It was 50 years ago today that Nixon met at Camp David with Fed Chair Arthur Burns, incoming Treasury Secretary John Connally, and then Undersecretary for International Monetary Affairs (and future Fed Chair) Paul Volcker and decided to close the gold window, thus ending the Bretton Woods system of exchange rate management.

Nixon went on TV on Sunday while financial markets were closed and announced that “I have directed Secretary Connally to suspend temporarily the convertibility of the dollar into gold or other reserve assets, except in amounts and conditions determined to be in the interest of monetary stability and in the best interests of the United States.” That “temporary” action has proved to be quite long-lasting!

The “Nixon Shock” permanently altered the global financial system. Nixon gave countries their monetary sovereignty. With the ending of the Bretton Woods system of fixed exchange rates, a system of individual currency management practices previously unknown except during wartime has now become embedded in the global financial landscape.

If you’re interested in the history of that decision, what led up to it and how it was made, you can read the history of it on the Fed’s website.

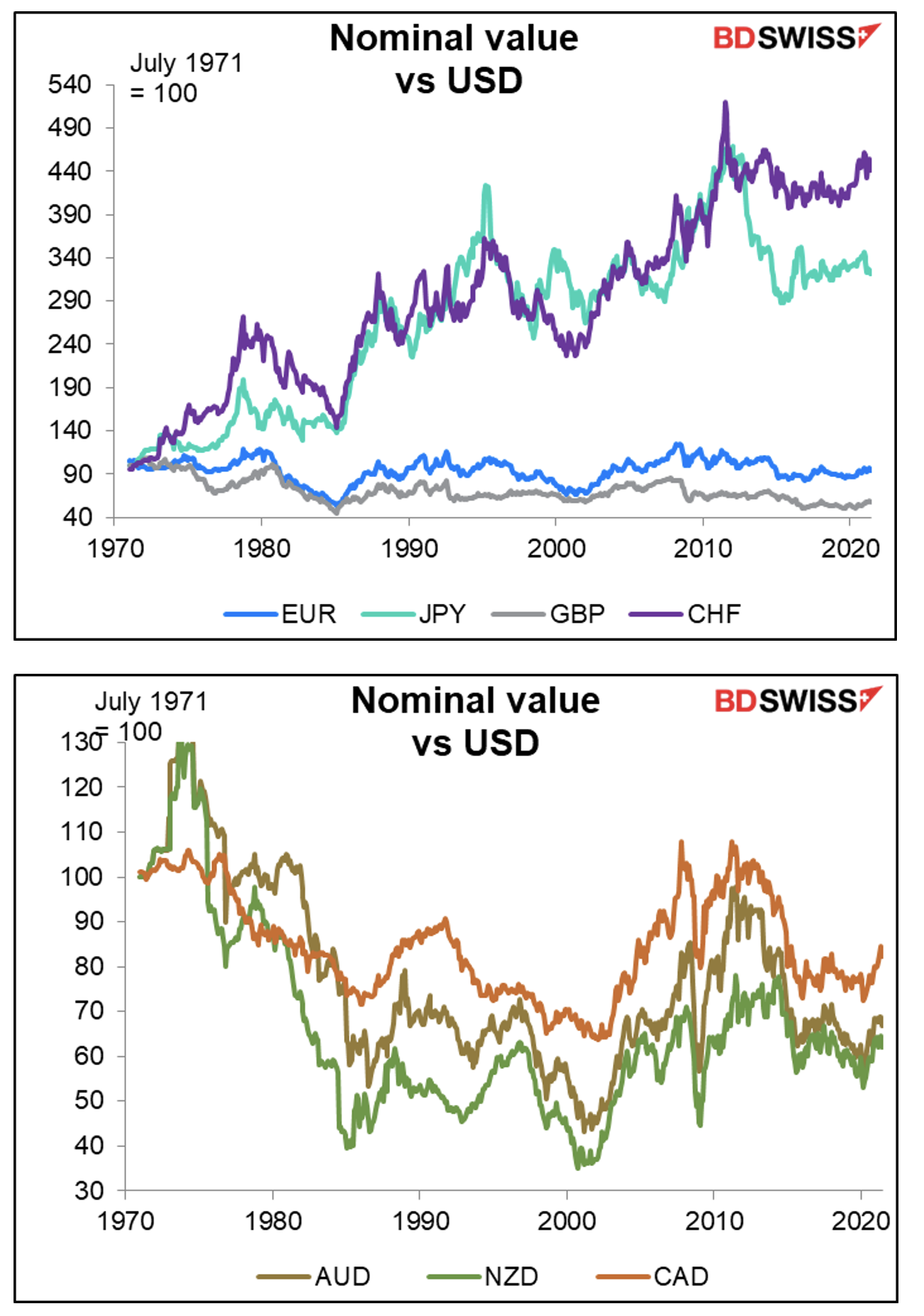

How have the major currencies fared under this system? Some have done better than others.

