In 2021, Costco Wholesale (NASDAQ: COST) grew revenue and earnings by 17.5% and 25.1% year over year, respectively, showing no signs of a slowdown any time soon. The company's consistent growth, strong balance sheet, and unique competitive advantages have awarded Costco a premium valuation from investors over the years. But in Costco's case, a lofty valuation should not impede investors from buying shares of its stock.

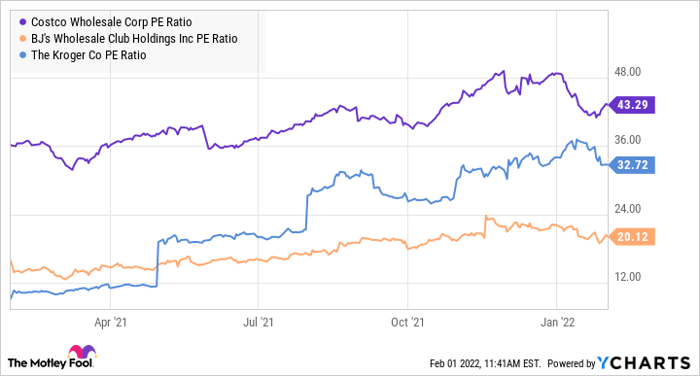

Costco currently trades at 43.3 times earnings, placing the company's valuation much higher than its industry peers. With close competitors like BJ's Wholesale Club (NYSE: BJ) and Kroger (NYSE: KR) trading at 20.1 times earnings and 32.7 times earnings, investors may be wary of Costco's high valuation. I believe, however, that Costco has earned its high-end appraisal and will continue to reward its long-term investors. Here are three reasons why.

COST PE Ratio data by YCharts

1. Costco's membership model ensures consistency

Costco has 62.5 million household members and a nearly 92% renewal rate. The company grew membership fees by 9.5% in 2021, which represented $3.9 billion in revenue. That doesn't seem like a lot when observing the company's $196 billion in annual sales, but there is one caveat investors should consider.

While only accounting for 2% of total revenue, membership fees represent about 77% of net income. Costco's membership model, as a result, is an essential component of its business and its ability to consistently increase profits. This is typically the case for subscription-based companies. The recurring billing associated with membership programs provides investors with cash-flow consistency and sales predictability. Given Costco's ability to retain customers year after year, the company isn't constantly forced to attract foot traffic into its warehouses. Most retail brands invest a lot of money into sales and marketing, but Costco doesn't have to in large part due to its membership model. The company does virtually no marketing, which is why you have probably never seen a Costco commercial or advertisement. This saves Costco money and ultimately leads to a more robust bottom line.

2. Kirkland Signature is an incredible success

Many Costco shoppers are familiar with the company's renowned private label, Kirkland Signature. What they might not know is that the brand makes up 30% of Costco's top-line. Kirkland sales triumphed $59 billion in 2021, translating to year-over-year growth of 13.5%. According to CNN Business, Kirkland products are sold for at least 20% less than other national brands in Costco's warehouses. A successful private label gives Costco more control over its operations. Because the company's signature brand accounts for a substantial amount of sales, Costco relies on less suppliers and requires lower inventory levels than other retailers.

The company can also better manage what products it sells in its warehouses, which grants Costco the flexibility to hand-pick items it believes will be the most profitable. Above all, as a massive revenue source for the company, Kirkland provides Costco with significant pricing leverage relative to its competition. This leads us to our final competitive advantage.

Image source: Getty Images.

3. Costco has the ability to sell items in bulk at very low prices

Costco is notorious for offering its customers bulk items at unbeatable prices. As mentioned above, Kirkland Signature is the primary force driving the company's pricing strategy. Because the company's signature brand accounts for a substantial amount of sales, Costco relies on fewer suppliers and requires lower inventory levels than other retailers. The company carries 4,000 stock keeping units (SKUs) per warehouse compared to 30,000 for most supermarkets. Likewise, the average Walmart and Target locations offer their customers 120,000 and 80,000, respectively. Less inventory translates to lower prices for its customers. It is part of Costco's mission to "carefully [choose] products based on quality, price, brand, and features" in order to offer superior value. Lower inventory levels lead to increased buying power for Costco because a lot of suppliers are competing for a limited amount of shelf space. Buying power creates pricing leverage for Costco, which in return enables the company to sell items at cheaper levels than other retailers.

The ability to offer such low prices helps facilitate the company's strong membership retention rate. Customers will keep coming back because they can't find better deals anywhere else. Strong membership retention leads to predictable cash flows and income, prompting investors to better understand the direction of Costco's business. Foreseeability in financial performance is extremely advantageous for investors because there is less ambiguity involved when analyzing the company.

Costco is worth paying up for

Costco shares certainly don't classify as cheap, but sometimes, we have to shell out today for great companies that will pay us back tomorrow. Costco's high-flying valuation won't stop it from reaching new milestones. Especially in today's market, where many investors are dumping speculative growth stocks and buying more mature companies, Costco is poised to generate strong shareholder returns. The company's competitive advantages, such as its membership model, private label, and low pricing strategy, have led to a stable economic moat that investors can rely on regardless of market conditions.

10 stocks we like better than Costco Wholesale

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now… and Costco Wholesale wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of January 10, 2022

Luke Meindl owns shares of Costco Wholesale. The Motley Fool owns and recommends Costco Wholesale. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.