About the Industry

The Zacks Financial Transaction Services industry is part of the Financial Technology or FinTech space, including companies with diverse natures of businesses. The industry comprises card and payment processing and other solutions providers, ATM services and money remittance service providers as well as providers of investment solutions to financial advisors. The players in this segment operate their unique and proprietary global payments network that links issuers and acquirers around the globe to facilitate the switching of transactions, permitting account holders to use their products at millions of acceptance locations. Monetary transactions are effectuated through these networks, offering a convenient, quick and secure payment method in several currencies across the globe. The industry is benefiting from the ongoing digitization movement triggered by the pandemic.

4 Trends that Remain Underway in the Financial Transaction Services Space

High Technology Expenses: The global shift toward contactless payment solutions continues to accelerate. In response, industry leaders are introducing cutting-edge payment innovations. These advancements have broadened customer access and diversified revenue streams, enhancing convenience. To remain competitive and sustain market leadership, significant investments in technology have become the need of the hour, thereby elevating the technology expenses of companies. Further, the widespread adoption of digital payments has heightened the risk of sophisticated cyber threats, posing significant challenges for both consumers and businesses. As a result, firms are prioritizing the development of secure payment systems, which further require technology investments. Though these measures are expected to fetch benefits in the long term, costs related to such investments dampen the margin growth of the industry participants.

Strain on Consumer Spending: Steady consumer spending implies increased utilization of financial transaction services, leading to higher transaction volumes and revenue growth for the industry participants. A flourishing e-commerce sector, driven by greater Internet accessibility and widespread smartphone adoption, is expected to sustain favorable consumer spending levels. However, Fitch Ratings anticipates U.S. consumer spending growth of 2.6% in 2025, slightly down from 2.8% in 2024, with new tariffs posing potential risks that could fuel inflation. While strong household balance sheets and a resilient labor market may continue to provide some respite to consumer spending, inflationary pressures could pose a challenge by potentially constraining consumers' purchasing power.

Expansion in Cross-Border Transactions: Financial transaction service providers are well-positioned to benefit from the rise in international trade, increased global travel and a growing demand for efficient remittance solutions. Companies offering advanced cross-border payment platforms are particularly attractive as they enable seamless international transactions and efficient currency exchange management. These solutions play a crucial role in helping businesses receive payments from global customers and make timely payments to suppliers, ensuring smooth operations. Additionally, the expanding global workforce continues to drive demand for reliable cross-border remittance services.

Strategic Growth via Mergers and Acquisitions: To establish comprehensive digital ecosystems, companies in the financial transaction services sector frequently pursue M&As alongside investments in technology. These strategies are vital for enhancing service capabilities, diversifying operations, expanding customer bases and strengtheningglobal marketpresence. In 2024, the Fed cut the interest rate three times. The Fed also hinted at probable two or three more cuts in 2025. Lower interest rates are expected to encourage companies to secure loans for M&A activities, allowing them to preserve cash reserves while fostering expansion.

Zacks Industry Rank Indicates Bearish Outlook

The group’s Zacks Industry Rank, which is the average of the Zacks Rank of all member stocks, indicates tepid near-term prospects. The Zacks Financial Transaction Services industry is housed within the broader Zacks Business Services sector. It currently carries a Zacks Industry Rank #133, which places it in the bottom 46% of 248 Zacks industries.

Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than two to one. The industry’s positioning in the bottom 50% of the Zacks-ranked industries is a result of the negative earnings outlook for the constituent companies in aggregate.

Despite the dismal scenario, we will present a few stocks that one can retain, given their solid growth endeavors. But before that, it is worth looking at the industry’s recent stock-market performance and the valuation picture.

Industry Outperforms Sector and S&P 500

The Zacks Financial Transaction Services industry outperformed its sector and the Zacks S&P 500 composite in the past year.

In the said time frame, the industry has grown 15.5% compared with the Business Services sector’s gain of 9.7%. The S&P 500 has rallied 9.5% in the same time frame.

One-Year Price Performance

Image Source: Zacks Investment Research

Industry's Current Valuation

On the basis of the forward 12-month Price/Earnings ratio, commonly used for valuing financial transaction services stocks, the industry is currently trading at 23.28X compared with the S&P 500’s 20.63X and the sector’s 24.39X.

