The beloved Mag 7 group has cooled off in a big way over recent months after big multi-year runs, raising some eyebrows among investors.

While the group’s performance in 2025 has left much to be desired, consistently strong top and bottom line growth gives them staying power for many years to come.

And this week, a member of the elite squad, Alphabet GOOGL, is on deck to report quarterly results. But is the recent underperformance a buying opportunity? Let’s take a closer look at what to expect in the tech titan’s quarterly release and how it currently fares.

Advertising & Cloud Results Remain Key

Headline expectations for Alphabet have reflected an overall stable trend, with expectations primarily remaining unchanged over recent months. The current Zacks Consensus EPS estimate of $2.01 suggests 6.3% year-over-year growth, whereas forecasted sales of $75.5 billion suggests a 12% move higher.

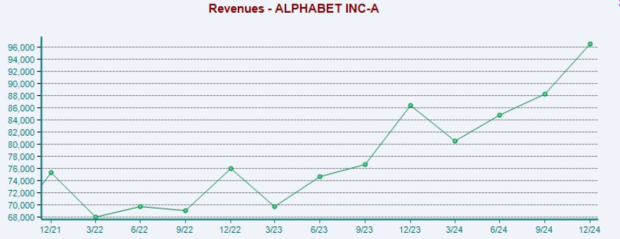

Below is a chart illustrating the company’s sales on a quarterly basis.

Image Source: Zacks Investment Research

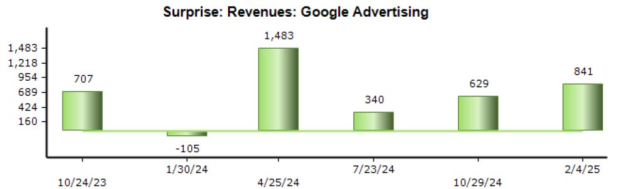

As usual, the company’s Advertising results will be a strong focus, which account for the bulk of Alphabet’s sales overall. For the period, the Zacks Consensus estimate for Advertising sales stands at $66.3 billion, reflecting 7.7% growth year-over-year.

As shown below, Alphabet has regularly exceeded our consensus expectations on the metric, with just one miss over the last six quarters. The company’s advertising results will likely be boosted by AI implementations that have delivered more relevant results for consumers.

Image Source: Zacks Investment Research

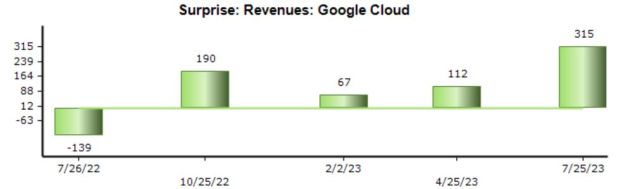

Another key metric to watch in the release is the company’s Cloud results, which have also been positive over recent periods. Our consensus estimate for Cloud sales stands at $12.1 billion, reflecting a 27% jump from the year-ago period.

The Cloud growth rate here is quite significant, though it does reflect a small deceleration from the prior period’s 30% year-over-year growth rate.

Image Source: Zacks Investment Research

Are GOOGL Shares a Buy?

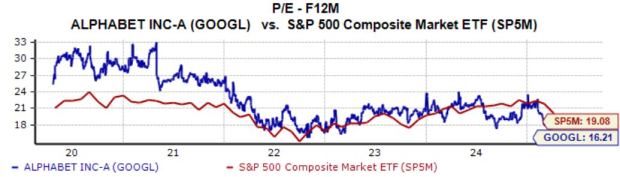

The above-mentioned risk-off environment over recent months has caused the company’s valuation multiples to come down significantly, with the current 16.2X forward 12-month earnings multiple reflecting a 15% discount relative to the S&P 500.

And the current PEG ratio works out to 1.0X, rounding out the valuation picture nicely.

Image Source: Zacks Investment Research

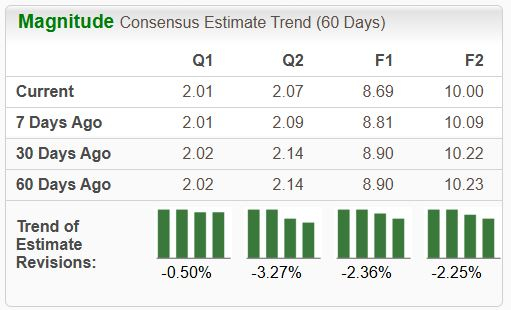

While the valuation picture remains attractive on a relative basis, Alphabet’s EPS outlook has taken a hit across the board over recent months, a bearish signal from analysts. Positive guidance and commentary during theearnings callcan certainly shift the earnings picture from negative to positive, and investors with a near-term timeframe should wait for more clarity.

Image Source: Zacks Investment Research

Bottom Line

Beloved Mag 7 member Alphabet GOOGL is on deck to report quarterly results this week, with investors looking for clarity following a rough start to 2025. Analysts haven’t moved their EPS and sales expectations much for the period to be reported over recent months, with the valuation picture remaining fair.

While the downward pressure has delivered an opportunity to scoop up shares at a discount, investors should remain cautious in the near term given the negative EPS outlook. From a long-term standpoint, there is no doubt that the stock will remain a strong selection for any portfolio given its immense earnings and sales power that will stay for years to come.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2024. While not all picks can be winners, previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Alphabet Inc. (GOOGL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.