As experienced market watchers and rookies alike prepare for a recession, growth stocks -- particularly the high-flying tech names of the COVID era -- aren’t many people’s favorite picks.

And there’s good reason for this. After all, inflation looks far from tamed and that was the reason for the Fed raising rates in the first place. Now, they’ve got nowhere to go but keep raising further. And that basically means everything is going to get more expensive and turn away a few consumers, or that companies will stop passing their increasing costs onto consumers in the hope that demand (or pricing) won’t shrink too much. It may be a bit of both.

The situation is actually pretty tricky because companies could cut production in order to maintain pricing, which wouldn't help bring down inflation, thus delaying the result of the Fed’s actions. Or they could cut production and still see shrinking demand, which if it continues for too long will land us in the recession that everybody's talking about.

Which brings us back to the topic of big technology stocks that have been outgrowing many smaller players over the past decade. COVID has also been great for them, as companies sped up their digitizing programs and consumers hastened to operate remotely. The crisis even had people throwing caution (and data) to the wind that were lapped up by many of these big tech companies.

With all that under the belt now, Big Tech stocks are gearing up for the next growth phase. They have huge war chests to wait out the worst of recessions, and can weather storms better than most.

There’s certainly a lot of pessimism around tech stocks now because of the risk of investing in growth names. And then there are individual factors, like for example Alphabet GOOGL, Meta Platforms META or Twitter TWTR, which depend on ad revenue. Because as everyone knows, people aren’t going to be buying and selling a lot of ads in a recession.

Or as in Microsoft’s MSFT case, enterprise sales (at least the transactions-based) may cool down. Advanced Micro Devices AMD could be slower to feel an impact since there is pent-up demand for the hardware that it sells.

Three of these companies are reporting after the bell today, which makes this a good time to check out what analysts are looking for in them-

Microsoft

In Microsoft’s case, analysts are expecting sequential and year-over-year growth in all its three segments: Productivity, Intelligent Cloud and Personal Computing.

The Productivity business is expected to grow 5.8% sequentially and 13.7% year over year.

Intelligent Cloud revenue is expected to grow 10.9% sequentially and 21.6% year over year.

The More Personal Computing segment is expected to see the slowest growth, increasing 1.3% sequentially and 4.5% year over year.

Microsoft has not missed analysts’ segment revenue targets in the preceding five quarters. However, it’s worth noting that Windows revenue has disappointed in the last two quarters (low single-digit range) while Office products and cloud services disappointed in the last quarter (by less than a percentage point). These could be areas to watch this quarter as well, especially as a sign of softening demand.

Another point to note is the expected sequential decline in Productivity profits.

Alphabet

Around 80% of Alphabet’s revenue in the March quarter came from advertising. So that is obviously the most important segment we should be focusing on. These ad revenues come from both Google properties (including search and YouTube) and network properties (bout 15% of total ad revenue in the last-concluded quarter).

Analysts are looking for 3.2% sequential and 12.0% year over year growth on Google properties in the June quarter. Of this, Google minus YouTube is expected to account for 85%, growing 3.0% sequentially and 13.9% year over year. YouTube is expected to grow a respective 7.8% and 5.7%.

Revenue from network properties is expected to grow 3.8% sequentially and 11.7% year over year.

Total ad revenues are expected to grow 3.3% sequentially and 11.9% from last year.

Other than YouTube, which analysts appear to be overly optimistic about, the company has been fairly consistent at beating analyst estimates.

Google Other, which includes things like Play and hardware, may have disappointed in the last quarter because of the cooldown in computing. This quarter, analysts are looking for 4.8% sequential and 7.8% year over year growth.

Google Cloud is expected to grow 10.2% sequentially and 38.6% year over year.

Other Bets is expected to see a 21% sequential decline, while still growing around 81% from last year.

Analysts expect a sequential decline in revenue from the EMEA region, which had disappointed in the March quarter. However, the US and APAC, which had also disappointed, are expected to grow this quarter.

Advanced Micro Devices

AMD has a solid history of beating analyst estimates, especially in its Computing and Graphics segment. In the last five quarters, this segment has posted an average surprise of 6.4%.

The Enterprise Embedded and Semi-Custom segment has also topped analyst estimates in each of the last five quarters, averaging 7.1%.

In the to-be-reported quarter, Computing and Graphics is expected to see a sequential decline of 4.0% although this will represent year-on-year growth of 19.6%.

Enterprise Embedded and Semi-Custom is expected to grow 9.7% sequentially and 73.1% year on year.

Conclusion

While technology stocks may be out of favor on account of their being tied to uncertain future growth, these Big Tech stocks are still delivering. What’s more, even at these subdued growth rates, they’re doing better than many others in the space. That said, you may want to wait until valuation comes down further, as seems likely in the event of a recession.

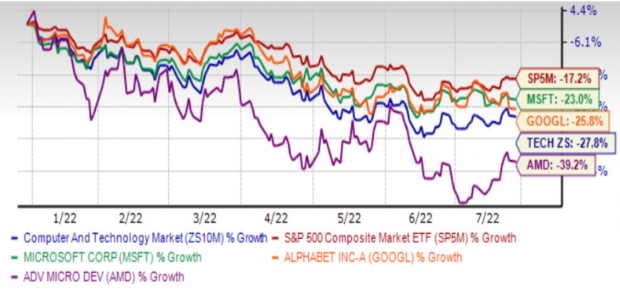

Year-to-Date Price Performance

Image Source: Zacks Investment Research

This Little-Known Semiconductor Stock Could Lead to Big Gains for Your Portfolio

The significance of semiconductors can't be overstated. Your smartphone couldn't function without it. Your personal computer would crash in minutes. Digital cameras, washing machines, refrigerators, ovens. You wouldn't be able to use any of them without semiconductors.

Disruptions in the supply chain have given semiconductors tremendous pricing power. That's why they present such a tremendous opportunity for investors.

And today, in a new free report, Zacks' leading stock strategist is revealing the one semiconductor stock that stands to gain the most. It's yours free and with no obligation.

>>Give me access to my free special report.Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Advanced Micro Devices, Inc. (AMD): Free Stock Analysis Report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Twitter, Inc. (TWTR): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

Meta Platforms, Inc. (META): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.