Kraft Heinz (NASDAQ: KHC) came about in large part at the behest of Warren Buffett's Berkshire Hathaway. With a gain for Berkshire of more than 2,470,000% from 1964-2019, few question Buffett's investment genius.

However, neither its status as a recession-proof consumer staples stock nor Buffett's business acumen have stopped Kraft Heinz from declining. Amid falling profits and a deteriorating business model, investors should consider avoiding this stock.

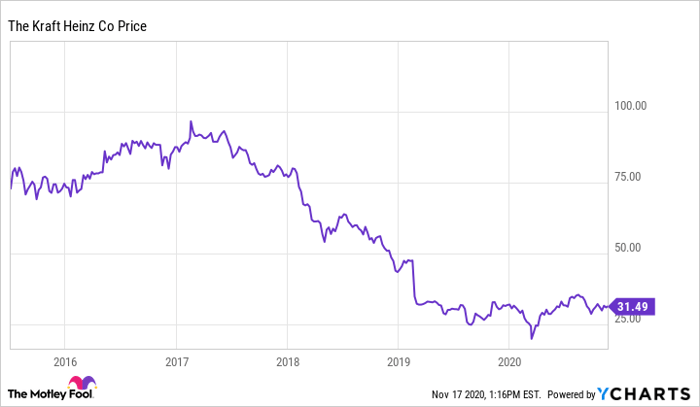

Kraft Heinz looks like a value stock

In many respects, Kraft Heinz does not look like a stock that investors should shun. For one, the COVID-19 pandemic led to a run on consumer products in the spring. Now, with cases surging to record highs, it could again spark another run on consumer staples.

Secondly, Kraft Heinz looks like a stereotypical Buffett stock in many respects. The stock sells for about 13 times forward earnings. Moreover, its annual dividend of $1.60 gives new investors a cash return of just over 5%.

Still, the stock faces significant issues

However, even Buffett is not immune to investment missteps. Kraft Heinz appears on track to become one of his most notable mistakes. Since the Kraft Heinz merger in 2015, shares have lost more than half their value.

In recent years, consumers have shown a preference for natural foods, causing a sales decline within the packaged food industry. This has hurt not only Kraft Heinz but also peers such as General Mills and Campbell Soup.

However, a strategic shift made by CEO Miguel Patricio may have offered Kraft Heinz a reprieve. Patricio streamlined the company from 55 categories to six platforms. He also began to view these platforms holistically, seeking to improve overall experiences rather than boosting individual products.

Company financials hint at further dangers

In the latest quarter, net sales rose by 6%. Still, forecasts indicate Patricio's changes may not offer enough help.

Despite the sales surge during the pandemic, analysts forecast a 2% drop in earnings this year. They also believe profits will fall by an additional 10% in fiscal 2021. The 2021 number likely reflects the return of pre-pandemic buying patterns, which indicates the latest increase in sales is likely temporary.

Image source: Getty Images.

Also, this decline could further endanger the dividend. The free cash flow for the first nine months of the year came in at $2.9 billion. This should cover the dividend expense of just under $1.5 billion during the same period.

Nonetheless, strategic shifts usually come at a cost. Slashing the payout could help fund such changes.

Moreover, investors must remember that Kraft Heinz does not have a track record of raising dividends. Hence, the company could easily reduce the payout again, much as it did in 2019.

How should Buffett and other investors respond?

Buffett continues to hold his Kraft Heinz stake, which amounts to more than 325 million shares. He had owned Heinz before the merger. In a partnership with 3G Capital, he purchased Kraft for $23 billion in 2013 and later merged it with Heinz.

Buffett admitted in a 2019 interview with CNBC he had paid too much for Kraft. At that time, he also revealed a $3 billion non-cash loss from a writedown of intangible assets.

Still, he has resisted selling this stock, likely due to the size of his investment. Currently, his stake amounts to about 27% of the company. This means that if Buffett wanted to sell, he would have to find a buyer for more than 325 million shares at the current price.

Fortunately, most stockholders do not have to contend with that problem, and investors may want to consider selling. Packaged products will probably not go away completely, and perhaps Patricio's strategic shift will improve the company's overall performance. However, until Kraft Heinz can reverse its earnings declines, the stock's downhill slide could easily resume.

10 stocks we like better than Kraft Heinz

When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the ten best stocks for investors to buy right now... and Kraft Heinz wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of October 20, 2020

Will Healy owns shares of Berkshire Hathaway (B shares). The Motley Fool owns shares of and recommends Berkshire Hathaway (B shares) and recommends the following options: long January 2021 $200 calls on Berkshire Hathaway (B shares), short January 2021 $200 puts on Berkshire Hathaway (B shares), and short December 2020 $210 calls on Berkshire Hathaway (B shares). The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.