No matter how or where you grew up, it’s likely you’ve been at the receiving end of well-meant financial tips intended to put you on the path to responsible spending, a balanced budget and a nest egg at the end of your working road. Yet a lot has changed in the past three years alone, from the Great Resignation to worldwide inflation and financial instability.

It’s time to rethink these six outdated money rules for a healthier relationship with your money.

1. Buy instead of rent.

The pandemic turned the housing market on its head, and three years later, mortgage rates are the highest in a decade. While rents are also climbing, a recent report from Realtor.com suggests that renting is more affordable than buying in 45 of the 50 largest cities in the US — some $800 less a month on average.

It’s not just high-cost living areas like New York City. The top five cities of Austin, San Francisco, Seattle, San Jose and San Diego offer the largest monthly savings for renters.

Homeownership continues to be among your best ways to build long-term wealth, offering tax advantages and the ability to build equity you can borrow against later. But it’s not something you want to rush. It requires good credit, a down payment of 20% or more and savings for taxes and upkeep, something renting can offer you time to build.

If you have the kind of job that allows you to work from anywhere, renting also affords flexibility to test out your dream cities before putting down roots. Just make sure you’re using the time to save toward your future.

2. Always keep a balance in your savings account.

This tip isn’t bad advice on its own, but there’s nuance as to where you save your money — and it shouldn’t be in an everyday savings account.

“Keeping a balance in your savings account might help you resist the temptation to spend it, but it doesn’t mean you’re taking full advantage of your earning potential,” says banking expert and certified anti-money laundering specialist Alexa Serrano Cruz.

While the national average savings rate is 0.35% APY, large banks are offering abysmal rates as low as 0.01% APY on standard savings. A stronger option for your nest egg is a high-yield savings account — or an HYSA.

Both traditional savings and HYSAs offer safe access to your money and the security of FDIC-insured savings. Yet HYSAs offer much higher APYs than your standard savings account, the best high-yield accounts offering 5% or more. “That’s about 14 times higher than the average,” explains Serrano Cruz.

Add no fees, small minimums and the ability to easily move your money among accounts — even those at other banks — and a high-yield account is a more valuable way to leverage your cash toward bigger savings goals.

3. Mutual funds are your best investment.

Mutual funds continue to be a popular choice for investors, offering diversification across stocks, bonds and other assets with minimal risk and a low bar to purchase. Still, you could be missing out on significant opportunities by investing in mutual funds alone.

Investments expert Matt Miczulski suggests ETFs as a potentially better option for investors.

“Take all the best features of a mutual fund, but include lower fees and more flexible trading — that’s an ETF,” explains Miczulski. “ETFs behave much like mutual funds and share many benefits, but typically with more tax efficiency, greater liquidity and lower fees.”

Taxes on ETF investments have been historically lower than those for mutual fund investments, according to the US Securities and Exchange Commission. And you can trade ETFs anytime the market is open, making them a convenient and more liquid investment option.

But no investment is without risks. Search the SEC’s Electronic Data Gathering, Analysis and Retrieval System for a mutual fund or ETF to understand the prospectus, investment strategy and risks before you buy.

4. Carry a balance on your credit card.

A credit card can be a way to increase your credit score with responsible spending and on-time payments.

But you don’t need to carry a balance to build credit, says personal finance expert Steve Dashiell. “What’s most important to credit bureaus is that you’re making your payments on time and keeping your credit utilization ratio below 30% month-to-month.”

Your credit utilization ratio represents the amount of revolving credit you’re using — or how much you owe on credit cards and other balances that vary monthly — divided by the total credit available to you. Rule of thumb is to keep your ratio under 30%. But the lower, the better to protect your credit score.

“Card balances can accrue interest if you’re not paying your statement balance each month,” adds Dashiell. “Instead, you can simply use your card and pay that statement balance each month. If that leaves you at $0 on your balance, it will still reflect positively on your credit score.”

To maximize your spending, look for a rewards card that offers cash back or points in categories like travel or groceries, no matter if you pay it off in full.

5. Don’t be a job-hopper.

TikTok user @sasssquashh went viral in early February for explaining why she changes jobs so frequently. Her reasons fit squarely in the top three reasons US workers told the Pew Research Center they’d left their jobs in 2021 — low pay, no advancement opportunities and disrespect at work.

She’s right on that first account: Switching jobs may be the most effective way to beat inflation if your salary isn’t keeping up with rising costs. Of Americans who switched employers between April 2021 and March 2022, half said they saw a net pay increase of 9.7% or more to their paycheck, according to Pew.

Job-hopping isn’t the stain on your resume that it once was, and it’s gained momentum as younger employees demand better working conditions, a healthier work–life balance and more fulfilling careers — all reasons prospective employers may understand.