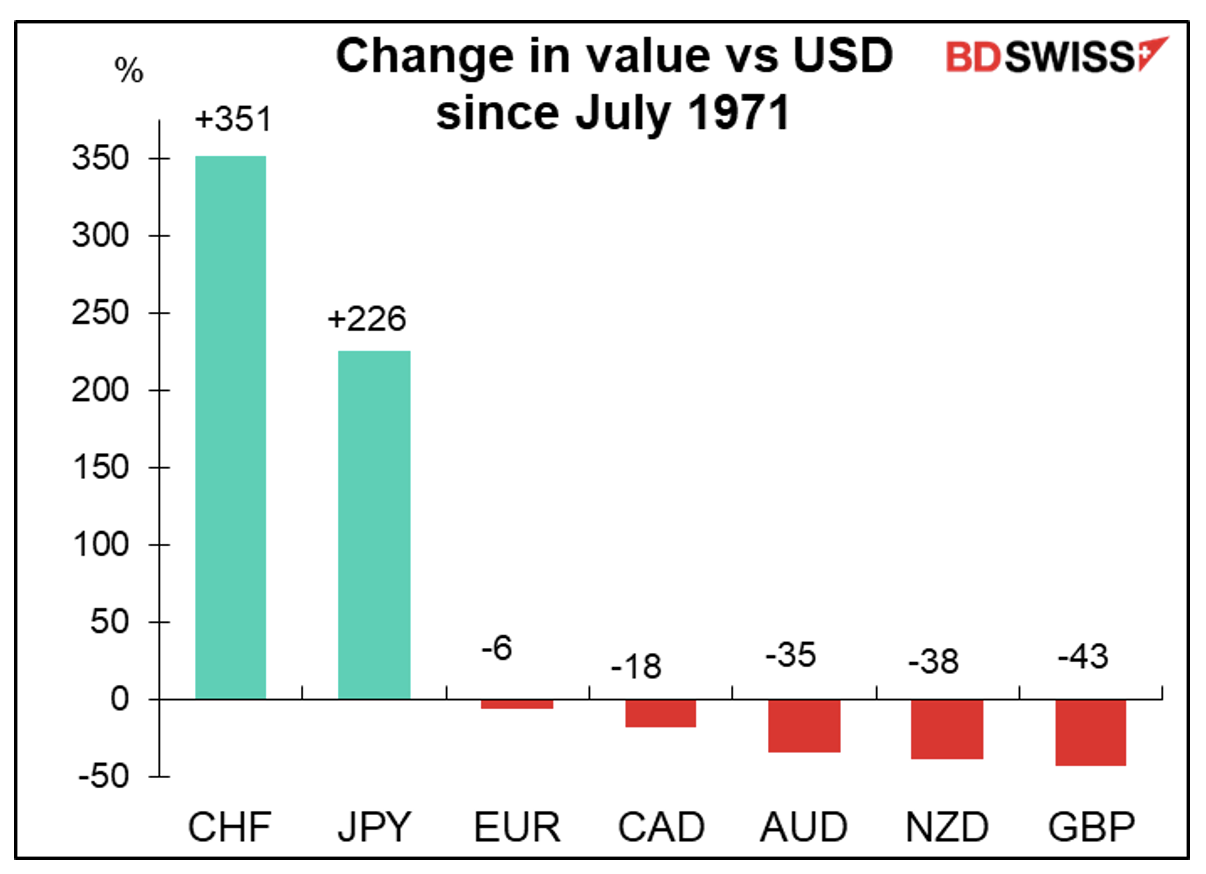

If we look at just the nominal value of the currency vs the dollar, then the Swiss franc and Japanese yen are the clear winners. The others have largely depreciated, with the pound the biggest loser. (The euro is artificially calculated before its launch.)

These changes represent only the price return. They don’t include interest payments and so don’t represent the total return one would’ve gotten from holding these currencies over this time period. I don’t have the data to make that calculation, nor is it available on Bloomberg. (I did run that calculation from August 1980 and came up with a totally different order: NZD was #1 and JPY, which has paid around zero interest since 1995, was last.)

