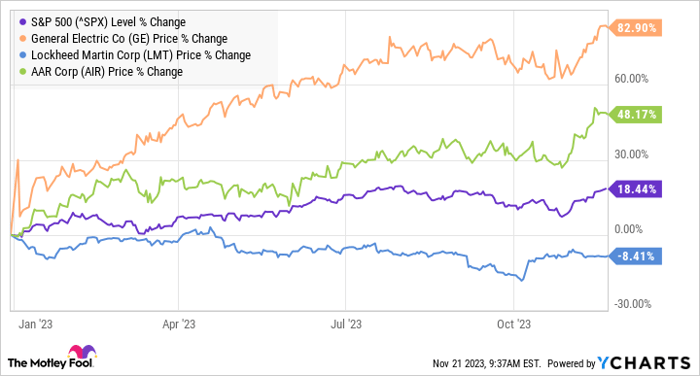

Lockheed Martin (NYSE: LMT) is down nearly 9% this year, while the stocks of other companies with aerospace and defense exposure, like General Electric (NYSE: GE) and AAR Corp (NYSE: AIR), have not only significantly outperformed Lockheed's stock but also trounced the S&P 500 index. Here's a look at the how and why.

Execution matters

The difference in stock performance comes down to exceeded expectations, favorable valuations at the start of the year, and excellent execution through 2023. The third of these factors is the one management has the strongest control over, and that has distinguished the two industrial companies from Lockheed Martin. Simply put, they have done the boring job of executing well this year.

In contrast, Lockheed Martin has had issues with its single-most important program, the F-35 multirole stealth fighter plane.

The F-35 represented 27% of total sales in 2022 and 66% of its aeronautics sales. Unfortunately, the company is falling behind its delivery targets.

At the beginning of the year, management was planning to deliver at least 147 F-35s this year, only to reduce the target to 100-120 in July and now to just 97. The company has suffered delays to a hardware and software upgrade known as Technology Refresh 3, or TR-3. Moreover, until the TR-3 is validated in 2024, the threat of more delivery delays will hang over the company.

General Electric

In contrast, GE has executed excellently in 2023. Its aerospace segment (commercial engines, aftermarket, and defense) has raised its earnings guidance through 2023, buoyed by an ongoing recovery in commercial flight departures and airplane production rates.

Meanwhile, GE Power, once the company's problem child, is now a solid earnings and cash-flow generator -- an achievement marked by working through less favorable legacy contracts and displaying pricing discipline on new contracts. That's a gameplan management is repeating at GE Renewable Energy, where onshore wind and grid solutions are profitable again.

Image source: Getty Images.

GE still has issues at offshore wind (set to lose $1 billion in 2023 and 2024), but this is a relatively new business for GE, and wind turbine manufacturers are looking to raise prices across the industry. Overall, GE started the year forecasting high-single-digit revenue growth and $3.4 billion to $4.2 billion in free cash flow (FCF) and now expects low-teens revenue growth and $4.7 billion to $5.1 billion in FCF.

AAR Corp

Lockheed Martin and GE are industrial giants with $100 billion-plus market caps, but the following stock is a tiddler in comparison. AAR Corp only has a $2.36 billion market cap, but it's well known in the aviation industry for its aviation services to commercial airlines and the military.

Its main business is parts supply (41% of revenue), a segment that grows in line with flight departures and is its highest-margin business, with a segment profit margin of close to 12%. Similarly, its repair and engineering segment (airframe maintenance, repair, overhaul, and engineering) also benefits from increased flight departures and generates about 27% of revenue. The third major segment, integrated solutions (support programs, logistics, and component support), generates around 27% of revenue and has a segment profit margin of 6%-plus.

The interesting thing about AAR's business is that its three primary segments are complementary. Its repair and engineering business means demand for parts, which its parts supply business can help service. Moreover, its integrated solutions business helps to ensure commercial and military fleet readiness.

Image source: Getty Images.

It's not a revolutionary business, but it is essential for the industry's growth. And AAR has built customer relationships with a who's who of the industry -- from premium-focused carriers like Delta Air Lines and budget airlines like Southwest to cargo airlines run by FedEx and UPS.

The recent first quarter of 2024 results saw the company growing sales by 23% year over year, and AAR continues to benefit from favorable end-market conditions. Meanwhile, management is building on the new distribution agreements signed through 2023 (including with an RTX business, Moog, and MTU) while signing agreements to service airlines like United Airlines and Pegasus.

General Electric and AAR Corp

The outperformances of GE and AAR are primarily driven by taking advantage of favorable market conditions and executing accordingly. In contrast, Lockheed-Martin has missed delivery targets on its key program. The difference comes down to the kind of boring blocking and tackling that wins football games and generates value for investors. If both companies keep doing the same in 2024, investors can also get positive returns from the stocks next year.

10 stocks we like better than Lockheed Martin

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Lockheed Martin wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of November 20, 2023

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends FedEx. The Motley Fool recommends Delta Air Lines, Lockheed Martin, RTX, Southwest Airlines, and United Parcel Service. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.