In the past five years, the industry traded as high as 36.25X, as low as 18.51X and at the median of 23.44X.

Forward 12-Month Price/Earnings (P/E) Ratio

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

5 Stocks to Keep a Close Eye on

We are presenting five stocks from the Financial Transaction Services industry that currently carry a Zacks Rank #3 (Hold). Considering the current industry scenario, it might be prudent for investors to retain these stocks in their portfolio as these are well-placed to generate growth in the long haul.

Visa: Headquartered in San Francisco, the company is a global frontrunner in digital payments, continuously expanding its network through new agreements, renewed partnerships, and strategic acquisitions. Strong operations across Latin America, Canada and the United States fuel growth for V. Steady consumer spending drives higher transaction processing fees, boosting Visa’s revenues. The company prioritizes technology investments to enhance its cutting-edge digital solutions.

The Zacks Consensus Estimate for Visa’s fiscal 2025 earnings is pegged at $11.30 per share, indicating an 12.4% rise from the year-ago figure. V’s earnings beat estimates in each of the last four quarters, the average surprise being 3.03%.

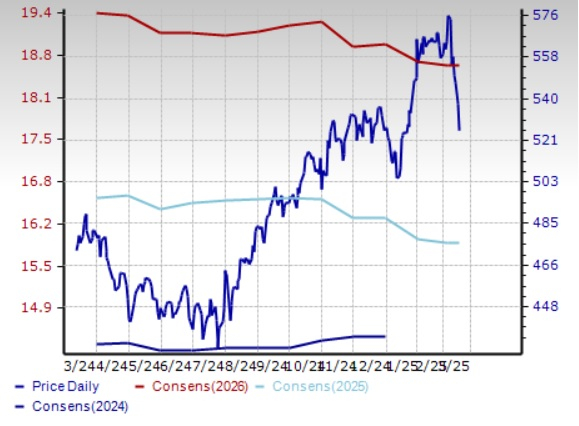

Price and Consensus: V

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Mastercard’s 2025 earnings is pegged at $15.91 per share, indicating an 9% rise from the year-ago figure. MA’s earnings beat estimates in each of the last four quarters, the average surprise being 3.29%.

Price and Consensus: MA

Image Source: Zacks Investment Research

Fiserv: The Wisconsin-based company offers a diverse suite of solutions, including payment processing, core banking platforms and digital banking services. Its business model leverages recurring revenue streams and high incremental margins from scaled processing operations. The company prioritizes excellence by acquiring new clients and deepening existing relationships.

The Zacks Consensus Estimate for Fiserv’s 2025 earnings is pegged at $10.23 per share, indicating a 16.3% rise from the year-ago figure. FI’s earnings beat estimates in each of the last four quarters, the average surprise being 2.89%.

Price and Consensus: FI

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Fidelity National’s 2025 earnings is pegged at $5.74 per share, indicating an improvement of 10% from the year-ago figure. FIS’ earnings beat estimates in each of the last four quarters, the average surprise being 9.35%.

Price and Consensus: FIS

Image Source: Zacks Investment Research

Western Union: Colorado-based Western Union, historically a brick-and-mortar money transfer provider, has built a robust digital presence. Through substantial investments and strategic digital partnerships, the company has achieved significant digital revenue growth. Western Union also collaborates with leading global and regional financial service providers in a bid to enhance capabilities.

The Zacks Consensus Estimate for Western Union’s 2025 earnings is pegged at $1.79 per share, indicating an improvement of 2.9% from the year-ago figure. WU’s earnings beat estimates in two of the last four quarters, matched the mark once and missed the same in the remaining one occassion, the average surprise being 3.07%.

Price and Consensus: WU

Image Source: Zacks Investment Research

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2024. While not all picks can be winners, previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Visa Inc. (V) : Free Stock Analysis Report

Mastercard Incorporated (MA) : Free Stock Analysis Report

Fidelity National Information Services, Inc. (FIS) : Free Stock Analysis Report

The Western Union Company (WU) : Free Stock Analysis Report

Fiserv, Inc. (FI) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.