Key Points

Production hiccups and a widening Q1 net loss forced Lucid to suspend production guidance.

Saudi Arabia's PIF is a majority investor of Lucid and showed recently that funding won't be limitless.

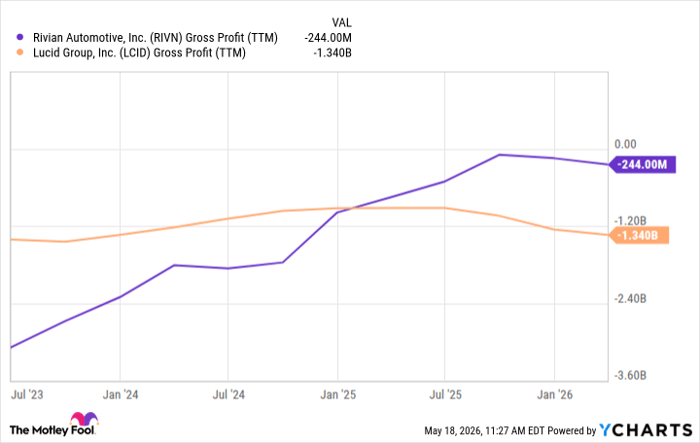

Rival EV maker Rivian has made much more impressive progress on gross profitability than Lucid.

- 10 stocks we like better than Lucid Group ›

Most investors understand it's probably an impossible task to find the next Tesla currently. But the allure of looking for such an investment remains, and it's one reason many look to Lucid Group (NASDAQ: LCID), considering it's widely recognized for making some of the most advanced electric vehicles (EVs) on the planet.

That said, every time the company appears to be turning a corner, something comes up. Before you even consider investing in Lucid, it's important to consider these three factors.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Production hiccups

Lucid's early history was marred by multiple supplier and production issues, making progress far bumpier than investors would have liked. Just as investors hoped Lucid had grown past that -- and in the automotive industry, you never entirely grow out of these hiccups – another issue reared its ugly head.

The EV maker recently launched Gravity SUV has been slower to accelerate production than hoped. Making matters worse, Gravity deliveries were significantly impacted in February due to a rear-seat defect that triggered a recall. Between the hiccup in Gravity production, the recall, and the ensuing temporary halt in Gravity sales, as well as a widening first-quarter net loss, the company opted to suspend its full-year production guidance and will provide an update at the end of the second quarter.

Image source: Lucid.

Lucid is a young automaker working through the process, and that's going to come with speed bumps, likely more than investors would like. It's just one thing to consider.

Funding red flag?

You might think that Lucid and LIV Golf have nothing in common, but that would be wildly inaccurate thanks to a certain investor. Saudi Arabia's Public Investment Fund (PIF) was instrumental in starting up LIV Golf, and it was intriguing to see how it all played out, with many thinking the PIF money could be essentially endless.

Then something a little funny happened: PIF decided it was time to stop throwing money at the start-up golf entity. The PIF began major financial backing of LIV Golf when it launched in 2021, and over the years, the wealthy fund has invested over $5 billion in the circuit, only to announce last month that it would stop funding LIV Golf at the conclusion of the 2026 season.

PIF was fairly quick to pull the plug on funding LIV Golf, but investors considering Lucid should understand the same entity has poured roughly $9.5 billion into the Lucid group over a slightly longer timeline, starting back in 2018. Investors could argue that the PIF's ties with Lucid are deeper as the Saudi fund is attempting to establish an independent automotive sector in Saudi Arabia and hopes Lucid's focus on the future of EVs, smart mobility, sustainable energy, and willingness to operate in the country will make it a cornerstone of that future.

That said, we now have our latest proof that the PIF funding isn't essentially endless, and that it can and will pull the plug. That's something investors have to consider because losing that investor would be devastating for Lucid.

Path to profits

Rivian Automotive (NASDAQ: RIVN) is a natural competitor to Lucid as both are young automakers focused purely on EVs. While Lucid has fewer deliveries and less scale, Rivian's progress on gross profitability has been impressive. Rivian reported its first-ever quarterly gross profit in the fourth quarter of 2024, partly driven by a significant reduction in costs per vehicle once the second-generation R1 vehicles hit the road.

Rivian followed that up with continued cost-cutting, then took a quick step forward by leveraging its surging software and services revenue from its Volkswagen joint venture to achieve its first full-year gross profit in 2025. While both are still burning through cash and reporting net losses, the difference in trajectories is clear in the following graph.

RIVN Gross Profit (TTM) data by YCharts

What it all means

Lucid remains an intriguing and unique investment opportunity, but these three simple factors to consider highlight just how complex and risky it is. The young EV maker continues to face production issues that hinder its results, has looming funding questions and concerns, and hasn't made nearly as much gross profit progress as Rivian, which shows investors it has a path to profits.

For the vast majority of investors, it's not time, perhaps not even close to time, to entertain Lucid as an investment.

Should you buy stock in Lucid Group right now?

Before you buy stock in Lucid Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Lucid Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $481,750!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,352,457!*

Now, it’s worth noting Stock Advisor’s total average return is 990% — a market-crushing outperformance compared to 206% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of May 20, 2026.

Daniel Miller has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Tesla. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.