The stock market is on fire. The benchmark S&P 500 index has gained 33% during the past 12 months, reaching new highs almost daily.

That's nothing compared to the shares of Affirm Holdings (NASDAQ: AFRM). The stock of the buy now, pay later (BNPL) specialist have skyrocketed about 300% during that period. Its impressive run was fueled by robust consumer spending in a surprisingly strong economy and key partnerships with top e-commerce providers.

However, before jumping on the bandwagon, I'd hesitate to buy Affirm today. Here's why.

Buy now, pay later has exploded in popularity

Affirm simplifies buying and borrowing through its buy now, pay later offering. The company lets customers split purchases into manageable installments and is easy to use. Unlike credit cards with high interest rates and late fees, BNPL gives customers a convenient way to spread out payments without accumulating interest -- assuming they meet the repayment terms.

The BNPL company offers flexible payment solutions. One is its "pay-in-4" offering, a short-term, interest-free option that lets customers split purchases into four bi-weekly installments. It also offers core loans, which offer more flexibility through monthly installment loans, which include interest-bearing installment loans or 0% annual percentage rate (APR) loans.

Affirm makes money in two key ways. First, it earns a fee from merchants whenever a customer makes a purchase using its product and earns higher fees from merchants when customers use its no-interest-rate product. The company also earns interest on its interest-bearing loans, which can be a good source of income during periods of rising interest rates.

Given the ease of use and transparent repayment options, BNPL products have exploded in popularity over the years. According to Adobe Analytics, consumers spent $75 billion online through BNPL platforms last year, up 14% from 2022.

Consumers are racking up debt

Despite fears of an impending recession since early 2022, consumer spending has remained surprisingly strong. Fueled by rising credit card balances and BNPL options, people continue spending. According to the Federal Reserve Bank of New York, American consumers owe $1.13 trillion on their credit cards, representing a 31% rise during the past two years. This comes even though credit card interest rates average 22.77% -- the highest level in decades.

Image source: Getty Images.

The high-interest-rate environment can make Affirm's 0% financing options more attractive to cost-conscious consumers. Products like its popular pay-in-4 plan can be a compelling alternative for consumers in a pinch who need to spread out their payment over several weeks.

Affirm has also cultivated strategic partnerships with e-commerce giants, becoming the first buy now, pay later option through Amazon Pay. It has also enjoyed a long-standing partnership with Shopify, with its Shop Pay offering. Affirm's partners appreciate the payment options because they boost conversion rates.

Through the first six months of 2023, the company's revenue rose has by an impressive 43% to over $1 billion. However, it still reported a net loss of $303 million during that period, although that's an improvement from the prior year's $593 million deficit.

Keep an eye on this metric

Although Affirm's growth and partnerships are impressive, investors have reason to be cautious.

Economic pressures on consumers continue to mount, especially with high interest rates. During the Federal Reserve's March 20 meeting, the committee maintained its benchmark interest rate at 5.25%. Additionally, expectations for interest-rate cuts have gone from six earlier this year to just three. If inflationary pressures persist, interest-rate cuts could get pushed even further out.

Increased borrowing has spurred demand for Affirm's product. However, it also suggests consumers increasingly rely on financing to make purchases, which could be a sign of financial strain.

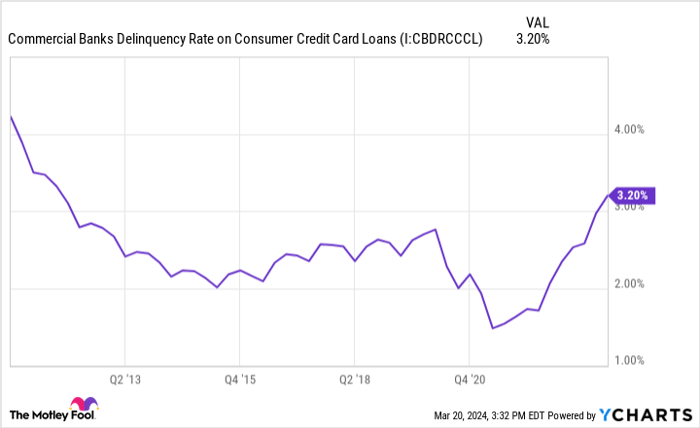

One key metric investors will want to monitor is Affirm's delinquency rates. Although its credit quality has been good, the company has seen its delinquencies tick up slightly to 2.4% during the past two quarters, even as Affirm tightens its lending standards. This trend isn't unique to Affirm, either. Credit card loan delinquencies have increased to 3.2%, suggesting some strain on consumers to repay their debts.

Commercial Banks Delinquency Rate on Consumer Credit Card Loans data by YCharts.

Caution is warranted

Affirm's growth intrigues me, but the company continues to lose money and faces uncertainty due to consumer health. During the past few years, the BNPL company has recorded net losses of more than $2 billion, and rising delinquencies could put further pressure on its bottom line.

Not only that, but it faces formidable competition. According to a consumer survey by LendingTree, PayPal is the most popular BNPL provider, with 55% of respondents saying they've used it. Klarna (33%) and Afterpay (owned by Block) (29%) are the next, followed by Affirm (28%).

Affirm confronts a challenging environment due to high interest rates, rising delinquencies, and rivals with more market share. Given the uncertainty and the company's mounting losses, I'd avoid buying Affirm stock today.

Should you invest $1,000 in Affirm right now?

Before you buy stock in Affirm, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Affirm wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 21, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Courtney Carlsen has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Adobe, Amazon, Block, PayPal, and Shopify. The Motley Fool recommends the following options: short March 2024 $67.50 calls on PayPal. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.