It's no secret that cybercriminals are constantly looking to exploit companies' weaknesses. Breaches and ransomware come at tremendous costs. Some direct costs include data restoration, downtime, ransom payments, and security. Others are tougher to measure, like reputation hits and loss of customer confidence.

Companies spend billions protecting systems and endpoints, so CrowdStrike (NASDAQ: CRWD) believes it will have an addressable market of over $100 billion in the next few years.

But what good is an addressable market if a company isn't prepared to take advantage of it? Let's take a look at three pillars of CrowdStrike's strategy.

1. Accumulate customers

The first thing CrowdStrike must do, and is doing, is accumulate customers. Customers have lots of choices regarding cloud security or endpoint protection, and it's an arms race between CrowdStrike, established players like Palo Alto Networks (NASDAQ: PANW), and challengers like SentinelOne (NYSE: S). CrowdStrike is delivering incredible results. Since 2018 it has grown its subscription customer base 12-fold to reach 16,325 at the end of fiscal 2022.

Data source: CrowdStrike. Chart by author.

This trend continued in the first quarter of fiscal 2023 as the subscription customer base reached 17,945. Savvy investors know this is a make-or-break area.

2. Increase adoption

The company is successfully boosting revenue from these customers. CrowdStrike's Falcon platform is modular so that customers can tailor solutions to their needs. CrowdStrike's sales multiply by encouraging customers to stay, adopt more modules, and increase the amount they spend each year.

At the end of the last quarter, more than 70% of CrowdStrike's customers were using at least four modules, and nearly 20% was using seven or more modules.

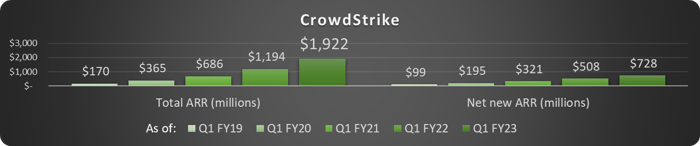

CrowdStrike has posted dollar-based net retention (DBNR) rates above 120% every quarter since 2019. A DBNR above 100% indicates that customers are spending more each period. 120% is quite impressive. The proof is in the pudding, as annual recurring revenue (ARR) has risen at dazzling rates. ARR reached $1.9 billion in Q1 of fiscal 2023, with $728 million added since Q1 of fiscal 2022.

Data source: CrowdStrike. Chart by author.

This trend also speaks highly of the Falcon platform. Customers must be pleased, given CrowdStrike's 98% customer retention rate.

3. Scale to profits

The last step will be turning growth into profits; astute investors know this may take years. Sales and marketing (S&M) is enormously expensive at this stage. CrowdStrike spent $617 million in this department in fiscal 2022. This is money well spent while CrowdStrike is growing and monetizing customers. In fact, shareholders know it is critical to spend money on both S&M and research and development at this stage -- even if it means forgoing profits for now.

There are clues that the company can become profitable in the future. The subscription gross margin is over 75%, and the company generates positive free cash flow, often a precursor to profitability.

CrowdStrike appears to be making all the right moves in achieving phenomenal growth. Growth stocks have rallied a bit recently after dropping for much of 2022. Still, better opportunities to accumulate CrowdStrike stock may be yet to come, given the current topsy-turvy market.

10 stocks we like better than CrowdStrike Holdings, Inc.

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and CrowdStrike Holdings, Inc. wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of June 2, 2022

Bradley Guichard has positions in CrowdStrike Holdings, Inc. and Palo Alto Networks. The Motley Fool has positions in and recommends CrowdStrike Holdings, Inc. and Palo Alto Networks. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.