And while it’s ideal to have a job lined up before you quit, if your job is negatively affecting your mental health or life at home, it may not be worth securing another offer before you leave. Of the roughly 25% of Americans who say they left a job in the past year, 3% admitted to quitting without another offer, according to the Finder Consumer Confidence Index, a quarterly survey of US consumer attitudes on wealth, debt, savings and work. It’s not unreasonable to assume it was the better option professionally and personally.

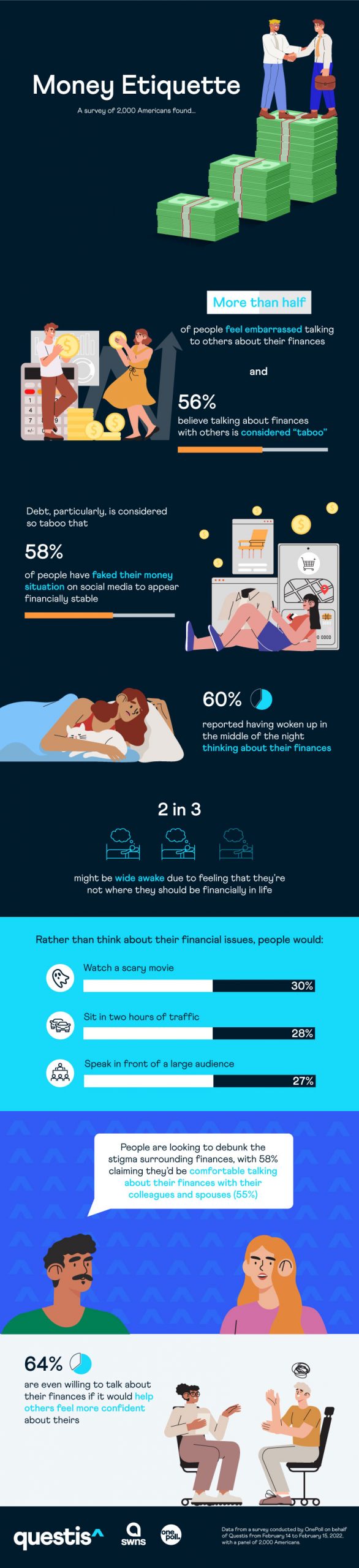

6. Never talk about money.

More than half of all Americans believe that talking about finances with others is “taboo,” according to a Questis survey of more than 2,000 people. At the same time, 58% of those respondents said they’d be comfortable talking about money with their colleagues and spouses if it were to debunk the stigma around finances.

And that is the No. 1 reason for breaking the financial silence: By not talking about money, you’re less informed about ways of managing your own wealth and not as strongly positioned to share what you know to benefit the people you care about — including younger people in your life. Confident financial literacy can mean the difference between budgeting success and falling into debt.

Same goes for your paycheck. You have the legal right under the National Labor Relations Act to talk about your salary among coworkers. Clear benefits to talking about your salary — with discretion, of course — include a better understanding of your value and a stronger position from which to ask for a raise. It can help you, your colleagues and people in your industry.

In the wake of last week’s Equal Pay Day on March 14, a day designed to raise awareness of wage gaps, pay transparency is also a way to help fix persisting income inequality among historically underpaid workers, including women and those within the BIPOC and LGBTQ communities.

The money move MVP

If you’re looking for the secret to wealth that transcends budgets, generations, jobs and where you live, it’s this: Spend less than you earn, and save the difference where it makes sense for your lifestyle. Even seemingly small amounts socked away can help you build a buffer for the unexpected in the short term — and help you invest in your future self and financial goals.

Sources

Here’s why salaries in the U.S. don’t keep up with inflation, December 14, 2022, CNBC

Majority of workers who quit a job in 2021 cite low pay, no opportunities for advancement, feeling disrespected, March 9, 2022, Pew Research Center

Majority of U.S. workers changing jobs are seeing real wage gains, July 28, 2022, Pew Research Center

Money etiquette infographic, OnePoll survey on behalf of Questis conducted February 14 to February 15, 2022

{kind=link}

Mutual funds and ETFs: A guide for investors, US Securities and Exchange Commission

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Finder

Finder is a global financial technology platform which allows members to save, invest and spend via the Finder mobile app and website. Finder’s mission is to help people make better financial decisions and work with partners to connect via API into the Finder platform to offer saving and investment services and products. Finder was founded in Australia in 2006 and now operates in 50+ countries with 2,600+ product partners and 10+ million visits every month, serviced by 500+ crew passionate about helping our members achieve their full financial potential.

Read Finder's Bio