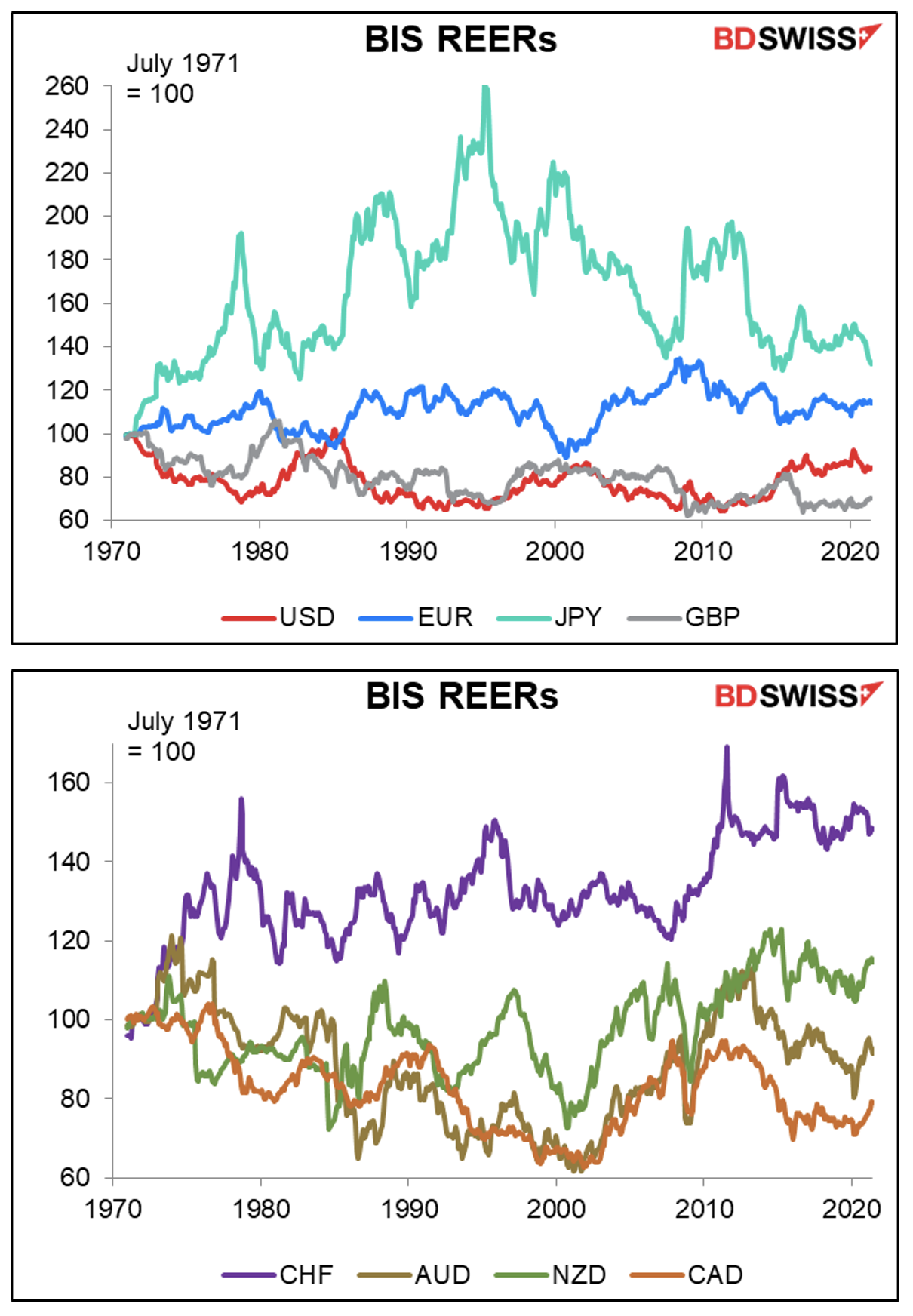

In any event, the changes in relative price of the various currencies are to some degree optical illusions because the inflation rates of the countries are different and the nominal value of a currency should naturally adjust to take that into account. For example: Let’s assume that USD 1 = JPY 100 and that a widget that costs $1 in the US costs JPY 100 in Japan. Let’s then assume that the U.S. has 5% inflation and Japan has 2% deflation. At the end of one year the widget will cost $1.05 in the U.S. and JPY 98 in Japan. For the real value of the USD/JPY exchange rate to stay the same, the nominal rate will have to move to 98/105= 93.33, or $1 = 93.33 yen. Did the yen appreciate or stay the same? The nominal value appreciated but the real value stayed the same.

