Credit: Shutterstock photo

Credit: Shutterstock photoBy Khursheed Brothers :

I'd like to preface by saying I'm a graduating high school senior, and I'll be matriculating to the University of Pennsylvania this fall, which has a Barnes & Noble Education ( BNED ) affiliated bookstore. During my correspondence to the university and my visit to UPenn in April, the bookstore was so integrated with the university - both the physical campus and the online infrastructure - that I was surprised to discover it was actually managed by a separate company. Based on both my personal experience and my analysis, I truly believe BNED is an attractive buy with tremendous upside at this price that fits both Warren Buffett's definition of a competitive advantage and his definition of cheap. Before I get into my analysis, however, I'd like to address some concerns put forth in other articles written in the past.

Secular Downturn

This phrase has been thrown around a lot to justify a takeover of the retail industry by the all-powerful and ubiquitous internet, specifically Amazon ( AMZN ). However, BNED does not operate in a traditional retail industry. Firstly, it's a specialty retail focusing on university merchandise and textbooks. Amazon has been selling textbooks for as long as I've been alive, yet traditional textbook companies are still thriving and BNED didnt reporta decline in its bottom line until 2014. Secondly, BNED operates a monopoly within the university when it comes to university apparel; general merchandise accounts for almost half of its total sales. And although textbook sales are decreasing, textbook rentals are poised to continue increasing. Any college student will tell you that their university bookstore is a hub for students and tourists alike, similar to anchor stores in malls, and this is not likely to go away any time soon. Finally, many cite the proliferation of cheap online resources to replace traditional textbooks, but a study showed that 77% of students prefer using a textbook, digital or otherwise.

Competition from Amazon, Chegg and other online retailers

It is no surprise that online retailers are skidding into this market, but again, I'd like to point out that although BNED has been competing with these retailers for years, a material impact from this "competition" only occurred a few years ago. Also, BNED has an advantage that these other companies do not and that is integration with the university software and infrastructure. To give an example, here is a picture from my orientation packet from UPenn:

The university bookstore is usually the fastest way to obtain textbooks, especially important seeing as students typically know which textbooks to get only days before or the day classes begin. The feasibility of BNED's entrenched system along with its price matching program are the drivers of its competitive advantage over other online retailers. I would contend the much more threatening competition to the university bookstore culture is student-to-student and other third-party transactions; however, seeing as there is a gradual shift to renting textbooks over buying them, I believe this mitigates this form of competition.

Bad Business Model

I've seen this one on virtually every Seeking Alpha article on this company. The most cited evidence of this is a perpetual decline in comparable store sells. However, I think these numbers are misleading: they are not indicative of a deteriorating performance and are instead indicative of a changing retail environment. It is evident that more students now prefer to rent textbooks over purchasing them. Typically, renting a used textbook runs at about 40-50% cheaper than buying a textbook. Therefore, the decline isn't necessarily less foot traffic, or bad decisions on the management's part; it's changing consumer tastes and we should be happy management is adapting to that by increasing its rental inventory.

So What's Wrong with BNED?

