Key Points

Amazon and Microsoft stock have both fallen around 20% from their highs, due to fears over AI spending.

Amazon's backlog will take years to fill, while Microsoft's cloud division is growing rapidly.

Both stocks now trade at reasonable earnings multiples.

- 10 stocks we like better than Microsoft ›

The narrative around artificial intelligence (AI) disruption is reaching a breaking point. Many software stocks are falling precipitously amid fears about the future of virtually every sector. We are getting to a point where rational analysis has been thrown out the window.

Even the two largest cloud companies in the world have seen their stocks fall from recent highs. Both Amazon (NASDAQ: AMZN) and Microsoft (NASDAQ: MSFT) stocks now trade down 20% or more, despite being the premier data center providers for the AI revolution.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Over the next few years, these two companies should see strong growth in their cloud divisions as they race to fulfill their massive backlogs. Does that make both Microsoft and Amazon no-brainer buys this month?

Image source: Getty Images.

Amazon's huge spending plans

Amazon is planning to spend $200 billion on capital expenditures in 2026. This is going to flip free cash flow from positive to negative, spooking Wall Street.

The astute investor focused on the long term should see this as a bullish development. Amazon Web Services (AWS) is booked out with AI demand for years at its current capital spending rate, according to division leader Matt Garman. This means the company will be running at full throttle even as it spends $200 billion annually to build data centers.

AWS revenue grew 24% year over year last quarter and posted $129 billion in sales in 2025. If this same revenue growth can be maintained over the next three years, the AWS division alone will be generating close to $250 billion in revenue in 2028. This does not include the massive retail operation Amazon has built with its e-commerce platform, either.

Cash flow is going to be hit in the short run. However, over the long term, AWS will be a huge profit driver for Amazon.

A precarious AI relationship?

Microsoft was one of the first big movers in AI, establishing a tight relationship with start-up OpenAI, maker of ChatGPT.

Having ChatGPT as a customer and spending tens of billions of dollars on cloud computing has helped Microsoft Azure -- its competitor to AWS -- grow revenue by 39% year over year last quarter. This is faster than Amazon, but at a smaller revenue base (the exact figure for Azure revenue is not disclosed).

Investors are nervous about Microsoft's own AI capex plans, which should number around $150 billion in 2026. It has a strong relationship with OpenAI, but the start-up itself is taking enormous risks by burning a ton of cash to try to gain market share. In the long term, if OpenAI runs into financial trouble, Microsoft Azure may take a revenue hit.

This is something to monitor, but it does not kill Microsoft's overall business or potential in cloud computing. It has strong customer diversification and has been growing at a strong double-digit rate for more than a decade. The Intelligent Cloud division -- which encompasses Azure, but also includes SQL Server, Windows Server, and security solutions -- hit $32.9 billion in revenue last quarter. Productivity and business solutions, which include segments like the Microsoft 365 suite, hit $34.1 billion in revenue, up 16% year over year.

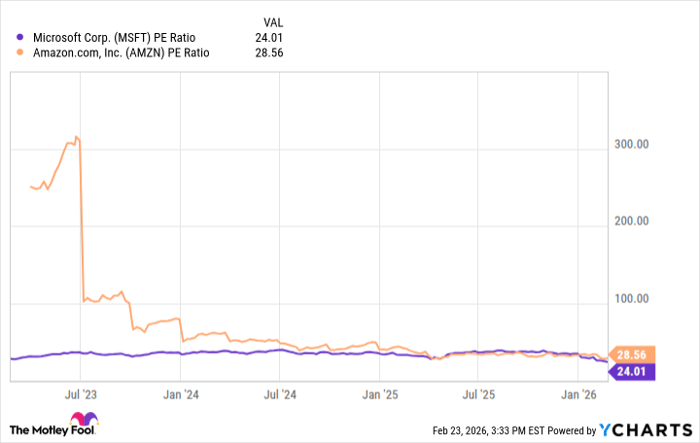

Data by YCharts.

Why these two stocks are no-brainer buys

Short-term concerns over AI spending and Microsoft's relationship with OpenAI are being overstated in the company's stock prices right now. These are diversified businesses with strong historical growth rates that are not reliant on one customer to succeed. As leaders in cloud computing, both stand to benefit tremendously from the AI revolution.

After taking these 20% haircuts, Microsoft and Amazon now trade at price-to-earnings ratios (P/Es) below 30 for the first time in many years. Microsoft has a P/E ratio of 24, while Amazon's is 28.5. However, over the long term, Amazon might look cheaper due to its potential to expand profit margins.

What's clear is that these are two fast-growing technology giants with significant competitive advantages and are now trading at reasonable prices. This makes them no-brainer buys for your portfolio today.

Should you buy stock in Microsoft right now?

Before you buy stock in Microsoft, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Microsoft wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $445,995!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,198,823!*

Now, it’s worth noting Stock Advisor’s total average return is 927% — a market-crushing outperformance compared to 194% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 26, 2026.

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.