Key Points

Visa processed over 66 billion payments worth over $3.8 trillion in its most recent fiscal quarter.

The financial powerhouse routinely has industry-leading margins, largely due to its scale.

Value-added services and stablecoins have been two fast-growing business segments for Visa.

- 10 stocks we like better than Visa ›

Nobody can predict how stocks will move in the market, but some companies are built for long-term success. And although business performance and stock price movements aren't always aligned, they tend to align over time.

And so, any time I invest in a stock, the plan is to hold it for the long haul. Of course, that doesn't always mean adding to my stake regularly.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

However, one stock I will consistently add to, no matter what's going on in the broader economy and market, is Visa (NYSE: V). It's a blue-chip stock that continues to get stronger with time. Here's why.

Image source: The Motley Fool.

Visa's scale is unmatched in its industry

Although Visa and Mastercard operate somewhat in a duopoly in the payment processing world, Visa's sheer scale is unmatched. In its fiscal second-quarter (ended March 31), it processed 66.1 billion payments, facilitated $3.87 trillion in volume, and was accepted by over 175 million merchants. For comparison, Mastercard processed around 43.8 billion ($2.7 tillion in dollar volume) in its most recent quarter.

Visa's main business model is simple: Take a percentage of every transaction that happens on its network. That's why volume is so important to its business. And since higher volume doesn't require higher costs once the payment infrastructure is put in place, Visa has the highest margins in the industry, and some of the highest you'll find anywhere.

In its most recent quarter, Visa's operating margin (profit after all operational costs) was 64.4%, and its net profit margin (profit after all expenses, interest, and taxes) was 53.6%. Mastercard's was 60.8% and 46.4%, respectively.

Going beyond just traditional payment processing

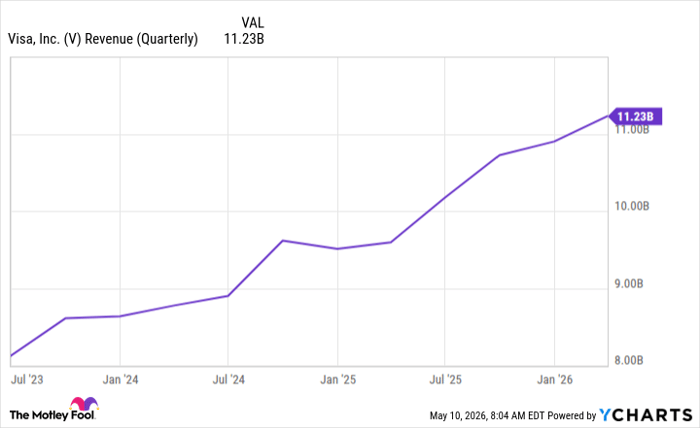

Processing payments will always be Visa's bread and butter, but its business has recently been expanding beyond that. Its value-added services (VAS) segment grew 27% year over year and accounted for 30% of its $11.2 billion in total revenue.

VAS includes services such as fraud detection, consulting, marketing, and data analytics. On the most recentearnings call Visa's CEO said VAS was a "bigger opportunity than ever" for the company. Visa has tons of data from its countless transactions to help financial institutions and companies with their operations.

It likely won't reach the level of payment processing, but it's a way for Visa to take advantage of its massive (and growing) scale.

V Revenue (Quarterly) data by YCharts

Visa has also embraced stablecoins, and it's trying to position itself as the main bridge between them and real-world practicality for people. Stablecoins are mostly used as digital piggy banks meant to maintain a stable value (usually by being tied to the U.S. dollar). However, they aren't useful on a large scale if the average person or business can't use them to purchase everyday items.

That's what Visa is trying to fix by acting as a middleman and issuing stablecoin-linked Visa cards that let people spend their stablecoins in their local grocery stores, gas stations, restaurants, or wherever Visa is accepted.

Regardless of how the technology plays out, it's encouraging to see Visa embrace emerging technology and other fintech developments. As the financial landscape changes with advancements in digital payments, its size alone won't be enough to maintain dominance. However, size and willingness to avoid complacency should keep Visa in a leadership position for quite some time.

Visa is priced well for a market giant

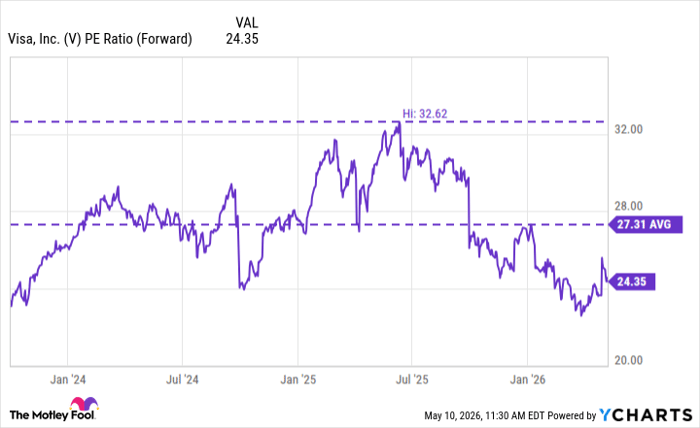

As of market open on May 11, Visa shares are trading at 24.4 times projected earnings per share over the next 12 months. That's lower than its average over the past few years and much cheaper than it was just a year ago.

V PE Ratio (Forward) data by YCharts

Visa's stock is almost never cheap, but after declining by over 10% in the past 12 months, it's much more fairly priced now. Considering how vital it is to the global payments infrastructure, it's a stock I'm holding onto for the long haul.

Should you buy stock in Visa right now?

Before you buy stock in Visa, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Visa wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $460,826!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,345,285!*

Now, it’s worth noting Stock Advisor’s total average return is 983% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of May 12, 2026.

Stefon Walters has positions in Visa. The Motley Fool has positions in and recommends Mastercard and Visa. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.