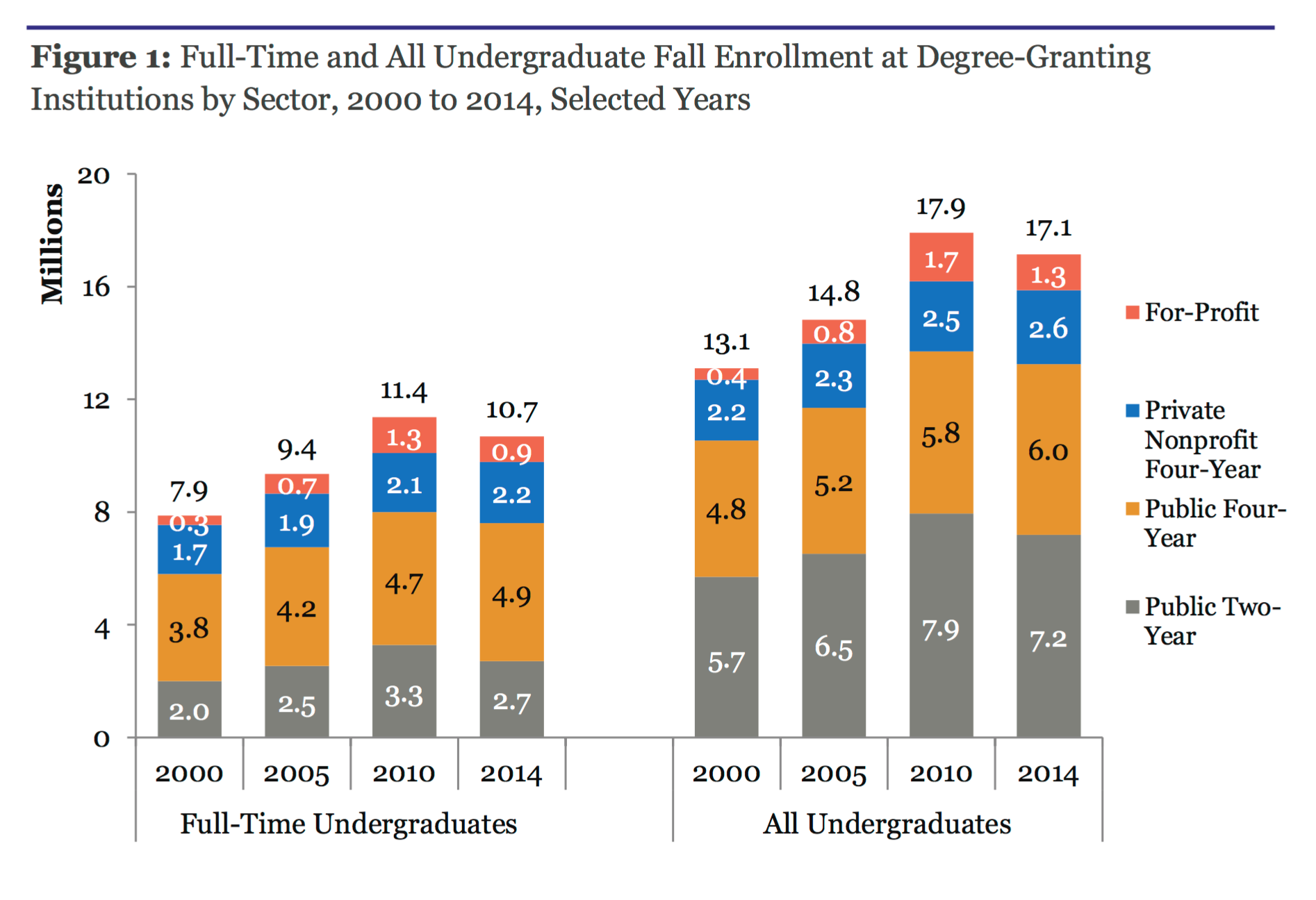

I mentioned that there was no noticeable hit on BNED's earnings until 2014, when it reported $34 million in earnings, about a 40% decrease from the previous year. I explained why I don't think this was caused simply by increased competition with Amazon; if that were the case, why didn't BNED show a decline earlier? Something must have happened during 2014… Lo and behold, 2014 was the year student enrollment in post-secondary institutions reversed its aggressive growth:

