A high dividend yield is often (but not always) a sign of a higher risk profile. The higher dividend is an investor's reward for taking on more risk. However, the risk is that the payout might hit the chopping block if the company's financial profile deteriorates.

Risk-tolerant investors have several alluring options these days, given all the uncertainty in the economy and broader market. Three high-yielding dividends stocks with big upside potential are Devon Energy (NYSE: DVN), Medical Properties Trust (NYSE: MPW), and Pioneer Natural Resources (NYSE: PXD).

A potentially high-octane payout

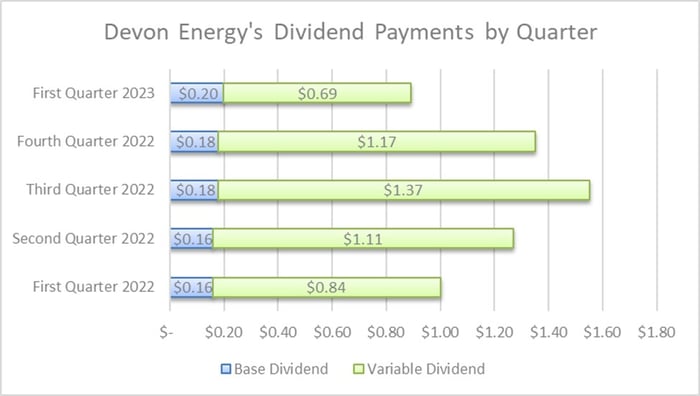

Devon Energy's dividend has two components. The oil and gas producer pays a fixed based dividend that it can sustain at lower energy prices. In addition, it pays up to half its post-base-dividend free cash flow each quarter via a variable dividend. Given that framework, Devon's dividend payment can vary significantly from quarter to quarter based on its volatile oil-fueled cash flows:

Data source: Devon Energy. Chart by author.

As that chart showcases, the company has steadily increased its base dividend payment. However, the variable dividend has differed each quarter. That makes it a bit trickier to determine Devon's dividend yield. If we use the most recent payment ($0.89 per share or $3.56 per share annualized), Devon has a 7.1% yield at its current stock price of $50. However, if we add up its last four payments ($5.06 per share), it has a more than 10% dividend yield.

The problem with that math is it's backward-looking. Oil prices are currently in the mid-$70s and below Devon's 2023 outlook for $80 oil. At that price point, the company would probably pay only a 4% yielding dividend this year, given its higher capital planned capital expenditures. However, several catalysts could push crude prices back up toward the triple digits by this summer. Devon's free cash flow will surge if that happens, probably driving up its dividend payment and stock price.

Plagued by a sickly tenant

Medical Properties Trust currently yields around 13.5%. Driving that sky-high yields are concerns that the healthcare REIT might need to reduce its dividend because of higher interest rates and tenant issues. The company warned that one of its largest tenants, Prospect Medical Holdings, might not pay rent on its Pennsylvania hospitals this year.

Given that outlook, Medical Properties Trust would generate only about $1.29 per share of adjusted funds from operations (FFO) this year, according to a worst-case scenario estimate by CFO Steve Hamner on the company's fourth-quarter conference call. With the current dividend payment at $0.29 per share ($1.16 per share annualized), it would put its dividend payout ratio at 90%. That doesn't leave much room for error.

However, the company expects to eventually recover all the rent owed by Prospect, though that could take 12 to 18 months. Furthermore, it expects to sell those hospitals at full value and redeploy the proceeds into better opportunities. If everything goes according to plan, the company could maintain its dividend and add healthier tenants to its portfolio, which could lift a significant weight off its stock price.

Another high-octane, high-upside dividend payment

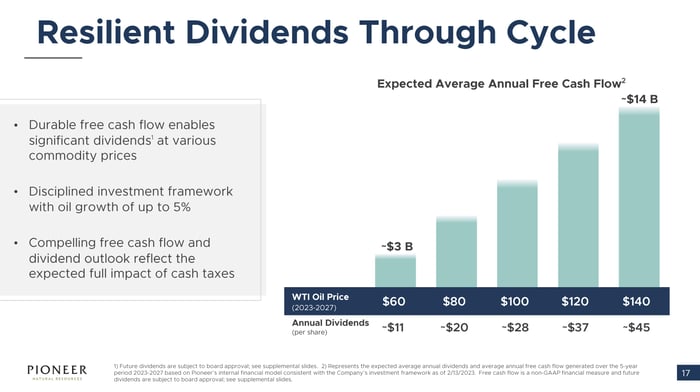

Pioneer Natural Resources shares a lot in common with Devon Energy. The oil and gas producer also has a fixed-plus-variable dividend framework. However, it has a higher payout ratio of 75% of its post-base-dividend free cash flow for the variable payment. It therefore has an even higher dividend yield.

The company has forecast its potential annual dividend payments based on various oil price points:

Image source: Pioneer Natural Resources investor relations presentation.

With shares recently below $200, Pioneer's dividend yield would be above 10% at $80 oil. Meanwhile, it would be more than 14% if crude rebounds toward $100 a barrel, which CEO Scott Sheffield expects to see later this summer. That would probably drive shares higher, especially given their relatively low valuation these days.

High-risk, high-reward opportunities

Devon Energy, Medical Properties Trust, and Pioneer Natural Resources offer big-time dividend yields. That's part of the reward investors can earn if everything goes as planned. In addition to those big payouts, investors could see significant stock price appreciation if the catalysts play out as expected.

However, there's also a high risk that those big-time payouts could fall. Devon and Pioneer have already reduced their dividends from peak levels because of the impact of higher oil prices on their cash flows. Investors need to weigh the risk with the reward to determine if these big-time dividend stocks are worth it in their particular situation.

10 stocks we like better than Devon Energy

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Devon Energy wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of March 8, 2023

Matthew DiLallo has positions in Medical Properties Trust and has the following options: short April 2023 $9 puts on Medical Properties Trust. The Motley Fool recommends Pioneer Natural Resources. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.