Automatic Data Processing, Inc. ADP reported better-than-expected second-quarter fiscal 2023 results.

Adjusted earnings per share of $1.96 beat the Zacks Consensus Estimate by 0.5% and grew 19% from the year-ago fiscal quarter’s reading. Total revenues of $4.4 billion beat the Zacks Consensus Estimate by 0.3% and improved 9.1% from the year-ago fiscal quarter’s reading on a reported basis and 10% on an organic constant-currency basis.

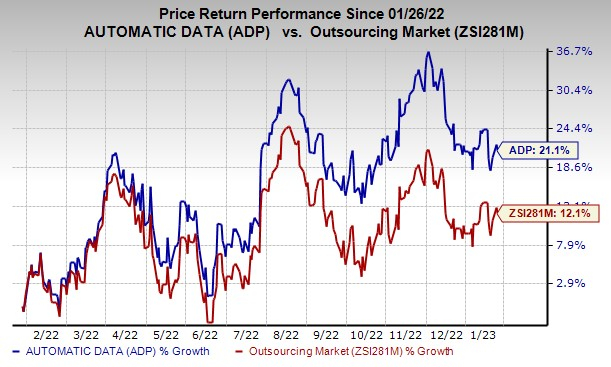

Over the past year, shares of ADP have gained 21.1% compared with 12.1% growth of the industry it belongs to.

Image Source: Zacks Investment Research

Let’s check out the numbers in detail:

Segments in Detail

Employer Services’ revenues of $2.9 billion increased 8% on a reported basis and 10% on an organic constant-currency basis. Pays per control increased 5% from the year-ago fiscal quarter’s reading.

PEO Services’ revenues were up 11% year over year to $1.5 billion. Average worksite employees paid by PEO Services were 711,000, up 8% from the year-ago fiscal quarter’s reading.

Interest on funds held for clients increased 77% to $187 million. ADP’s average client funds balance increased 4% to $33.4 billion. Average interest yield on client funds expanded 90 basis points to 2.2%.

Automatic Data Processing, Inc. Price, Consensus and EPS Surprise

Automatic Data Processing, Inc. price-consensus-eps-surprise-chart | Automatic Data Processing, Inc. Quote

Margins

Adjusted EBIT increased 15% from the year-ago fiscal quarter’s reading to $1.1 billion. Adjusted EBIT margin grew 120 basis points to 24.3%.

Margin of Employer Services and PEO Services increased 170 bps and 130 bps, respectively.

Balance Sheet and Cash Flow

ADP exited second-quarter fiscal 2022 with cash and cash equivalents of $1.35 billion compared with $1.21 billion in the prior fiscal quarter. Long-term debt of $2.99 billion was flat sequentially.

Automatic Data Processing generated $900 million of cash from operating activities in the quarter. Capital expenditures were $49.7 million. ADP paid out dividends worth $432.6 million and repurchased shares worth $220.2 million in the reported quarter.

Fiscal 2023 Outlook

ADP still expects revenues to register 8-9% growth. Adjusted EPS is still expected to register 15-17% growth. Adjusted effective tax rate is estimated to be approximately at 23%.

Automatic Data Processing expects Employer Services revenues to grow at a rate of about 8-9% (prior view: 7-8%), while PEO Services revenues are still expected to grow at 8-9% rate (prior view: 10-12%).

Currently, ADP carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Stocks to Consider

Some better-ranked stocks worth considering in the broader Zacks Business Services sector are Paychex, Inc. PAYX and DocuSign, Inc. DOCU.

Paychex carries a Zacks Rank #2 (Buy) at present. PAYX has a long-term earnings growth expectation of 7.5%.

Paychex delivered a trailing four-quarter earnings surprise of 5.9%, on average.

DocuSign is currently Zacks #1 Ranked. DOCU has a long-term earnings growth expectation of 13.7%.

DOCU delivered a trailing four-quarter earnings surprise of 6.6%, on average.

Zacks Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>Paychex, Inc. (PAYX) : Free Stock Analysis Report

Automatic Data Processing, Inc. (ADP) : Free Stock Analysis Report

DocuSign (DOCU) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.