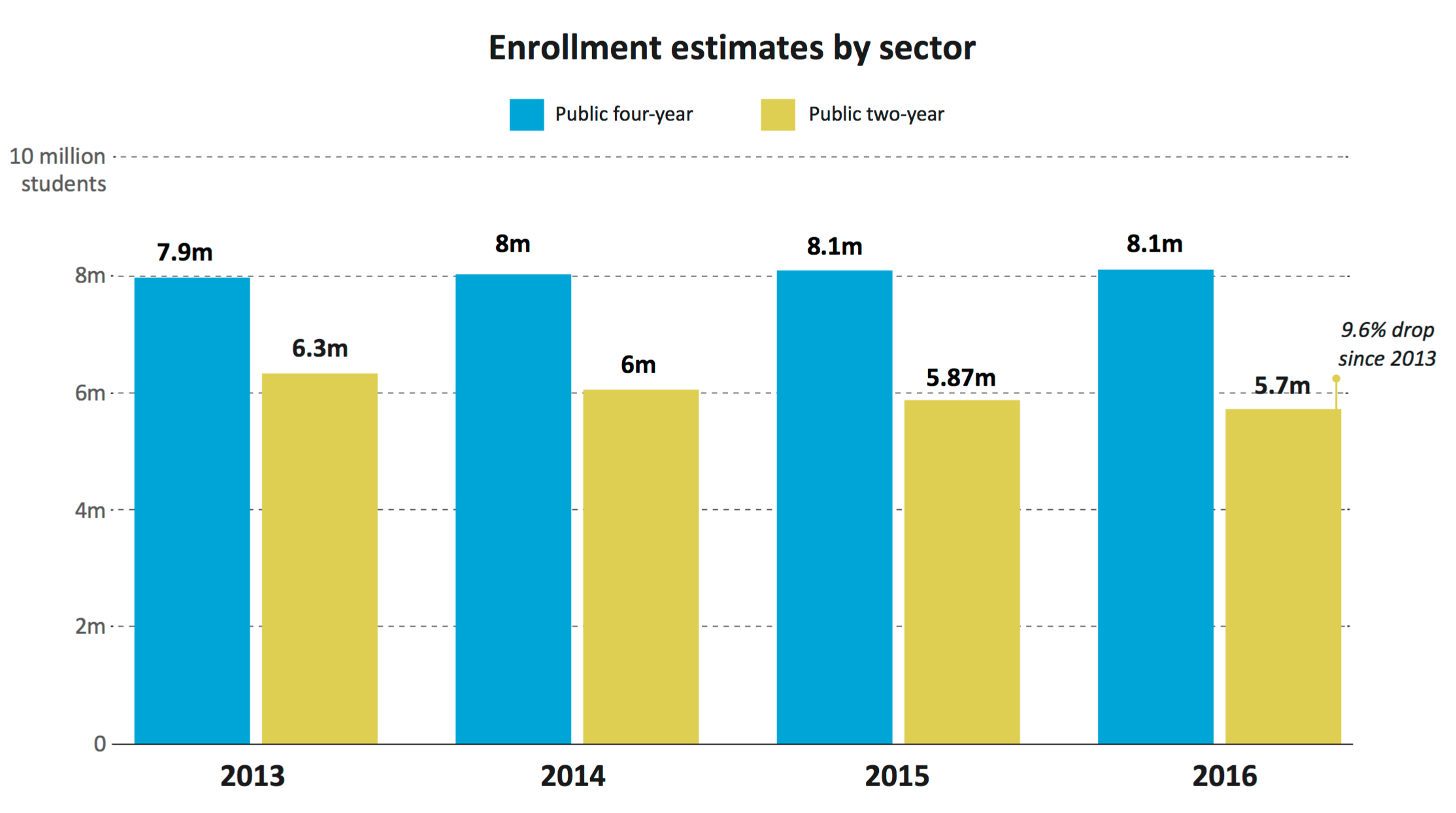

If we look at the numbers more closely, we see that since 2013, there has been a 9.6% drop in student enrollment in public 2-year post-secondary institutions:

Let us run some rough numbers to examine the severity of this decline. 2016 revenue was $1.8 billion. BNED impacts about 5 million students so the revenue per student is $360. The decline from 2010-2014 was 0.8 million students. BNED captures about 25% of the market so BNED lost out on 200,000 students (ignoring effects of potential growth during this same period). That's $72 million in potential revenue - multiplying it by the 5-year average gross margin of 15% and we have $10.8 million of lost income.

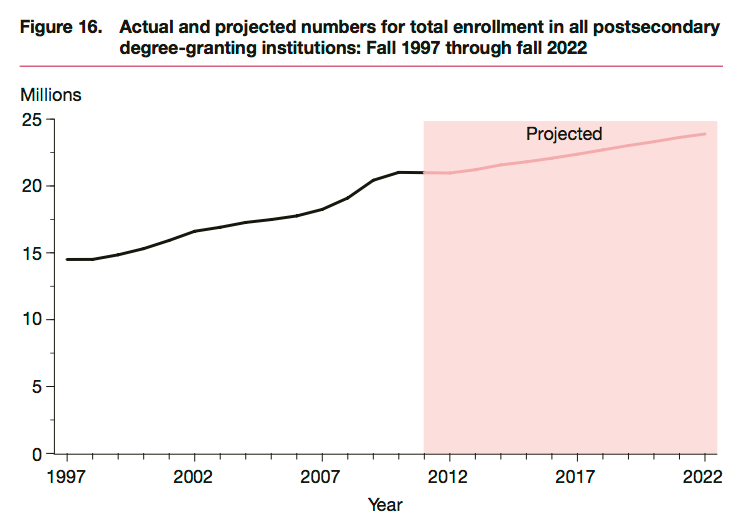

Now, it would be great if this trend were to reverse. Fortunately, it will. The National Center for Education Statistics predicts that total post-secondary education enrollment will increase by 14% from now until 2023 (links here and here ):

Does this pass the reasonability test? Well, in today's increasingly competitive, globalized job market, a college education is indispensable for anyone who seeks a high paying career. In addition, while there has been a recent trend of de-funding of public institutions, federal financial aid programs have increased and endowments for private institutions have been on the rise. In addition, the market itself is increasing: the number of high school graduates is skyrocketing (you can find the data on this in the link above) and the expectation of a college degree is almost universal. From a personal standpoint, more and more high schoolers have college as the end goal rather than graduation, and I do not believe this was the case a while back. In light of these facts, I can stand behind this projection.

