY index measures the nominal value of the dollar against these currencies, not its real, that is, inflation-adjusted value.

- Anchoring: Recent data tends to be an “anchor” for people’s way of looking at the world. We get used to what’s happening around us and tend to think of it as normal. Thus in this case, the DXY’s elevated level is taken as normal, and the recent fall is what has to be explained. But what if the higher level was the anomaly that needs to be explained and the fall is only natural – as it is in this case, IMHO?

- The DXY index is an inaccurate measure of the dollar’s strength We’ll get to that later.

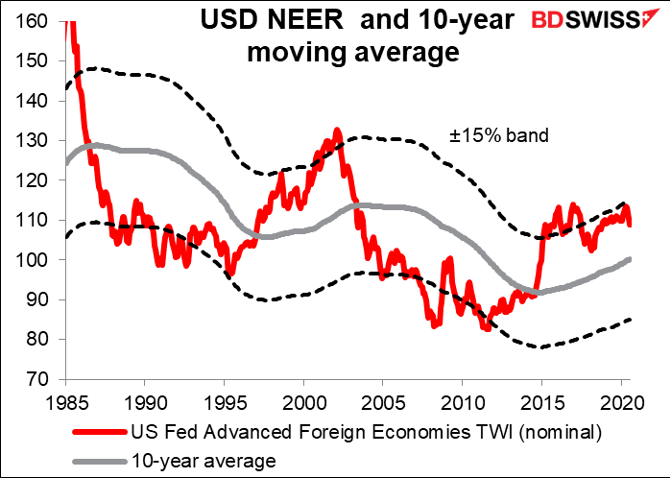

We can avoid all of these fallacies by looking at where today’s rates fit into the long-term history of the dollar’s real value. We’ll use the US currency’s real effective exchange rate (REER) against a broad group of the country’s major trading partners, as calculated by US Fed. A REER is a currency’s inflation-adjusted value against the currencies of the country’s significant trading partners, in this the case 26 countries (or zones, as in Eurozone) that each account for at least 0.5% of US bilateral trade. That’s a lot better way to measure the dollar’s value than an index in which one currency has over a 50% weighting. Would anyone measure a stock market with an index where one stock comprised over half the index?

Looking at this, we get at totally different picture. Back in April, the recent peak, the dollar’s real value was the highest it’s been in nearly 18 years (since October 2002, to be exact). That was the extraordinary move, not the recent decline.

Far from being a catastrophe that needs explaining then, the dollar’s 3.6% retracement from its April peak came almost right on schedule. In general, the US currency has reversed course when it got to ±15% of its 10-year average rate. That rule of thumb held this time as well.

One reason why people think the dollar is near collapse is because of the Fed’s “money printing” activities. Admittedly, the Fed has indeed been blowing up its balance sheet, but who hasn’t been? FX is a relative game, and relatively speaking, the Fed’s actions may have been primus inter pares, first among equals, but they were not unique. (I don’t even put the Bank of Canada on this graph, because they’ve expanded their balance sheet some 3x from its pre-crisis level!) Furthermore, for most currency pairs there’s little evidence that the relative expansion of the central bank’s balance sheet drives the relative value of the currencies.

