ICON plc ICLR has put valuation back in focus after a -16.2% year-to-date drop, even as the stock is up 9.9% over the past 12 months. The move looks softer than the broader tape, with the S&P 500 up 10.2% year to date and up 29.3% over the past year.

Against its benchmarks, the setup is mixed. The Zacks sub-industry and Zacks Medical sector are down 11.2% and 7.5% year to date, and down 3.2% and up 0.8% over the past year, respectively. That dispersion matters because it shapes whether the stock’s multiple is truly “cheap” or simply reflecting a shifting earnings backdrop.

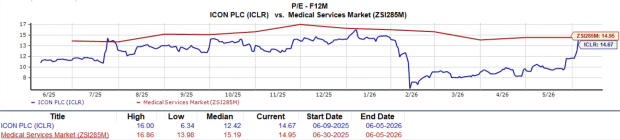

ICON’s Forward Multiple vs Benchmarks

On the surface, the valuation case is straightforward. ICON trades at 14.7X forward 12-month earnings, below 15.0X for the Zacks sub-industry, 19.5X for the Zacks Medical sector and 22.0X for the S&P 500.

That discount is not subtle, and it is also below the company’s own five-year median multiple of 18.3X (with a five-year range of 6.3X to 33.6X). The market is already paying less for each dollar of expected earnings than it does for peers and the broader index. The key question is whether that gap compensates investors for near-term uncertainty.

Image Source: Zacks Investment Research

ICLR’s Price Target Logic and What It Assumes

The price target is explicitly multiple-driven. ICON’s $145 target is based on 12.2X forward 12-month earnings, which sits close to the current trading multiple. That construction frames the call as one where upside is not dependent on a re-rating. It is largely about whether earnings execution stabilizes while the multiple remains restrained.

The multiple choice also matches a view that the stock is likely to lag the market over the next 6 to 12 months. With a cautious outlook already embedded, investors are left weighing whether incremental proof points can lift confidence enough to expand the valuation, or whether the reset keeps a lid on what the market is willing to pay.

ICON’s 2026 Guidance Creates a Multiple Trap Risk

A lower forward multiple can look attractive, but the “E” in the ratio is where the tension sits for ICON. Management guided to 2026 revenue of $7.85-$8.15 billion and adjusted earnings per share of $10.00-$11.00. That implies a down year versus 2025 revenue of $8.25 billion and adjusted earnings per share of $12.53.

The guidance is tied to prior-year cancellations and a weaker bookings environment that persisted from 2024 through the first three quarters of 2025, with elevated cancellation activity weighing on 2026 conversion. Pass-through revenue is expected to remain broadly in line with 2025 levels, which implies a steeper decline in direct fee revenue and can limit growth visibility even as commercial indicators improve. In that context, a “cheap” multiple can become a trap if estimates keep resetting lower.

ICON’s Margin Path Is the Real Catalyst or Warning

Margins are where the next leg likely gets decided. Fourth-quarter 2025 results showed how quickly profitability can swing when mix and estimates move. Pass-through revenue exceeded expectations by more than $150 million, and a portfolio review drove cost-to-complete and realizable value adjustments that management said reduced quarterly earnings by more than $50 million. Adjusted EBITDA margin fell to 15.5%, and adjusted earnings per share dropped to $2.52 from $3.86 a year ago.

Management expects first-quarter 2026 results to start near that fourth-quarter run rate and to improve through 2026, but the weaker starting point increases sensitivity to mix, pass-through timing and operational efficiency initiatives. Management also flagged that 2026 margins will be shaped by mix and sustained pass-through levels, with automation and technology deployment targeted to support margin progression. Execution risk is high because even small deviations in portfolio assumptions can flow directly into profitability.

Based on short-term price targets offered by 14 analysts, the average price target of $151.57 represents an decrease of 0.8% from the last closing price.

Image Source: Zacks Investment Research

ICLR’s Decision Lens for Investors

For investors with a transaction mindset, the valuation discount is real, but it is not the only variable. The stock carries Zacks Rank #5 (Strong Sell). That rating keeps the burden of proof on the company to demonstrate that remediation is fully embedded and that operational performance can stabilize through the reset year.

The “cheap enough” question hinges on credibility around remediation, evidence that bookings and cancellations are stabilizing, and signs that margins can climb from the lower early-2026 starting level. In the peer set, IQVIA Holdings Inc. IQV and Thermo Fisher Scientific Inc. TMO both carry Zacks Rank #3 (Hold), underscoring how differently the market is treating near-term visibility and execution risk across the group.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThermo Fisher Scientific Inc. (TMO) : Free Stock Analysis Report

ICON PLC (ICLR) : Free Stock Analysis Report

IQVIA Holdings Inc. (IQV) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.