Valuation

I begin by valuing the assets. I make no adjustments to current assets and net PPE to get a value of $987 million. Then, I value goodwill and other intangibles at $0. However, I do believe that Barnes & Noble Education benefits from the exclusive contracts it has with universities to integrate its digital systems and sell merchandise. The biggest adjustment will come from this.

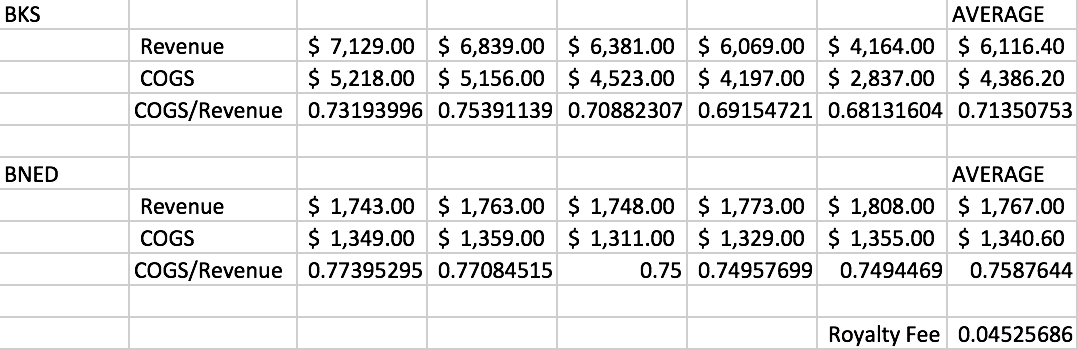

In all the SEC filings I've read, I could not find how much BNED pays universities for these contracts. All we know is that it pays a percentage of its sales to the university, contained in the Cost of Goods Sold ((COGS)) entry. Therefore, I took BNED's closest counterpart, Barnes & Noble (NYSE: [[BKS]]) and found its average COGS/Revenue for the past 5 years, and did the same for BNED. I subtracted the averages to find the estimated extra cost going into royalties to universities, which came out to be about 4.5%.

In estimating the value of the 770 contracts, let us analyze how much a new entrant would have to pay to recreate these same contracts. The company made $1.8 billion, meaning it paid $81 million in royalty fees. The average contract with a university lasts anywhere between 1 and 15 years. Let's assume the average contract is 7 years with 94% of contracts renewed at their end; therefore, BNED spends about $567 million over 7 years to maintain its current contracts, which is about $460 million when discounted at a rate of 5%. In addition to the hard assets, therefore, a new entrant may likely need to produce additional capital upwards of $400 million in order to also obtain the same university contracts as BNED.

Although this is by nature a hypothetical number, I want to stress that BNED enjoys a monopoly within each university, and it must maintain this monopoly through these contracts. There are a few reasons it is important to place a value on this. First of all, look at BKS: it has no competitive advantage that I can think of and its bottom line has been falling, and its stock has fallen 40% over the past year. During this same time, BNED has been producing a profit, albeit small but still a profit. Taking into account how similar these bookstores are, it's the university contracts that create this difference despite BNED having higher costs than BKS. Secondly, we must analyze the overarching market BNED operates in: the market in which universities are the target customers. That market is essentially a duopoly with Follett Corp. and BNED commanding ~70% of the market. The question we need to ask ourselves is why it's a duopoly, especially with many smaller, low cost retailers seeking market share? Well, I believe it is because of the university's switching costs since the bookstore is so integrated within the university's infrastructure - think of Apple ( AAPL ) and iCloud. In light of this, I feel justified in valuing this intangible asset.

Adding $460 million to the $987 million and subtracting liabilities yields a reproduction value of $660 million, or $14 a share, a 40% upside. Looking at it from an enterprise value perspective, the enterprise value of this firm is $342 million. Bruce Greenwald writes in his book that if you can buy a firm for less than its reproduction value, you may have found yourself a good investment opportunity. If you look at it from an earnings perspective, adjusting for cash inflows/outflows and one-time charges, I came up with normalized earnings of $31 million, and it isn't uncommon for a company like BNED with virtually no debt to be trading at P/E's upwards of 20. Finally, if you analyze the quarterly reports for this year, you'll see signs of both increased earnings as well as increased cash flow, further strengthening BNED's balance sheet. Any way you look at it, BNED is trading for an attractive price, and is likely to appreciate in value once headwinds in the post-secondary education market clear out, and signs of this reversal are already becoming noticeable.

See also Ultra Petroleum ( UPL ) Presents At 2017 Wells Fargo West Coast Energy Conference - Slideshow on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}