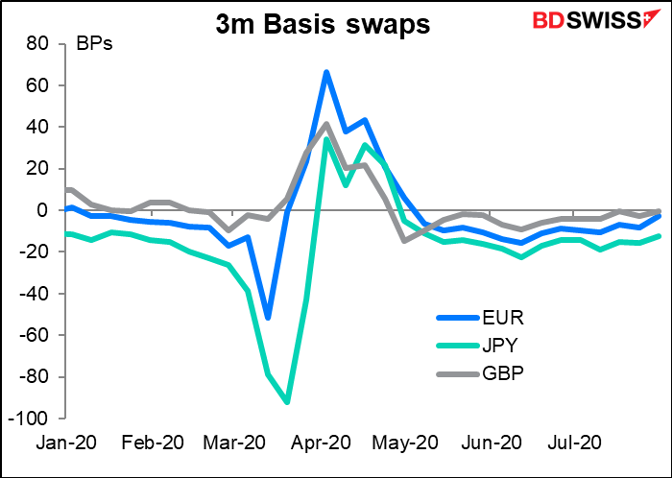

No, the fact that has to be explained is not the dollar’s sudden decline, but rather its sudden rise back in March and April. That’s an easy one, but not an obvious one. The problem was that foreigners had borrowed some $12.6tn in USD, partially by borrowing from banks and partly by issuing securities. They needed to get dollars to pay the interest on these borrowings. Furthermore, investors who owned USD securities – principally Japanese investors – need to get dollars to hedge their investments.

The resulting scramble for dollars pushed the value of the US currency up. In particular, borrowers who couldn’t get any dollars from their banks – which suddenly found their balance sheets blown up as every company with a credit line drew it down simultaneously to provide working capital – turned to the FX swap market to get dollars. That is, they bought dollars now with an agreement to repay them later. This sent the FX basis swap rates – the cost of doing this trade –soaring (or plunging, to be more accurate).

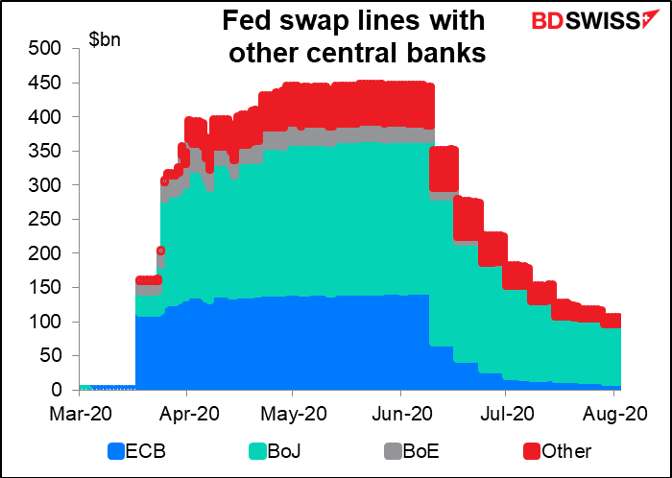

Eventually the Fed got into the act. It activated or reactivated swap lines with 14 central banks so that they could supply dollars to their local borrowers. Hey presto! $449bn later, the anomaly in the FX swap market disappears and the dollar falls back. (See Bank for International Settlements (BIS) Bulletin #1, Dollar funding costs during the Covid-19 crisis through the lens of the FX swap market )

Finally, the ultimate reason why I think this whole issue is nothing to get excited about: the DXY index is not an accurate measure of even the dollar’s nominal value, much less its real value. The weightings of each currency were set in 1973 and only revised once when the various European currencies were rolled into the euro.

The Fed’s Advanced Foreign Economies Dollar Index (nominal) measures the same currencies (plus AUD) but uses very different weightings and comes up with a very different result. As mentioned above, the euro accounts for 57.6% of the DXY but only 38.5% in the Fed index. On the other hand, CAD has a 9.1% weighting in the DXY and 28.1% in the Fed index, apropos of Canada’s position as the #4 trade partner of the US (after the EU, Mexico, and China). This nominal index tells a very different story than the DXY: it was down only 1.34% in July and off 4.2% from its April peak. This is hardly anything to get excited about.

In short, a more accurate measure of the dollar’s nominal value tells similar story to the real index: the dollar has been skating along the limits of its normal range for quite some time and some reversion to the mean is not at all surprising.

But that conclusion doesn’t get many clicks, does it?

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Marshall Gittler

Marshall Gittler: Head of Investment Research at BDSwiss Group -- Marshall is a renowned expert in the field of fundamental analysis, with over 30 years’ experience researching the markets. His career spans a range of elite investment banks and international securities firms including UBS, Merrill Lynch, Bank of America and Deutsche Bank. Marshall has established himself as global thought leader, educating and delivering high level FX research, helping traders to make the best trading decisions.

Read Marshall's Bio