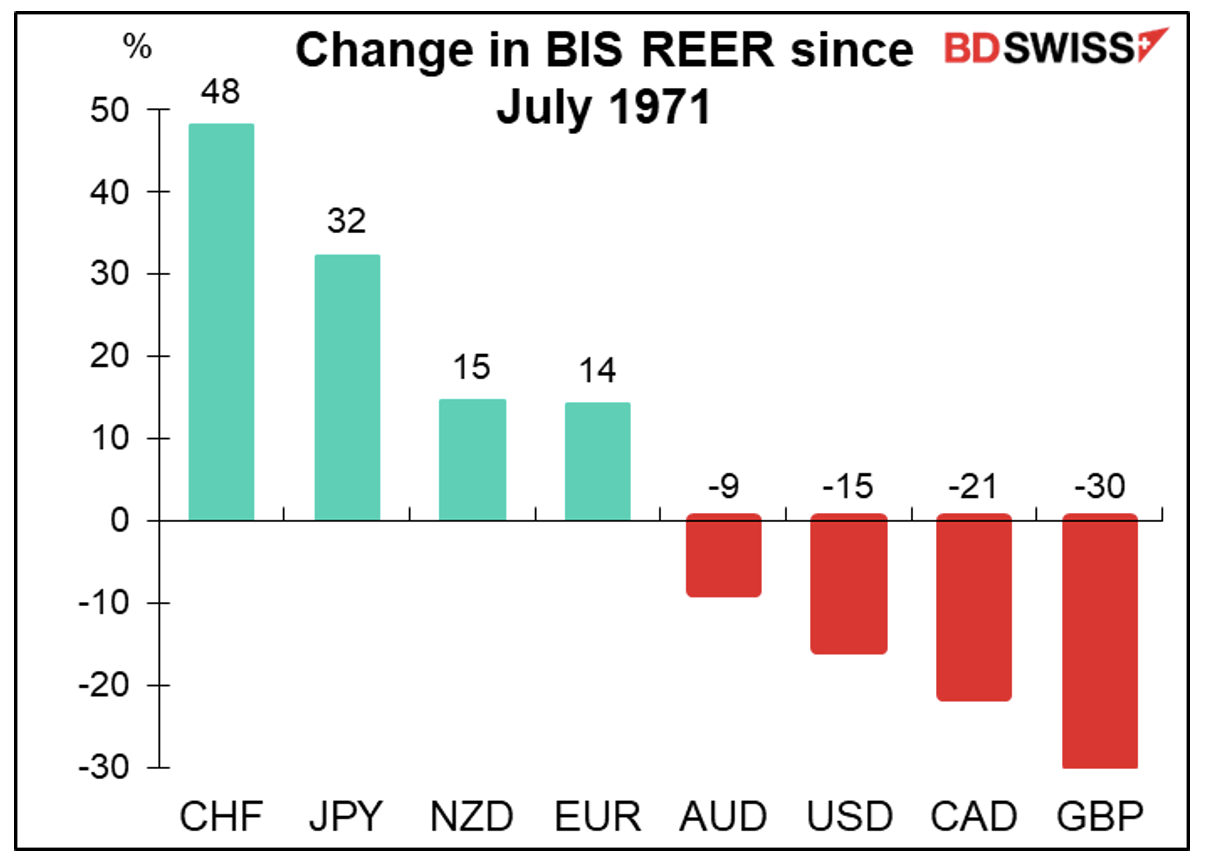

The Bank for International Settlements (BIS) calculates an index of the real value of each major currency against the currencies of its major trading partners (called the real effective exchange rate, or REER). On this basis, the NZD has done much better and the USD worse than the nominal changes would imply. The low-inflation CHF and JPY are still the overwhelming winners, although by no means as much, and the poor beleaguered pound the loser, albeit by less.

Not to show my age, but I was a high school exchange student in Japan when Nixon tore the global monetary system apart. The area where I was living, Fukui Prefecture, was hard-hit by the sudden appreciation of the yen. I lived near Sabae, the-then world’s capital for making eyeglass frames. Even today they make some 25% of the world’s eyeglass frames there, apparently. I had to make a speech to the local Rotary Club shortly after this event. Torn between loyalty to my President and the desire to placate my audience, needless to say I blasted Nixon’s perfidy as best I could in my poor Japanese. Given that I was near draft age and not a big fan of Nixon’s Vietnam policy, this bit of disloyalty did not cause me many sleepless nights.

I owe my career as a forex strategist to this event, so I’m quite grateful that Nixon did it.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Policy & Regulation Gold

Marshall Gittler

Marshall Gittler: Head of at BDSwiss Group -- Marshall is a renowned expert in the field of fundamental analysis, with over 30 years’ experience researching the markets. His career spans a range of elite investment banks and international securities firms including UBS, Merrill Lynch, Bank of America and Deutsche Bank. Marshall has established himself as global thought leader, educating and delivering high level FX research, helping traders to make the best trading decisions.

Read Marshall's Bio