The proliferation of technology in everyday life led to increasing chip demand over the years, and the advent of artificial intelligence (AI) only increased this demand. The pandemic, meanwhile, fueled a major global chip shortage over the past few years.

While areas of the semiconductor market are now more balanced in 2024, there are still some areas within the chip sector where demand far outstrips supply, especially for AI chips. With insatiable demand for AI chips in the data center and what appears to be the start of a hardware upgrade cycle needed to support AI-powered applications, the semiconductor industry continues to find itself in a strong spot.

Based on the current chip environment, one company in particular looks best suited to be a long-term winner: Taiwan Semiconductor Manufacturing Company (NYSE: TSM), or TSMC for short.

The arms dealer in the chip race

The biggest theme in the semiconductor market is, no doubt, the race to build out the data centers needed to support AI. Nvidia and its graphic processing units (GPUs) have been the biggest winners thus far, with insatiable demand for Nvidia products. The company currently owns about an estimated 80% market share in GPUs.

Advanced Micro Devices has always been Nvidia's biggest rival, and the company is projecting $4 billion in AI chip sales this year, a $500 million increase from recent estimates. Intel, meanwhile, just introduced its Xeon 6 processor for data centers, and the Gaudi 2 and Gaudi 3 AI accelerators to try to capture some AI market share.

However, the market is so lucrative that many heavy hitters are trying to get into the act with their own AI chips. For example, Amazon has introduced two, Trainium and Inferentia, that its cloud computing customers can use. Alphabet has been pushing its latest Trillium chips, while also recently developing a CPU (central processing unit) based on one from Arm Holdings. Microsoft and Meta Platforms have joined the fray as well.

Not to be outdone, Apple is developing its own in-house AI server chips to be used within its data centers for AI inference. It's introduced a new M4 chip focused on running AI applications on its devices. Apple has also been rumored to be trying to lock up all of TSMC's capacity in the newest 2-nanometer technology.

Softbank and Arm will reportedly set up an AI chip division, to provide homegrown chips to the data centers that Softbank plans to build around the globe; it has already been in talks with TSMC to try and secure capacity.

Image source: Getty Images.

This is all great news for TSMC. Most of these companies don't own their own fabrication facilities ("fabs"), instead opting to outsource their chip manufacturing. With all these companies looking to get into the AI chip game, TSMC is building out its own capacity to help keep up with demand. The current supply-demand imbalance also gives it solid negotiating power when signing up customers for new capacity.

In addition to building new fabs, TSMC is set to move down to 2-nanometer production technology, which is what Apple is reportedly looking to secure. The smaller the chips, the more that fit onto a wafer, leading to increased capacity and lower costs. The denser chips, meanwhile, provide lower power consumption and higher speeds.

An attractive stock to buy

Whoever the winners of the war over AI chips will be, TSMC is set to benefit from the increased competition in the space and the need of companies to secure production capacity. With AI still believed to be in its early days, the long-term future for TSMC appears bright.

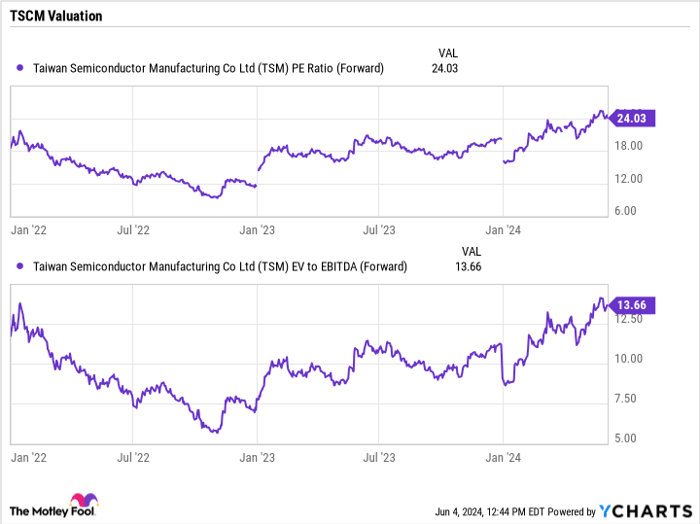

The stock currently trades at a forward price-to-earnings (P/E) ratio of 24, and a multiple of under 14 on an enterprise value-to-EBITDA basis. The latter metric considers its net debt position and takes out noncash expenses such as depreciation. Given the upfront costs to build new fabs and the associated depreciation, I prefer this metric when valuing TSMC. However, I find the stock attractively valued using either P/E or EV/EBITDA, based on future growth.

TSM PE Ratio (Forward) data by YCharts.

There will likely be a number of winning AI stocks. But TSMC looks like one of the safest bets to benefit from the increasing demand for all things AI-related, and the chips that are helping power this AI revolution.

Should you invest $1,000 in Taiwan Semiconductor Manufacturing right now?

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $741,362!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 3, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors.

Geoffrey Seiler has positions in Alphabet. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short August 2024 $35 calls on Intel, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.